Advertisement

- United States

- /

- Pharma

- /

- NasdaqCM:LQDA

Broker Revenue Forecasts For Liquidia Corporation (NASDAQ:LQDA) Are Surging Higher

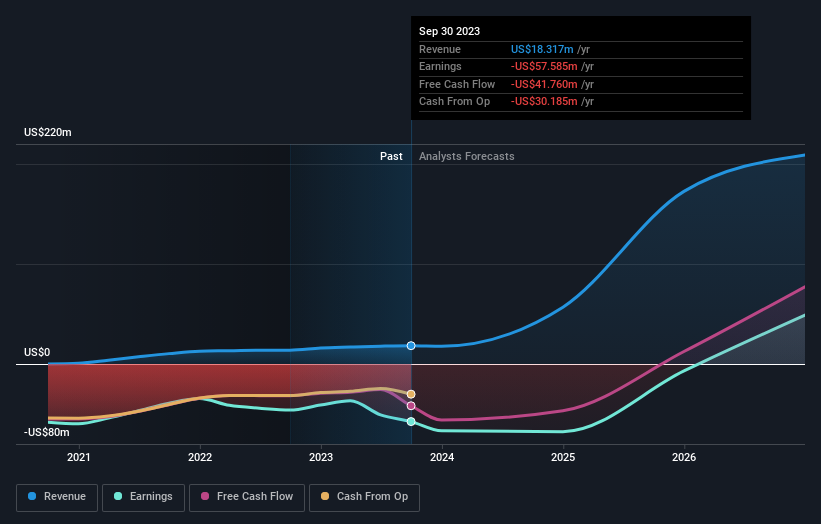

Shareholders in Liquidia Corporation (NASDAQ:LQDA) may be thrilled to learn that the analysts have just delivered a major upgrade to their near-term forecasts. The revenue forecast for next year has experienced a facelift, with the analysts now much more optimistic on its sales pipeline. The market seems to be pricing in some improvement in the business too, with the stock up 7.2% over the past week, closing at US$13.34. It will be interesting to see if this latest upgrade is enough to kickstart further buying interest in the stock.

Following the upgrade, the latest consensus from Liquidia's seven analysts is for revenues of US$57m in 2024, which would reflect a substantial 210% improvement in sales compared to the last 12 months. Per-share losses are expected to explode, reaching US$0.93 per share. Yet prior to the latest estimates, the analysts had been forecasting revenues of US$52m and losses of US$0.94 per share in 2024. So there's definitely been a change in sentiment in this update, with the analysts upgrading next year's revenue estimates, while at the same time holding losses per share steady.

Check out our latest analysis for Liquidia

Analysts increased their price target 5.8% to US$20.86, perhaps signalling that higher revenues are a strong leading indicator for Liquidia's valuation.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's clear from the latest estimates that Liquidia's rate of growth is expected to accelerate meaningfully, with the forecast 147% annualised revenue growth to the end of 2024 noticeably faster than its historical growth of 35% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 7.9% annually. Factoring in the forecast acceleration in revenue, it's pretty clear that Liquidia is expected to grow much faster than its industry.

The Bottom Line

The highlight for us was that the consensus reduced its estimated losses next year, perhaps suggesting Liquidia is moving incrementally towards profitability. They also upgraded their revenue estimates for next year, and sales are expected to grow faster than the wider market. There was also an increase in the price target, suggesting that there is more optimism baked into the forecasts than there was previously. Seeing the dramatic upgrade to next year's forecasts, it might be time to take another look at Liquidia.

That's a pretty serious upgrade, but shareholders might be even more pleased to know that forecasts expect Liquidia to be able to reach break-even within the next few years. For more information, you can click through to our free platform to learn more about these forecasts.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:LQDA

Liquidia

A biopharmaceutical company, develops, manufactures, and commercializes various products for unmet patient needs in the United States.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor