Advertisement

- United States

- /

- Life Sciences

- /

- NasdaqGS:FTRE

Fortrea (FTRE) Valuation Check as Legal Probe Questions Revenue Recognition and 2025 EBITDA Targets

Simply Wall St

Reviewed by Simply Wall St

Fortrea Holdings (FTRE) is back in the spotlight after Grabar Law Office launched an investigation into whether its leadership misled investors on revenue recognition, cost savings, and 2025 EBITDA expectations.

See our latest analysis for Fortrea Holdings.

That backdrop helps explain why, even with a sharp 1 month share price return of 25.99 percent and 3 month share price return of 21.31 percent off a 12.75 dollars close, Fortrea’s year to date share price return of negative 31.64 percent and 1 year total shareholder return of negative 46.27 percent suggest recent momentum is more about shifting risk perceptions than a settled turnaround story.

If this kind of volatility has you reassessing your watchlist, it could be a good moment to scan other healthcare names through healthcare stocks and compare how their risk reward profiles stack up.

With shares still down sharply over 12 months but screening as deeply discounted on intrinsic value, the key question now is whether Fortrea is genuinely mispriced or if the market already anticipates all the growth ahead.

Most Popular Narrative Narrative: 14% Overvalued

With the narrative fair value sitting below Fortrea’s recent 12.75 dollars close, the story hinges on whether leaner operations can truly transform long term earnings power.

Post spin, the company has executed significant cost optimization initiatives (achieving over 50 million dollars in net savings year to date and targeting 90 to 100 million dollars for the year), with further SG and A savings and margin improvements anticipated in 2026 as more of these initiatives annualize supporting both EBITDA and net income growth.

Curious how flat top line expectations can still support a higher value case, built on sharply improving margins and a surprisingly low future earnings multiple? The full narrative unpacks the precise mix of revenue stability, margin rebuild, and valuation reset driving this fair value call. Dive in to see which assumptions matter most for Fortrea’s next chapter.

Result: Fair Value of $11.21 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, declining biotech win rates and heavy reliance on a concentrated customer base could quickly undermine the margin rebuild that underpins this valuation case.

Find out about the key risks to this Fortrea Holdings narrative.

Another Lens on Value

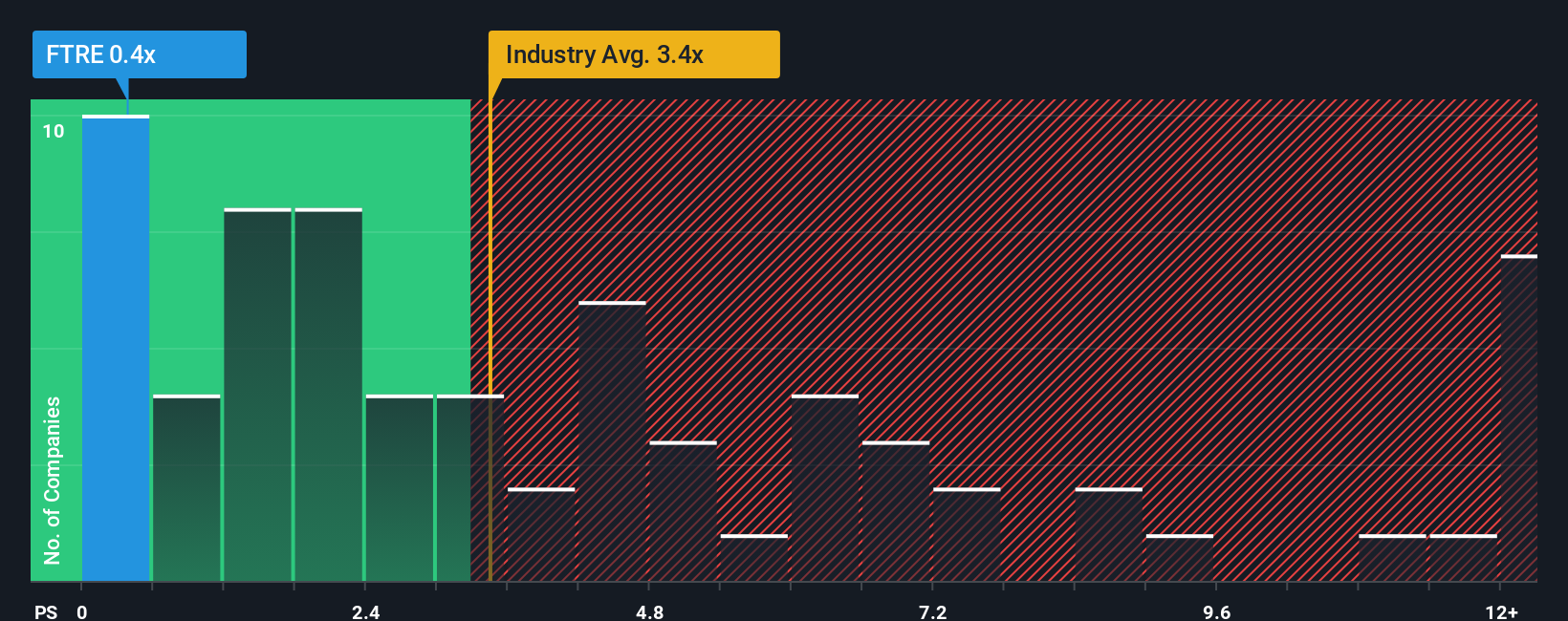

While the narrative view pegs Fortrea at around 14 percent overvalued at 11.21 dollars per share, its 0.4 times price to sales ratio tells a very different story. That is far below US Life Sciences peers at 3.5 times and an 8.1 times peer average, and even below a 1.8 times fair ratio our models suggest the market could gravitate toward. If sentiment truly normalizes, is the real risk missing a rerating rather than overpaying today?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Fortrea Holdings Narrative

If you see the story differently or want to stress test the assumptions yourself, you can build a custom Fortrea view in under three minutes: Do it your way.

A great starting point for your Fortrea Holdings research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in your next opportunity by scanning focused stock shortlists built from hard numbers, not hype, so your capital works smarter.

- Target reliable income streams by reviewing these 14 dividend stocks with yields > 3% that can strengthen your portfolio’s cash flow without chasing risky yields.

- Position yourself early in powerful trends by assessing these 24 AI penny stocks with the financials to support durable, long term growth.

- Capitalize on pricing dislocations by filtering for these 933 undervalued stocks based on cash flows that the market may be overlooking right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:FTRE

Fortrea Holdings

A contract research organization, provides biopharmaceutical product and medical device development solutions to pharmaceutical, biotechnology, and medical device customers worldwide.

Undervalued with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

10 followersusers have followed this narrative

5 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

YE

Yellow_fever on China Starch Holdings ·

China Starch Holdings eyes a revenue growth of 4.66% with a 5-year strategic plan

Fair Value:HK$0.562.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Power Solutions International ·

PSIX The timing of insider sales is a serious question mark

Fair Value:US$37.3845.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Marvell Technology ·

The Great Strategy Swap – Selling "Old Auto" to Buy "Future Light"

Fair Value:US$155.3740.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.6% undervalued

946 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.2% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative