- United States

- /

- Pharma

- /

- NasdaqCM:DERM

A Piece Of The Puzzle Missing From Journey Medical Corporation's (NASDAQ:DERM) 26% Share Price Climb

Journey Medical Corporation (NASDAQ:DERM) shares have continued their recent momentum with a 26% gain in the last month alone. The annual gain comes to 124% following the latest surge, making investors sit up and take notice.

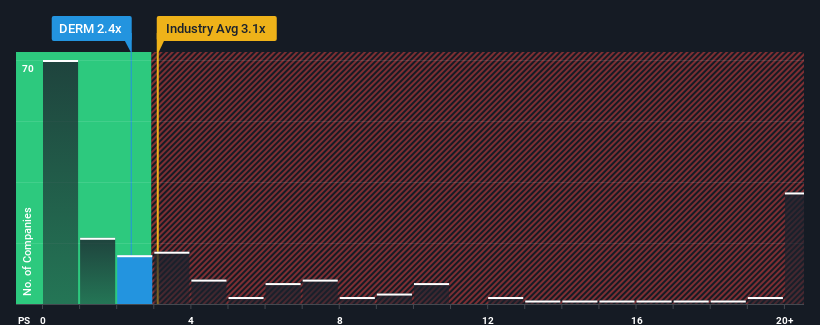

In spite of the firm bounce in price, Journey Medical may still be sending buy signals at present with its price-to-sales (or "P/S") ratio of 2.4x, considering almost half of all companies in the Pharmaceuticals industry in the United States have P/S ratios greater than 3.1x and even P/S higher than 11x aren't out of the ordinary. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Journey Medical

What Does Journey Medical's Recent Performance Look Like?

Journey Medical hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. The P/S ratio is probably low because investors think this poor revenue performance isn't going to get any better. If you still like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Journey Medical.Do Revenue Forecasts Match The Low P/S Ratio?

In order to justify its P/S ratio, Journey Medical would need to produce sluggish growth that's trailing the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 28%. The last three years don't look nice either as the company has shrunk revenue by 2.6% in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 36% per annum during the coming three years according to the four analysts following the company. That's shaping up to be materially higher than the 18% per annum growth forecast for the broader industry.

With this in consideration, we find it intriguing that Journey Medical's P/S sits behind most of its industry peers. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

What Does Journey Medical's P/S Mean For Investors?

Despite Journey Medical's share price climbing recently, its P/S still lags most other companies. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

A look at Journey Medical's revenues reveals that, despite glowing future growth forecasts, its P/S is much lower than we'd expect. There could be some major risk factors that are placing downward pressure on the P/S ratio. While the possibility of the share price plunging seems unlikely due to the high growth forecasted for the company, the market does appear to have some hesitation.

You should always think about risks. Case in point, we've spotted 2 warning signs for Journey Medical you should be aware of, and 1 of them is significant.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

If you're looking to trade Journey Medical, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:DERM

Journey Medical

Focuses on the development and commercialization of pharmaceutical products for the treatment of dermatological conditions in the United States.

High growth potential and good value.

Similar Companies

Market Insights

Community Narratives