David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, FibroGen, Inc. (NASDAQ:FGEN) does carry debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for FibroGen

What Is FibroGen's Net Debt?

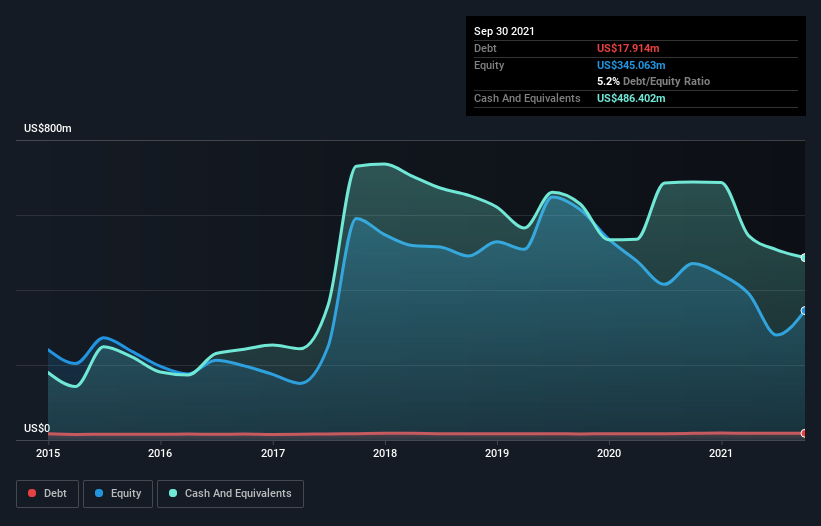

The chart below, which you can click on for greater detail, shows that FibroGen had US$17.9m in debt in September 2021; about the same as the year before. But on the other hand it also has US$486.4m in cash, leading to a US$468.5m net cash position.

How Strong Is FibroGen's Balance Sheet?

We can see from the most recent balance sheet that FibroGen had liabilities of US$209.3m falling due within a year, and liabilities of US$296.1m due beyond that. Offsetting these obligations, it had cash of US$486.4m as well as receivables valued at US$44.0m due within 12 months. So it actually has US$24.9m more liquid assets than total liabilities.

This state of affairs indicates that FibroGen's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the US$1.35b company is struggling for cash, we still think it's worth monitoring its balance sheet. Succinctly put, FibroGen boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine FibroGen's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, FibroGen reported revenue of US$284m, which is a gain of 138%, although it did not report any earnings before interest and tax. So there's no doubt that shareholders are cheering for growth

So How Risky Is FibroGen?

Statistically speaking companies that lose money are riskier than those that make money. And the fact is that over the last twelve months FibroGen lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$66m and booked a US$215m accounting loss. But the saving grace is the US$468.5m on the balance sheet. That means it could keep spending at its current rate for more than two years. The good news for shareholders is that FibroGen has dazzling revenue growth, so there's a very good chance it can boost its free cash flow in the years to come. While unprofitable companies can be risky, they can also grow hard and fast in those pre-profit years. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 3 warning signs for FibroGen you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you're looking to trade FibroGen, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:FGEN

FibroGen

A biopharmaceutical company, discovers, develops, and commercializes therapeutics to treat serious unmet medical needs.

Slight and slightly overvalued.