Advertisement

- United States

- /

- Biotech

- /

- NasdaqGS:RXRX

Analysts Are Betting On Recursion Pharmaceuticals, Inc. (NASDAQ:RXRX) With A Big Upgrade This Week

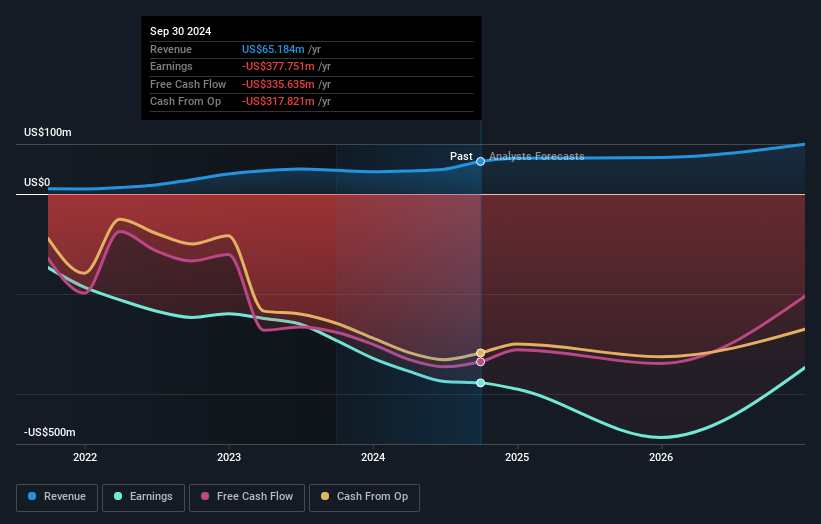

Celebrations may be in order for Recursion Pharmaceuticals, Inc. (NASDAQ:RXRX) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The analysts have sharply increased their revenue numbers, with a view that Recursion Pharmaceuticals will make substantially more sales than they'd previously expected. The market may be pricing in some blue sky too, with the share price gaining 11% to US$7.10 in the last 7 days. We'll be curious to see if these new estimates convince the market to lift the stock price higher still.

Following the upgrade, the most recent consensus for Recursion Pharmaceuticals from its eight analysts is for revenues of US$73m in 2025 which, if met, would be a notable 12% increase on its sales over the past 12 months. Losses are supposed to balloon 33% to US$1.76 per share. Yet prior to the latest estimates, the analysts had been forecasting revenues of US$63m and losses of US$1.79 per share in 2025. So there's been quite a change-up of views after the recent consensus updates, withthe analysts noticeably increasing their revenue forecasts while also expecting losses per share to hold steady.

View our latest analysis for Recursion Pharmaceuticals

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Recursion Pharmaceuticals' past performance and to peers in the same industry. It's pretty clear that there is an expectation that Recursion Pharmaceuticals' revenue growth will slow down substantially, with revenues to the end of 2025 expected to display 9.4% growth on an annualised basis. This is compared to a historical growth rate of 50% over the past five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 21% per year. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Recursion Pharmaceuticals.

The Bottom Line

The most important thing here is that analysts reduced their loss per share estimates for next year, reflecting increased optimism around Recursion Pharmaceuticals' prospects. Pleasantly, analysts also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow slower than the wider market. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at Recursion Pharmaceuticals.

These earnings upgrades look like a sterling endorsement, but before diving in - you should know that we've spotted 3 potential concerns with Recursion Pharmaceuticals, including dilutive stock issuance over the past year. You can learn more, and discover the 2 other concerns we've identified, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies backed by insiders.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:RXRX

Recursion Pharmaceuticals

Operates as a clinical-stage biotechnology company, engages in the decoding biology and chemistry by integrating technological innovations across biology, chemistry, automation, data science, and engineering to industrialize drug discovery in the United States.

Excellent balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4729.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.8% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.8% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.71.9% undervalued

1341 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative