- United States

- /

- Pharma

- /

- NasdaqCM:RGC

Here's Why We're Not Too Worried About Regencell Bioscience Holdings' (NASDAQ:RGC) Cash Burn Situation

Just because a business does not make any money, does not mean that the stock will go down. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. Having said that, unprofitable companies are risky because they could potentially burn through all their cash and become distressed.

Given this risk, we thought we'd take a look at whether Regencell Bioscience Holdings (NASDAQ:RGC) shareholders should be worried about its cash burn. In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. Let's start with an examination of the business' cash, relative to its cash burn.

View our latest analysis for Regencell Bioscience Holdings

How Long Is Regencell Bioscience Holdings' Cash Runway?

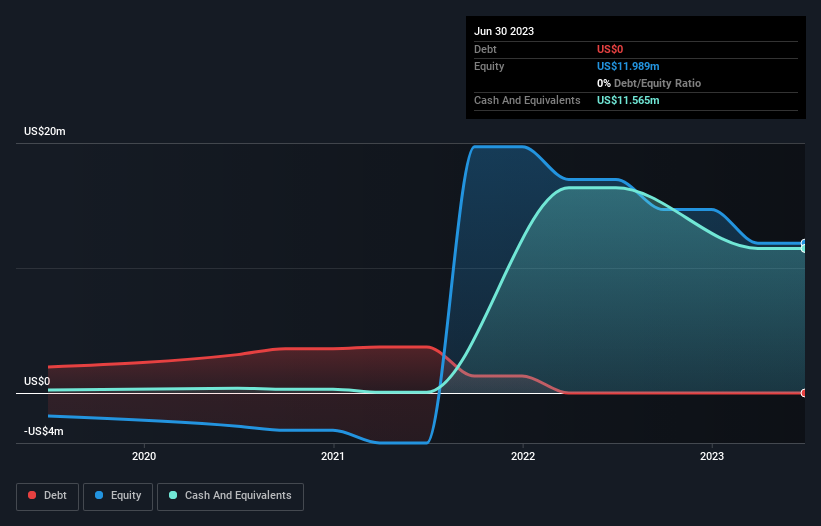

A company's cash runway is calculated by dividing its cash hoard by its cash burn. When Regencell Bioscience Holdings last reported its balance sheet in June 2023, it had zero debt and cash worth US$12m. Importantly, its cash burn was US$5.0m over the trailing twelve months. That means it had a cash runway of about 2.3 years as of June 2023. That's decent, giving the company a couple years to develop its business. You can see how its cash balance has changed over time in the image below.

How Is Regencell Bioscience Holdings' Cash Burn Changing Over Time?

Regencell Bioscience Holdings didn't record any revenue over the last year, indicating that it's an early stage company still developing its business. So while we can't look to sales to understand growth, we can look at how the cash burn is changing to understand how expenditure is trending over time. As it happens, the company's cash burn reduced by 17% over the last year, which suggests that management are maintaining a fairly steady rate of business development, albeit with a slight decrease in spending. Regencell Bioscience Holdings makes us a little nervous due to its lack of substantial operating revenue. We prefer most of the stocks on this list of stocks that analysts expect to grow.

How Easily Can Regencell Bioscience Holdings Raise Cash?

Even though it has reduced its cash burn recently, shareholders should still consider how easy it would be for Regencell Bioscience Holdings to raise more cash in the future. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Since it has a market capitalisation of US$193m, Regencell Bioscience Holdings' US$5.0m in cash burn equates to about 2.6% of its market value. That means it could easily issue a few shares to fund more growth, and might well be in a position to borrow cheaply.

How Risky Is Regencell Bioscience Holdings' Cash Burn Situation?

It may already be apparent to you that we're relatively comfortable with the way Regencell Bioscience Holdings is burning through its cash. In particular, we think its cash burn relative to its market cap stands out as evidence that the company is well on top of its spending. Its weak point is its cash burn reduction, but even that wasn't too bad! After taking into account the various metrics mentioned in this report, we're pretty comfortable with how the company is spending its cash, as it seems on track to meet its needs over the medium term. Taking an in-depth view of risks, we've identified 3 warning signs for Regencell Bioscience Holdings that you should be aware of before investing.

Of course Regencell Bioscience Holdings may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you're looking to trade Regencell Bioscience Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:RGC

Regencell Bioscience Holdings

Operates as a Traditional Chinese medicine (TCM) bioscience company in Hong Kong.

Adequate balance sheet low.

Market Insights

Community Narratives