Advertisement

- United States

- /

- Life Sciences

- /

- NasdaqGS:LAB

Fluidigm Corporation (NASDAQ:FLDM) Analysts Just Slashed This Year's Estimates

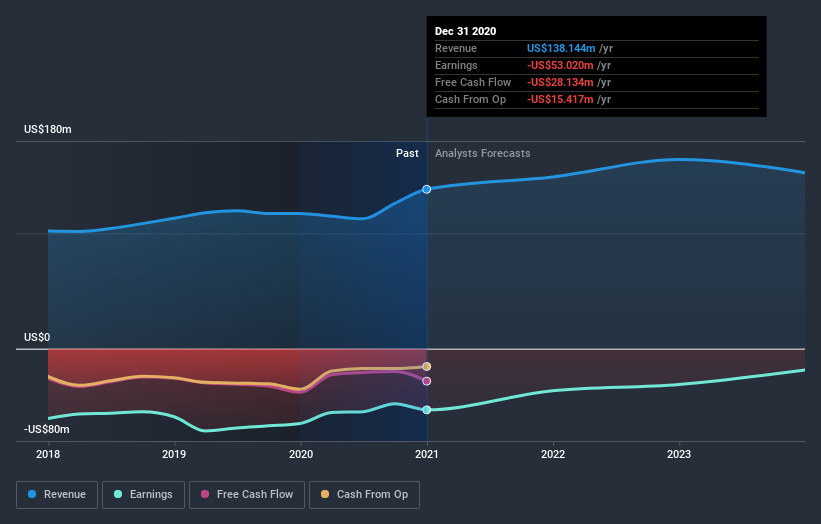

Today is shaping up negative for Fluidigm Corporation (NASDAQ:FLDM) shareholders, with the analysts delivering a substantial negative revision to this year's forecasts. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting the analysts have soured majorly on the business.

Following the downgrade, the latest consensus from Fluidigm's three analysts is for revenues of US$149m in 2021, which would reflect a modest 7.8% improvement in sales compared to the last 12 months. The loss per share is anticipated to greatly reduce in the near future, narrowing 35% to US$0.48. Yet before this consensus update, the analysts had been forecasting revenues of US$198m and losses of US$0.42 per share in 2021. So there's been quite a change-up of views after the recent consensus updates, with the analysts making a serious cut to their revenue forecasts while also expecting losses per share to increase.

Check out our latest analysis for Fluidigm

The consensus price target fell 21% to US$10.33, implicitly signalling that lower earnings per share are a leading indicator for Fluidigm's valuation. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. Currently, the most bullish analyst values Fluidigm at US$14.00 per share, while the most bearish prices it at US$8.00. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. The analysts are definitely expecting Fluidigm's growth to accelerate, with the forecast 7.8% growth ranking favourably alongside historical growth of 3.0% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to see revenue growth of 9.6% next year. It seems obvious that, while the future growth outlook is brighter than the recent past, Fluidigm is expected to grow slower than the wider industry.

The Bottom Line

The most important thing to note from this downgrade is that the consensus increased its forecast losses this year, suggesting all may not be well at Fluidigm. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. With a serious cut to this year's expectations and a falling price target, we wouldn't be surprised if investors were becoming wary of Fluidigm.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. At Simply Wall St, we have a full range of analyst estimates for Fluidigm going out to 2023, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

When trading Fluidigm or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGS:LAB

Standard BioTools

Provides instruments, consumables, reagents, and software services for researchers and clinical laboratories in the Americas, Europe, the Middle East, Africa, and the Asia pacific.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality Assets, Cautious Expansion and Commodity Super-cycle To Deliver Steady Revenue Growth

Fair Value US$20.44|5.2% undervalued

ST

Equity Analyst and Writer

Tullow Oil's Share Price Could Soar Up to 135% if Oil Holds at $70

Fair Value UK£0.45|69.8% undervalued

OI

Community Contributor