Advertisement

- United States

- /

- Pharma

- /

- NasdaqGM:MDWD

MediWound Ltd.'s (NASDAQ:MDWD) 26% Share Price Surge Not Quite Adding Up

MediWound Ltd. (NASDAQ:MDWD) shareholders would be excited to see that the share price has had a great month, posting a 26% gain and recovering from prior weakness. Taking a wider view, although not as strong as the last month, the full year gain of 12% is also fairly reasonable.

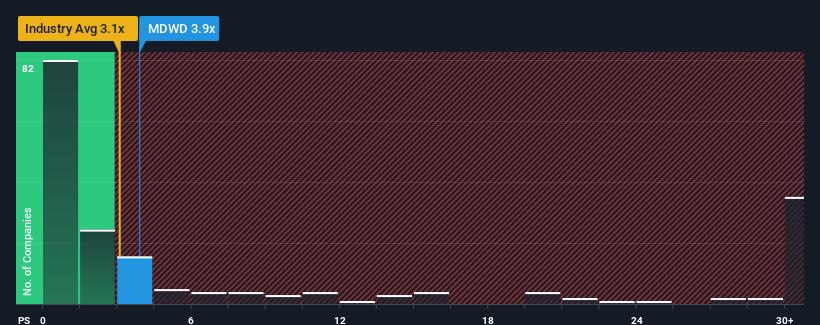

Following the firm bounce in price, MediWound's price-to-sales (or "P/S") ratio of 3.9x might make it look like a sell right now compared to the wider Pharmaceuticals industry in the United States, where around half of the companies have P/S ratios below 3.1x and even P/S below 0.7x are quite common. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for MediWound

How MediWound Has Been Performing

With revenue growth that's inferior to most other companies of late, MediWound has been relatively sluggish. One possibility is that the P/S ratio is high because investors think this lacklustre revenue performance will improve markedly. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on MediWound.Do Revenue Forecasts Match The High P/S Ratio?

In order to justify its P/S ratio, MediWound would need to produce impressive growth in excess of the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 23%. The latest three year period has also seen a 22% overall rise in revenue, aided extensively by its short-term performance. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Turning to the outlook, the next three years should generate growth of 31% per year as estimated by the four analysts watching the company. That's shaping up to be materially lower than the 53% per annum growth forecast for the broader industry.

With this in consideration, we believe it doesn't make sense that MediWound's P/S is outpacing its industry peers. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as this level of revenue growth is likely to weigh heavily on the share price eventually.

The Key Takeaway

MediWound shares have taken a big step in a northerly direction, but its P/S is elevated as a result. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've concluded that MediWound currently trades on a much higher than expected P/S since its forecast growth is lower than the wider industry. The weakness in the company's revenue estimate doesn't bode well for the elevated P/S, which could take a fall if the revenue sentiment doesn't improve. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Having said that, be aware MediWound is showing 2 warning signs in our investment analysis, and 1 of those can't be ignored.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:MDWD

MediWound

A biopharmaceutical company, develops, manufactures, and commercializes novel, bio-therapeutic, and non-surgical solutions for tissue repair and regeneration in the United States and internationally.

Flawless balance sheet with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|29.6% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|49.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.8% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.2% undervalued

AX

Community Contributor