Advertisement

- United States

- /

- Life Sciences

- /

- NasdaqGM:HBIO

Further weakness as Harvard Bioscience (NASDAQ:HBIO) drops 11% this week, taking three-year losses to 69%

If you love investing in stocks you're bound to buy some losers. But long term Harvard Bioscience, Inc. (NASDAQ:HBIO) shareholders have had a particularly rough ride in the last three year. So they might be feeling emotional about the 69% share price collapse, in that time. The more recent news is of little comfort, with the share price down 61% in a year. The falls have accelerated recently, with the share price down 25% in the last three months.

After losing 11% this past week, it's worth investigating the company's fundamentals to see what we can infer from past performance.

View our latest analysis for Harvard Bioscience

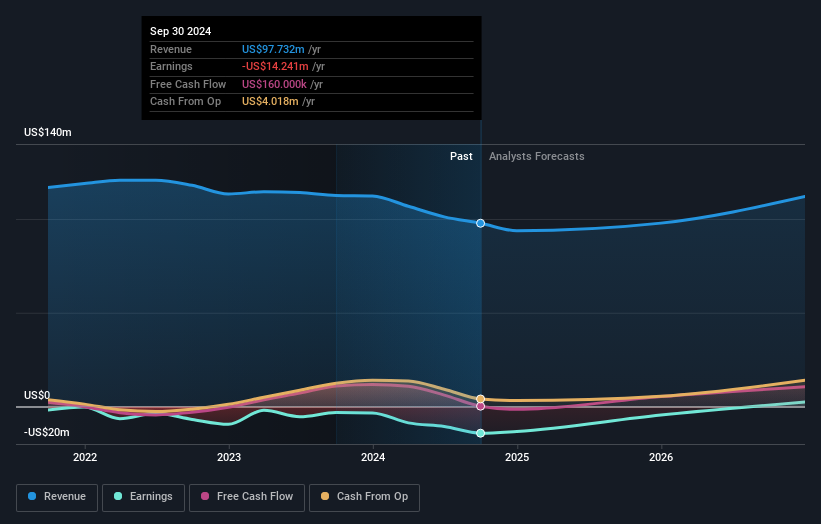

Given that Harvard Bioscience didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. Shareholders of unprofitable companies usually desire strong revenue growth. That's because it's hard to be confident a company will be sustainable if revenue growth is negligible, and it never makes a profit.

Over the last three years, Harvard Bioscience's revenue dropped 5.7% per year. That's not what investors generally want to see. With revenue in decline, and profit but a dream, we can understand why the share price has been declining at 19% per year. Of course, it's the future that will determine whether today's price is a good one. We don't generally like to own companies that lose money and can't grow revenues. But any company is worth looking at when it makes a maiden profit.

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

This free interactive report on Harvard Bioscience's balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

While the broader market gained around 23% in the last year, Harvard Bioscience shareholders lost 61%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 7% over the last half decade. Generally speaking long term share price weakness can be a bad sign, though contrarian investors might want to research the stock in hope of a turnaround. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Take risks, for example - Harvard Bioscience has 2 warning signs we think you should be aware of.

We will like Harvard Bioscience better if we see some big insider buys. While we wait, check out this free list of undervalued stocks (mostly small caps) with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Harvard Bioscience might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:HBIO

Harvard Bioscience

Develops, manufactures, and sells technologies, products, and services for life science applications in the United States, Germany, and internationally.

Fair value with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|37.8% undervalued

IN

Community Contributor

CSL is undervalued in High Tax Scenario

Fair Value AU$263.33|10.2% undervalued

RA

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor