If you are eyeing Exelixis and wondering if now is the right moment to get in, you are not alone. Plenty of investors are weighing the same question, especially after seeing the company deliver a solid one-year total return of nearly 47% and an even more impressive three-year gain of over 100%. While there has been some recent turbulence, with a roughly 15% dip over the past month, Exelixis remains up by more than 11% year to date. That kind of performance does not go unnoticed, and it certainly hints at both growth potential and shifting perceptions of risk.

Digging deeper, it is clear that analysts see room for upside too, with the current share price sitting over 18% below consensus price targets. Add in steady annual revenue and income growth, and you can see why the mood around this biotech name feels optimistic despite short-term volatility. For those who look beyond headlines, Exelixis boasts a strong showing on valuation metrics. It is undervalued in 5 out of 6 key checks, giving it a valuation score of 5. That looks compelling on paper, but there is always more to the story than just ratios.

If you are serious about understanding what Exelixis is truly worth, you need to look at how those different valuation approaches work in practice. Next, we will break down the methods used and what they reveal. Later, we will talk about what many investors overlook when figuring out a company’s real value.

Exelixis delivered 46.9% returns over the last year. See how this stacks up to the rest of the Biotechs industry.

Advertisement

Approach 1: Exelixis Cash Flows

A Discounted Cash Flow (DCF) model works by projecting a company’s future cash flows and then discounting them back to their present value. This approach helps estimate what a business is truly worth today based on how much money it can generate over time.

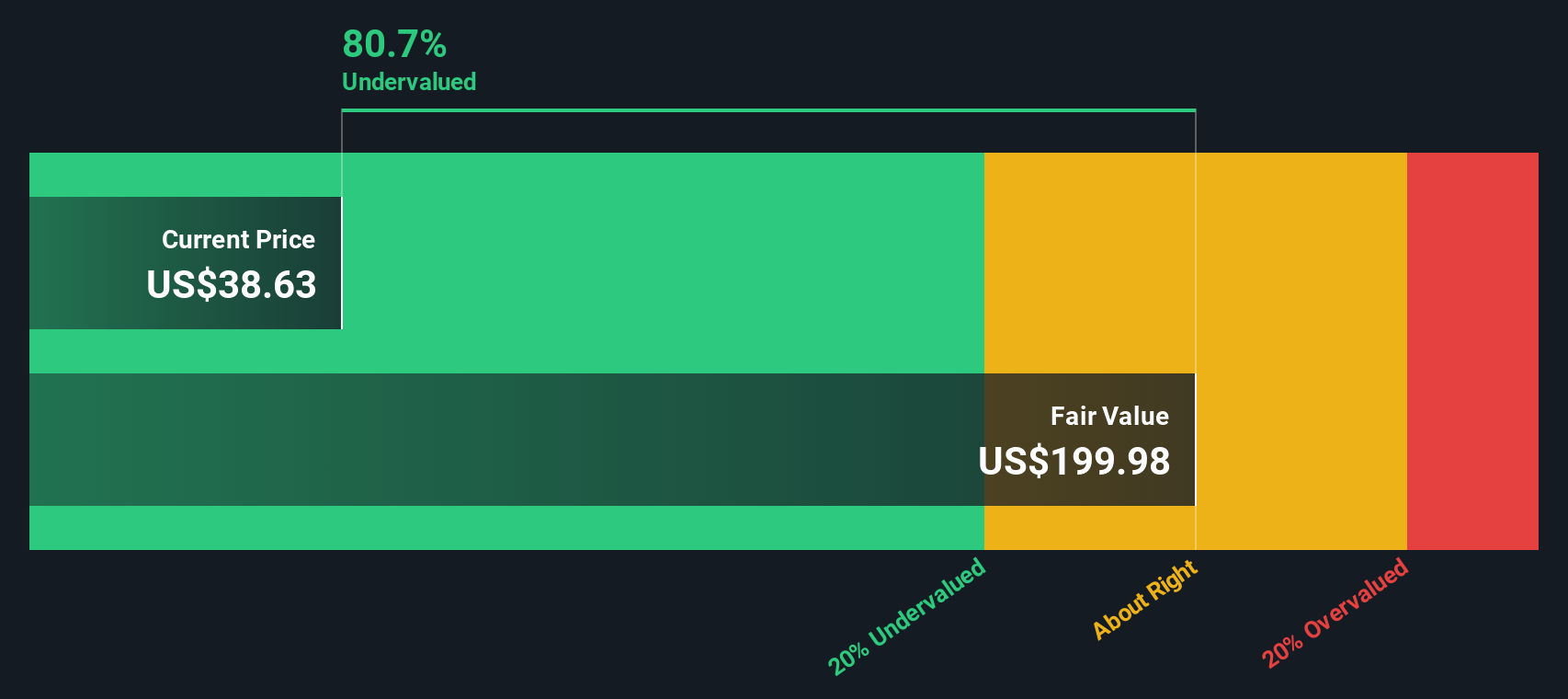

For Exelixis, the most recent twelve months of Free Cash Flow came in at $631 million. Analysts project this figure will grow steadily, reaching as high as $1.77 billion by the end of 2029 as the company's business expands. Looking even further ahead, ten-year projections suggest continued growth, with future free cash flows climbing each year.

