Advertisement

- United States

- /

- Biotech

- /

- NasdaqGM:RYTM

Industry Analysts Just Made An Incredible Upgrade To Their Rhythm Pharmaceuticals, Inc. (NASDAQ:RYTM) Revenue Forecasts

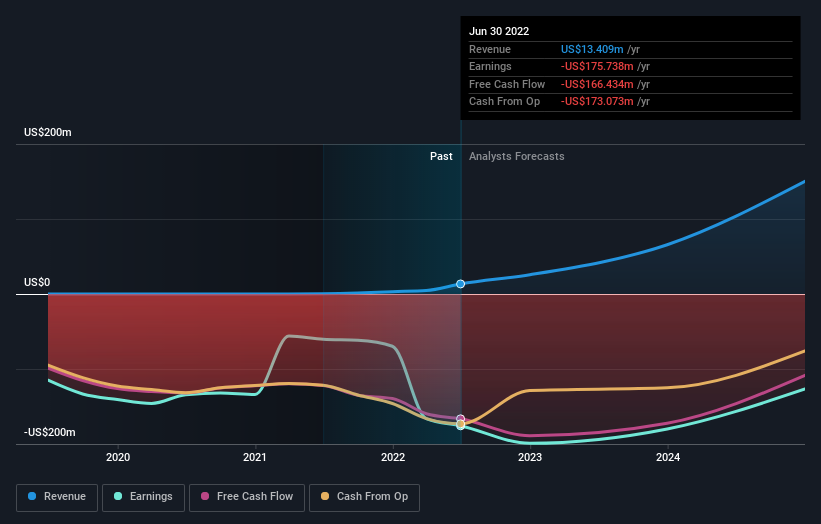

Celebrations may be in order for Rhythm Pharmaceuticals, Inc. (NASDAQ:RYTM) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The consensus estimated revenue numbers rose, with their view now clearly much more bullish on the company's business prospects. Investors have been pretty optimistic on Rhythm Pharmaceuticals too, with the stock up 61% to US$20.24 over the past week. It will be interesting to see if today's upgrade is enough to propel the stock even higher.

After the upgrade, the eight analysts covering Rhythm Pharmaceuticals are now predicting revenues of US$26m in 2022. If met, this would reflect a substantial 92% improvement in sales compared to the last 12 months. Losses are expected to increase substantially, hitting US$3.85 per share. Yet before this consensus update, the analysts had been forecasting revenues of US$16m and losses of US$3.89 per share in 2022. So there's definitely been a change in sentiment in this update, with the analysts upgrading this year's revenue estimates, while at the same time holding losses per share steady.

See our latest analysis for Rhythm Pharmaceuticals

Analysts increased their price target 21% to US$25.50, perhaps signalling that higher revenues are a strong leading indicator for Rhythm Pharmaceuticals's valuation. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic Rhythm Pharmaceuticals analyst has a price target of US$40.00 per share, while the most pessimistic values it at US$6.00. So we wouldn't be assigning too much credibility to analyst price targets in this case, because there are clearly some widely differing views on what kind of performance this business can generate. With this in mind, we wouldn't rely too heavily on the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

Of course, another way to look at these forecasts is to place them into context against the industry itself. The analysts are definitely expecting Rhythm Pharmaceuticals' growth to accelerate, with the forecast 268% annualised growth to the end of 2022 ranking favourably alongside historical growth of 101% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 14% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Rhythm Pharmaceuticals to grow faster than the wider industry.

The Bottom Line

The most important thing here is that analysts reduced their loss per share estimates for this year, reflecting increased optimism around Rhythm Pharmaceuticals' prospects. They also upgraded their revenue estimates for this year, and sales are expected to grow faster than the wider market. There was also a nice increase in the price target, with analysts apparently feeling that the intrinsic value of the business is improving. Seeing the dramatic upgrade to this year's forecasts, it might be time to take another look at Rhythm Pharmaceuticals.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. At Simply Wall St, we have a full range of analyst estimates for Rhythm Pharmaceuticals going out to 2024, and you can see them free on our platform here..

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:RYTM

Rhythm Pharmaceuticals

A commercial-stage biopharmaceutical company, focuses on the rare neuroendocrine diseases.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.7% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor