- United States

- /

- Biotech

- /

- NasdaqCM:RCEL

AVITA Medical, Inc.'s (NASDAQ:RCEL) Price Is Right But Growth Is Lacking After Shares Rocket 39%

Despite an already strong run, AVITA Medical, Inc. (NASDAQ:RCEL) shares have been powering on, with a gain of 39% in the last thirty days. Looking back a bit further, it's encouraging to see the stock is up 85% in the last year.

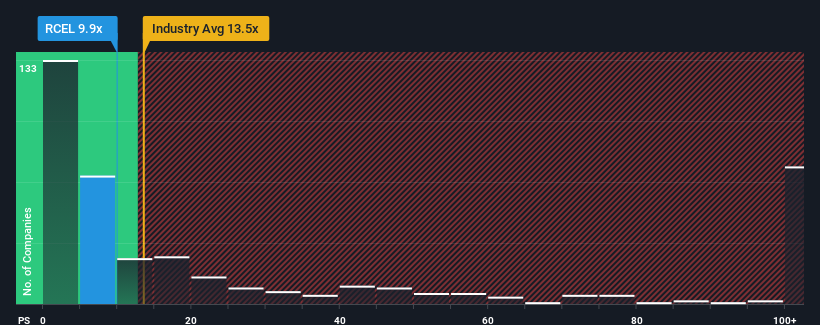

In spite of the firm bounce in price, AVITA Medical may still be sending buy signals at present with its price-to-sales (or "P/S") ratio of 9.9x, considering almost half of all companies in the Biotechs industry in the United States have P/S ratios greater than 13.5x and even P/S higher than 57x aren't out of the ordinary. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

View our latest analysis for AVITA Medical

How AVITA Medical Has Been Performing

Recent times have been advantageous for AVITA Medical as its revenues have been rising faster than most other companies. Perhaps the market is expecting future revenue performance to dive, which has kept the P/S suppressed. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on AVITA Medical.How Is AVITA Medical's Revenue Growth Trending?

AVITA Medical's P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 42%. Pleasingly, revenue has also lifted 182% in aggregate from three years ago, thanks to the last 12 months of growth. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Turning to the outlook, the next three years should generate growth of 43% per year as estimated by the nine analysts watching the company. With the industry predicted to deliver 228% growth per annum, the company is positioned for a weaker revenue result.

With this in consideration, its clear as to why AVITA Medical's P/S is falling short industry peers. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

What Does AVITA Medical's P/S Mean For Investors?

AVITA Medical's stock price has surged recently, but its but its P/S still remains modest. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that AVITA Medical maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. Shareholders' pessimism on the revenue prospects for the company seems to be the main contributor to the depressed P/S. The company will need a change of fortune to justify the P/S rising higher in the future.

There are also other vital risk factors to consider before investing and we've discovered 1 warning sign for AVITA Medical that you should be aware of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:RCEL

AVITA Medical

Operates as a regenerative medicine company in the United States and internationally.

Exceptional growth potential and undervalued.

Similar Companies

Market Insights

Community Narratives