Using these numbers in a two-stage Free Cash Flow to Equity model, the estimated intrinsic value of Exelixis is about $200 per share. This represents a significant difference from the current share price, suggesting the stock is 81.1% undervalued compared to where the DCF model sets fair value.

In summary, based on the discounted cash flow analysis, Exelixis appears to be trading well below the potential supported by its projected future cash generation if the forecasts are realized.

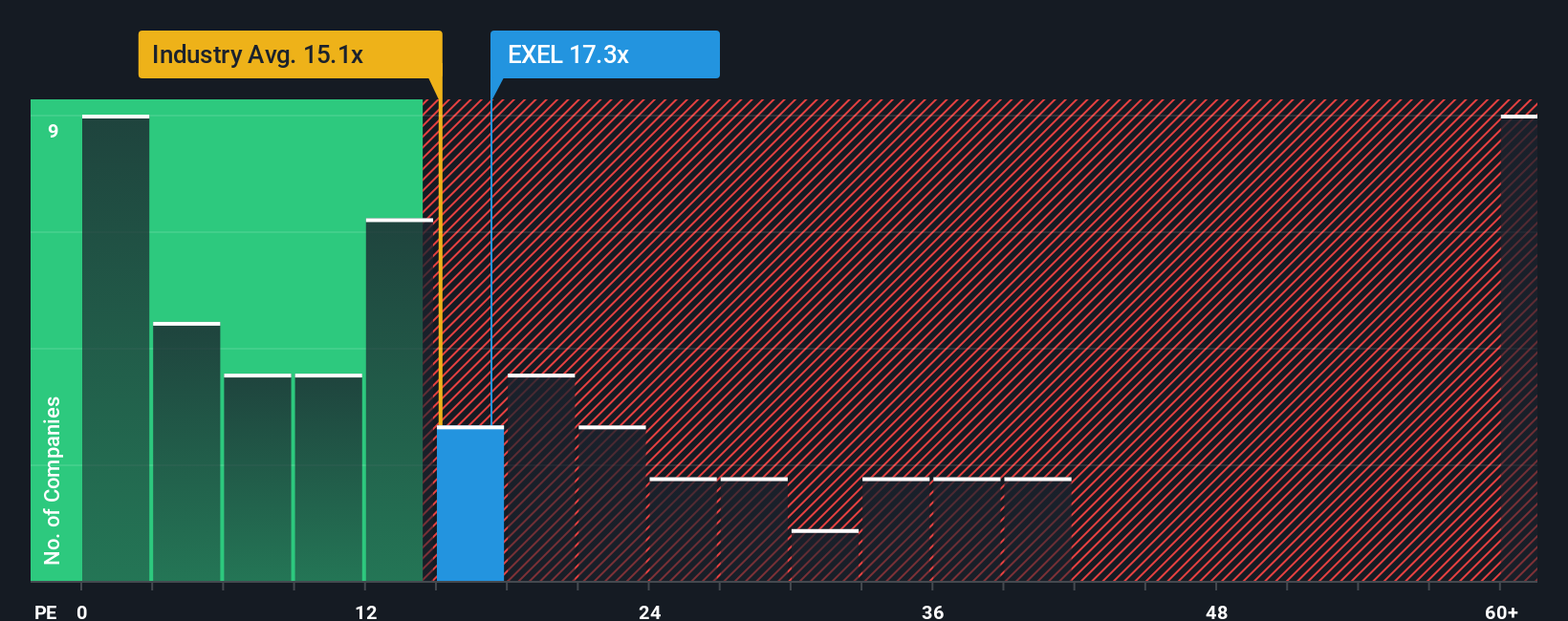

For profitable companies like Exelixis, the Price-to-Earnings (PE) ratio is often the go-to valuation metric. It gives investors a simple way to compare how much they are paying for each dollar of earnings, and works especially well for businesses with a history of consistent profitability.

A company’s PE ratio reflects how the market views its future growth prospects and risks. Typically, higher growth rates and lower risks justify a higher PE, while companies expected to face slowdowns or more uncertainty tend to trade at lower multiples. Understanding how Exelixis’s PE compares to benchmarks can help clarify whether the current price is reasonable.

At present, Exelixis trades at a PE of 16.92x. This is slightly below both the average for its biotech peers at 20.24x and the broader industry average of 16.93x. Simply Wall St’s proprietary Fair Ratio for Exelixis, which incorporates its earnings growth outlook, industry position, and risks, stands at 20.94x. This suggests that Exelixis’s current valuation is under where this model indicates it could be, potentially leaving room for upside if the business meets growth expectations.

Upgrade Your Decision Making: Choose your Exelixis Narrative

Investing is not just about numbers; it is also about the story you believe in for a company. That is where Narratives come in. A Narrative is your personal investment thesis: the story and assumptions you think best explain where Exelixis is headed, tying together its business future (such as growth drivers and risks) with your own forecasts for revenue, earnings, and what is a fair value for the shares today.

Narratives link the “why” behind the numbers with a clear financial forecast and current fair value, turning abstract data into actionable investment ideas. This approach makes it much easier to decide if and when to buy or sell, all within the Simply Wall St platform and its community of millions of investors.

Whenever new news or earnings are released, Narratives are updated dynamically so your assumptions and fair valuation automatically reflect the latest facts.

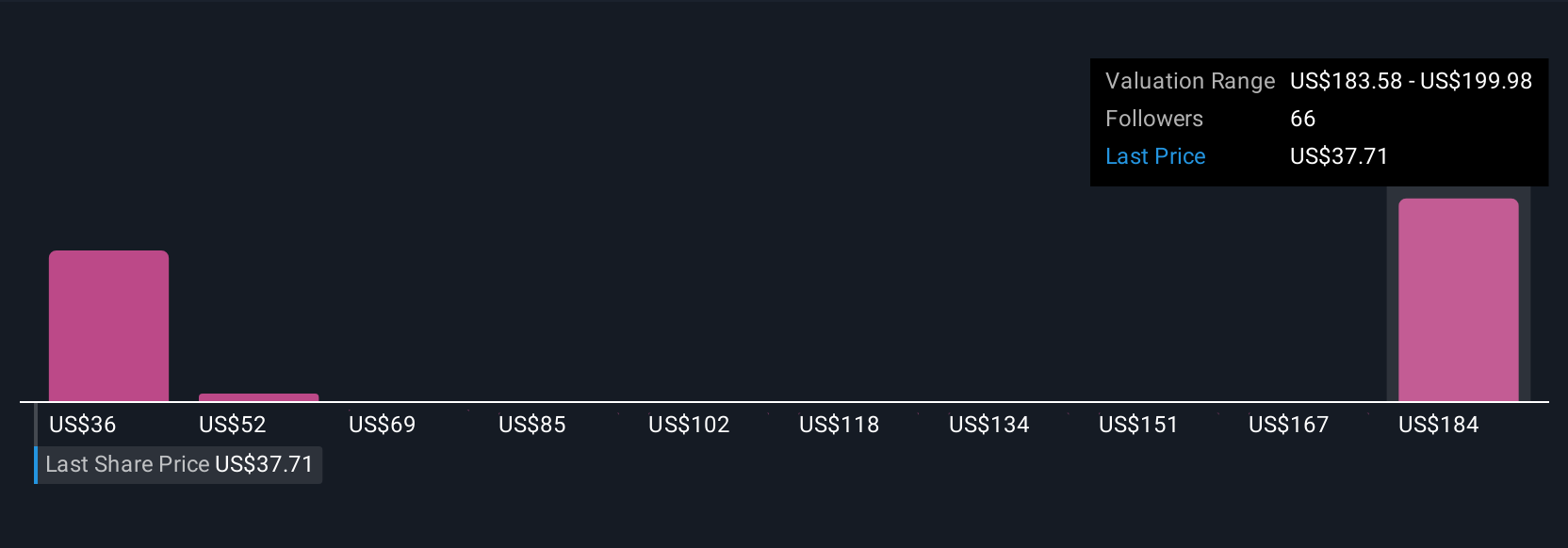

For example, using Exelixis, one investor’s Narrative driven by confidence in global oncology growth sees a price target as high as $60, reflecting bullish revenue and pipeline success. Another investor, focusing on competition or margin risks, may set fair value as low as $36. Your own Narrative helps you decide where you stand.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Exelixis might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

An oncology company, focuses on the discovery, development, and commercialization of new medicines for difficult-to-treat cancers in the United States.