Advertisement

- United States

- /

- Pharma

- /

- NasdaqGM:MDWD

Optimistic Investors Push MediWound Ltd. (NASDAQ:MDWD) Shares Up 26% But Growth Is Lacking

MediWound Ltd. (NASDAQ:MDWD) shares have continued their recent momentum with a 26% gain in the last month alone. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 9.6% over the last year.

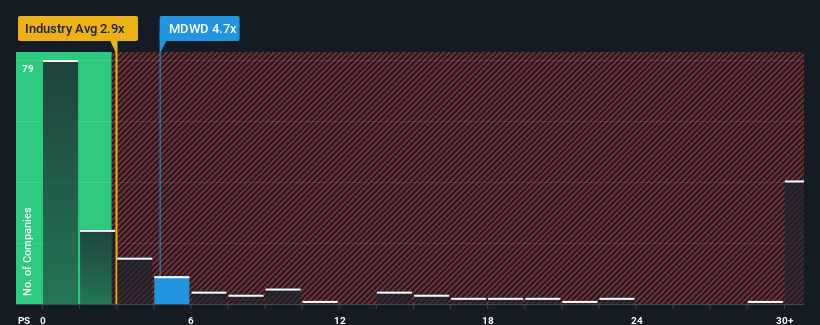

After such a large jump in price, MediWound may be sending sell signals at present with a price-to-sales (or "P/S") ratio of 4.7x, when you consider almost half of the companies in the Pharmaceuticals industry in the United States have P/S ratios under 2.9x and even P/S lower than 0.7x aren't out of the ordinary. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for MediWound

What Does MediWound's Recent Performance Look Like?

Recent times haven't been great for MediWound as its revenue has been rising slower than most other companies. One possibility is that the P/S ratio is high because investors think this lacklustre revenue performance will improve markedly. If not, then existing shareholders may be very nervous about the viability of the share price.

Keen to find out how analysts think MediWound's future stacks up against the industry? In that case, our free report is a great place to start.Do Revenue Forecasts Match The High P/S Ratio?

MediWound's P/S ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the industry.

Taking a look back first, we see that the company grew revenue by an impressive 23% last year. The latest three year period has also seen a 22% overall rise in revenue, aided extensively by its short-term performance. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Turning to the outlook, the next three years should generate growth of 25% each year as estimated by the four analysts watching the company. Meanwhile, the rest of the industry is forecast to expand by 53% each year, which is noticeably more attractive.

With this information, we find it concerning that MediWound is trading at a P/S higher than the industry. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

What We Can Learn From MediWound's P/S?

MediWound shares have taken a big step in a northerly direction, but its P/S is elevated as a result. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Despite analysts forecasting some poorer-than-industry revenue growth figures for MediWound, this doesn't appear to be impacting the P/S in the slightest. When we see a weak revenue outlook, we suspect the share price faces a much greater risk of declining, bringing back down the P/S figures. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

It is also worth noting that we have found 1 warning sign for MediWound that you need to take into consideration.

If you're unsure about the strength of MediWound's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:MDWD

MediWound

A biopharmaceutical company, develops, manufactures, and commercializes novel, bio-therapeutic, and non-surgical solutions for tissue repair and regeneration in the United States and internationally.

Flawless balance sheet with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|28.9% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|46.3% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|33.9% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|56.1% undervalued

AX

Community Contributor