Advertisement

- United States

- /

- Biotech

- /

- NasdaqCM:SGMO

Companies Like Sangamo Therapeutics (NASDAQ:SGMO) Are In A Position To Invest In Growth

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. Having said that, unprofitable companies are risky because they could potentially burn through all their cash and become distressed.

Given this risk, we thought we'd take a look at whether Sangamo Therapeutics (NASDAQ:SGMO) shareholders should be worried about its cash burn. In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

How Long Is Sangamo Therapeutics' Cash Runway?

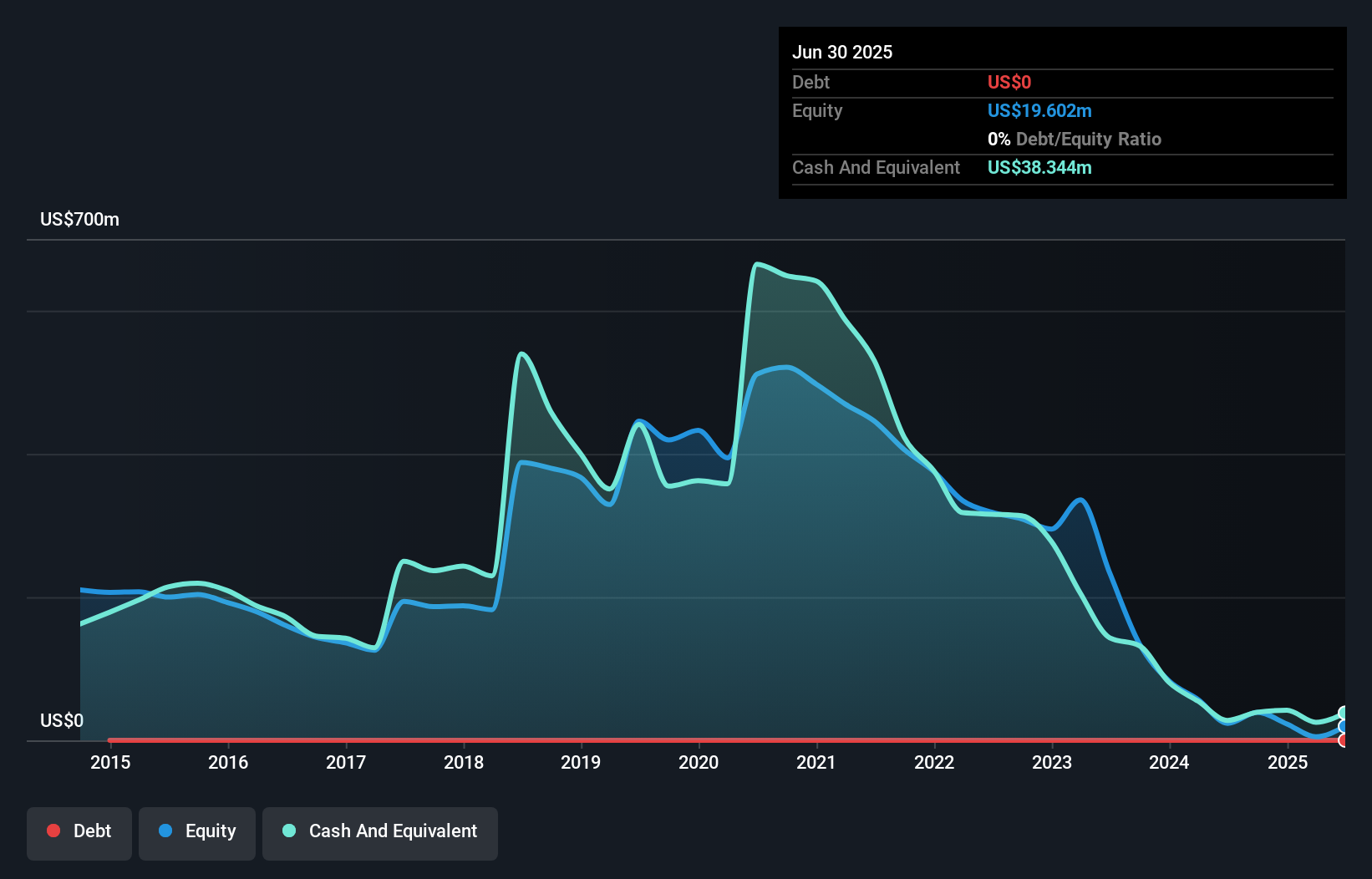

A company's cash runway is calculated by dividing its cash hoard by its cash burn. In June 2025, Sangamo Therapeutics had US$38m in cash, and was debt-free. Importantly, its cash burn was US$36m over the trailing twelve months. That means it had a cash runway of around 13 months as of June 2025. Notably, analysts forecast that Sangamo Therapeutics will break even (at a free cash flow level) in about 3 years. Essentially, that means the company will either reduce its cash burn, or else require more cash. You can see how its cash balance has changed over time in the image below.

Check out our latest analysis for Sangamo Therapeutics

How Well Is Sangamo Therapeutics Growing?

Happily, Sangamo Therapeutics is travelling in the right direction when it comes to its cash burn, which is down 80% over the last year. But its revenue is better yet, flying higher than Elon Musk and his rocket, with growth of 566% in the last year. Overall, we'd say its growth is rather impressive. Clearly, however, the crucial factor is whether the company will grow its business going forward. So you might want to take a peek at how much the company is expected to grow in the next few years.

Can Sangamo Therapeutics Raise More Cash Easily?

Sangamo Therapeutics seems to be in a fairly good position, in terms of cash burn, but we still think it's worthwhile considering how easily it could raise more money if it wanted to. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Many companies end up issuing new shares to fund future growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Sangamo Therapeutics has a market capitalisation of US$165m and burnt through US$36m last year, which is 22% of the company's market value. That's fairly notable cash burn, so if the company had to sell shares to cover the cost of another year's operations, shareholders would suffer some costly dilution.

How Risky Is Sangamo Therapeutics' Cash Burn Situation?

On this analysis of Sangamo Therapeutics' cash burn, we think its revenue growth was reassuring, while its cash burn relative to its market cap has us a bit worried. Shareholders can take heart from the fact that analysts are forecasting it will reach breakeven. Based on the factors mentioned in this article, we think its cash burn situation warrants some attention from shareholders, but we don't think they should be worried. Taking a deeper dive, we've spotted 4 warning signs for Sangamo Therapeutics you should be aware of, and 2 of them are potentially serious.

Of course Sangamo Therapeutics may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:SGMO

Sangamo Therapeutics

A clinical-stage genomic medicine company, focuses on translating science into medicines that transform the lives of patients and families afflicted with serious diseases in the United States.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|28.9% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|27.0% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|1.9% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.5% undervalued

RO

Community Contributor