- United States

- /

- Pharma

- /

- NasdaqGM:EYPT

Revenues Not Telling The Story For EyePoint Pharmaceuticals, Inc. (NASDAQ:EYPT) After Shares Rise 52%

EyePoint Pharmaceuticals, Inc. (NASDAQ:EYPT) shares have had a really impressive month, gaining 52% after a shaky period beforehand. The last month tops off a massive increase of 112% in the last year.

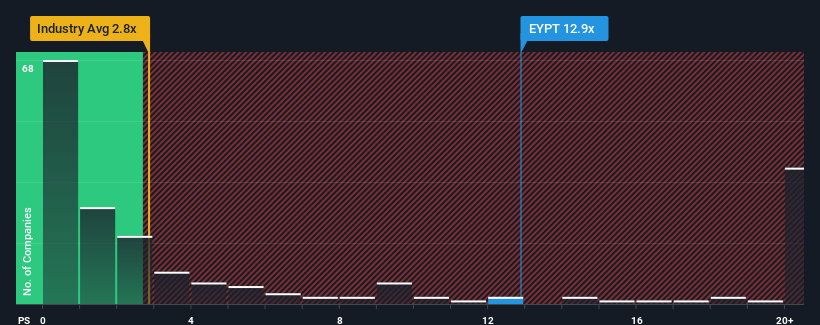

Since its price has surged higher, you could be forgiven for thinking EyePoint Pharmaceuticals is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 12.9x, considering almost half the companies in the United States' Pharmaceuticals industry have P/S ratios below 2.9x. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for EyePoint Pharmaceuticals

What Does EyePoint Pharmaceuticals' Recent Performance Look Like?

Recent times have been advantageous for EyePoint Pharmaceuticals as its revenues have been rising faster than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. If not, then existing shareholders might be a little nervous about the viability of the share price.

Keen to find out how analysts think EyePoint Pharmaceuticals' future stacks up against the industry? In that case, our free report is a great place to start.Is There Enough Revenue Growth Forecasted For EyePoint Pharmaceuticals?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like EyePoint Pharmaceuticals' to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 35%. Revenue has also lifted 29% in aggregate from three years ago, mostly thanks to the last 12 months of growth. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Shifting to the future, estimates from the analysts covering the company suggest revenue growth is heading into negative territory, declining 10.0% each year over the next three years. Meanwhile, the broader industry is forecast to expand by 19% each year, which paints a poor picture.

With this in mind, we find it intriguing that EyePoint Pharmaceuticals' P/S is closely matching its industry peers. Apparently many investors in the company reject the analyst cohort's pessimism and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as these declining revenues are likely to weigh heavily on the share price eventually.

The Bottom Line On EyePoint Pharmaceuticals' P/S

The strong share price surge has lead to EyePoint Pharmaceuticals' P/S soaring as well. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

For a company with revenues that are set to decline in the context of a growing industry, EyePoint Pharmaceuticals' P/S is much higher than we would've anticipated. In cases like this where we see revenue decline on the horizon, we suspect the share price is at risk of following suit, bringing back the high P/S into the realms of suitability. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

And what about other risks? Every company has them, and we've spotted 4 warning signs for EyePoint Pharmaceuticals (of which 2 shouldn't be ignored!) you should know about.

If you're unsure about the strength of EyePoint Pharmaceuticals' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if EyePoint Pharmaceuticals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:EYPT

EyePoint Pharmaceuticals

Engages in developing and commercializing therapeutics to improve the lives of patients with serious retinal diseases.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Community Narratives