Advertisement

- United States

- /

- Biotech

- /

- NasdaqCM:IMTX

How Rising Losses in the Latest Results Will Impact Immatics (IMTX) Investors

Simply Wall St

Reviewed by Sasha Jovanovic

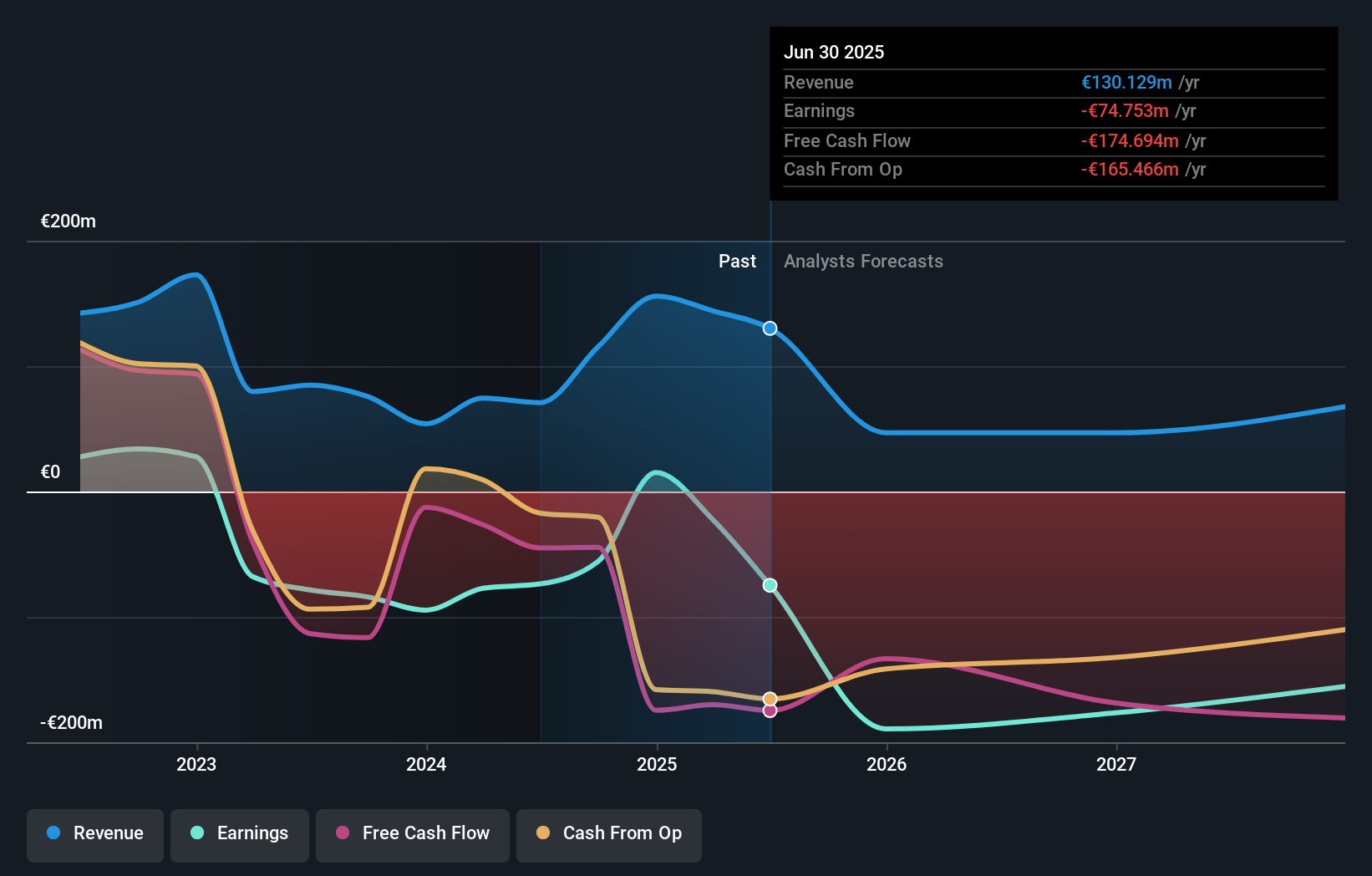

- Immatics N.V. recently reported third quarter and nine-month earnings results, disclosing a net loss of €50.55 million for the quarter and €160.75 million for the nine months ended September 30, 2025, both figures significantly higher than the same periods a year earlier.

- The marked increase in net losses and loss per share could point to heightened operational costs or pressures on revenue generation for the company.

- Given the significantly higher quarterly loss, we’ll examine how this may reshape Immatics’ investment narrative and outlook.

We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

What Is Immatics' Investment Narrative?

To be a shareholder in Immatics, you need conviction in the long-term potential of its cancer immunotherapy pipeline and confidence that the company’s innovation and partnerships, such as its work with Moderna and Bristol Myers Squibb, will eventually translate into meaningful clinical or commercial milestones. The recent Q3 earnings news, with a quarterly net loss of €50.55 million and a nine-month loss of €160.75 million, signals a marked acceleration in spending or pressure on revenue that can heighten concerns around cash burn and funding needs. Previously, short-term focus was on clinical trial updates and alliance progress, but this level of loss raises the importance of near-term financial management and potential dilution risks. For now, the biggest risk has shifted, investors must closely watch if Immatics can sustain its ambitious R&D program without compromising financial stability as it approaches key data readouts.

But against the promise of new therapies, mounting financial pressures could become a real test for shareholders. Upon reviewing our latest valuation report, Immatics' share price might be too optimistic.Exploring Other Perspectives

Explore 4 other fair value estimates on Immatics - why the stock might be worth less than half the current price!

Build Your Own Immatics Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Immatics research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Immatics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Immatics' overall financial health at a glance.

Looking For Alternative Opportunities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:IMTX

Immatics

A clinical-stage biopharmaceutical company, focuses on the research and development of potential T cell redirecting immunotherapies for the treatment of cancer in the United States.

Flawless balance sheet with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative