Advertisement

- United States

- /

- Biotech

- /

- OTCPK:CLVS.Q

Clovis Oncology, Inc. (NASDAQ:CLVS) Consensus Forecasts Have Become A Little Darker Since Its Latest Report

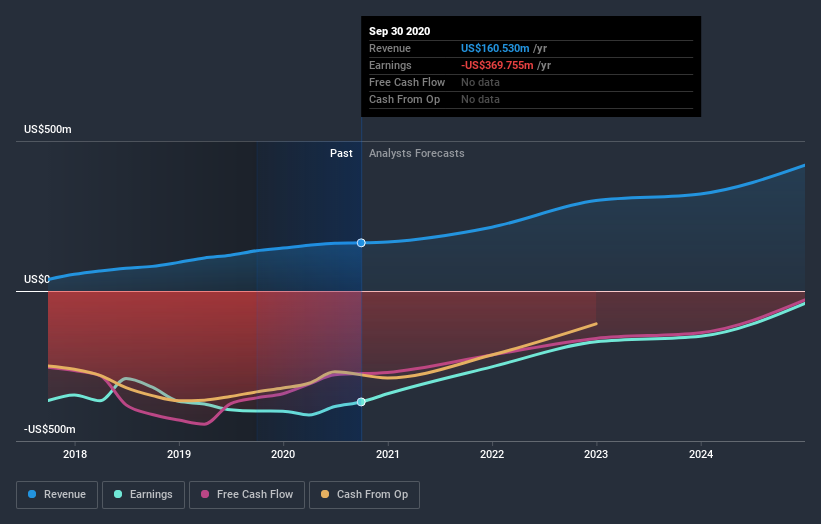

It's been a mediocre week for Clovis Oncology, Inc. (NASDAQ:CLVS) shareholders, with the stock dropping 14% to US$4.26 in the week since its latest third-quarter results. The results weren't stellar - revenue fell 9.1% short of analyst estimates at US$39m, although statutory losses were a relative bright spot. The per-share loss was US$0.89, 11% smaller than the analysts were expecting prior to the result. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Check out our latest analysis for Clovis Oncology

Taking into account the latest results, the current consensus from Clovis Oncology's five analysts is for revenues of US$212.7m in 2021, which would reflect a major 33% increase on its sales over the past 12 months. Losses are predicted to fall substantially, shrinking 47% to US$2.65. Yet prior to the latest earnings, the analysts had been forecasting revenues of US$235.2m and losses of US$2.67 per share in 2021.

The average price target fell 17% to US$7.20, with the analysts clearly concerned about the weaker revenue outlook and expectation of ongoing losses. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values Clovis Oncology at US$15.00 per share, while the most bearish prices it at US$3.00. We would probably assign less value to the analyst forecasts in this situation, because such a wide range of estimates could imply that the future of this business is difficult to value accurately. With this in mind, we wouldn't rely too heavily the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would highlight that Clovis Oncology's revenue growth is expected to slow, with forecast 33% increase next year well below the historical 48%p.a. growth over the last five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 20% next year. Even after the forecast slowdown in growth, it seems obvious that Clovis Oncology is also expected to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts reconfirmed their loss per share estimates for next year. They also downgraded their revenue estimates, although industry data suggests that Clovis Oncology's revenues are expected to grow faster than the wider industry. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

With that in mind, we wouldn't be too quick to come to a conclusion on Clovis Oncology. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple Clovis Oncology analysts - going out to 2024, and you can see them free on our platform here.

That said, it's still necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with Clovis Oncology (at least 1 which is significant) , and understanding these should be part of your investment process.

When trading Clovis Oncology or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About OTCPK:CLVS.Q

Clovis Oncology

Clovis Oncology, Inc., a biopharmaceutical company, focuses on acquiring, developing, and commercializing anti-cancer agents in the United States, Europe, and internationally.

Slightly overvalued with weak fundamentals.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|29.9% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.9% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|64.1% undervalued

ME

Community Contributor