- United States

- /

- Life Sciences

- /

- NasdaqCM:BLFS

Is There Still Opportunity in BioLife Solutions After 15% Share Price Gain in 2025?

Reviewed by Bailey Pemberton

Thinking about what to do next with BioLife Solutions stock? You are not alone. Over the past year, shares have quietly climbed 15.6%, and while that performance might catch your eye, it is the bigger context that makes this stock so interesting right now. Investors have watched it rebound 6.8% in just the last 30 days, adding to a 4.4% gain year-to-date. Yet, when looking further back, the five-year total return lags at -5.9%, painting a far more complex picture. So, what is driving this mixed bag of returns?

Recent shifts in sentiment across the biotech industry, combined with ongoing advancements in cell and gene therapy storage and delivery, have fueled speculation among analysts that BioLife Solutions is well-positioned for future growth. Part of that optimism is rooted in changing risk appetites, as more investors bet on companies supporting the broader life sciences ecosystem, even if near-term volatility remains a reality.

If you are looking for a quick answer on whether the stock is undervalued, here is a sneak peek: BioLife Solutions scores a 2 out of 6 on our valuation scale. That means it checks the box for undervaluation on two of six key metrics we track. But those numbers do not tell the whole story on their own.

As we break down the different valuation approaches, you will see why this score matters and what it could mean for your portfolio. Stick around, because at the end, we will explore an even smarter, more holistic way to think about valuation for a company like BioLife Solutions.

BioLife Solutions scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: BioLife Solutions Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting its future free cash flows and discounting them back to today’s dollars. This approach helps investors look beyond current earnings and instead focus on the business’s long-term cash-generating potential.

For BioLife Solutions, the most recent Free Cash Flow stands at $6.1 Million. Analysts project rapid growth, with Free Cash Flow expected to reach $57.5 Million by 2029. The next five years use direct analyst estimates, while projections for later years are extrapolated to provide an extended view of the company’s potential trajectory.

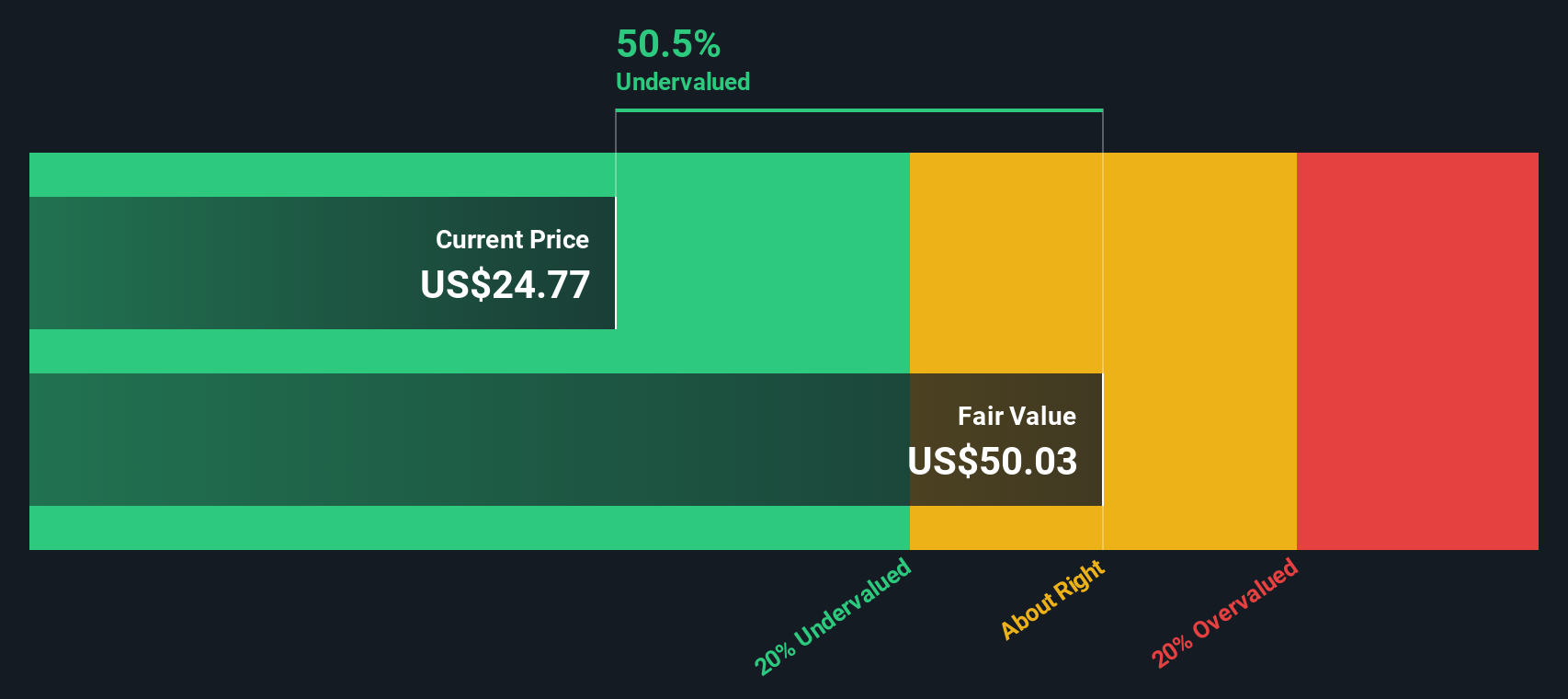

After modeling these projections and discounting them back to the present, the DCF analysis assigns BioLife Solutions an intrinsic value of $42.37 per share. Based on this model, the stock currently trades at a 35.5% discount, indicating it is significantly undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests BioLife Solutions is undervalued by 35.5%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: BioLife Solutions Price vs Sales

For companies like BioLife Solutions that are not yet profitable on the bottom line, the Price-to-Sales (P/S) ratio is often the most appropriate valuation tool. This metric helps investors assess how the market values the company relative to its sales, providing insight especially when earnings are negative or volatile.

Growth potential and perceived business risks both impact what counts as a "normal" or fair P/S ratio. A higher ratio can be justified when the market expects rapid sales growth or sees the company as a leading innovator. Conversely, slower growth or greater uncertainties push that fair multiple lower.

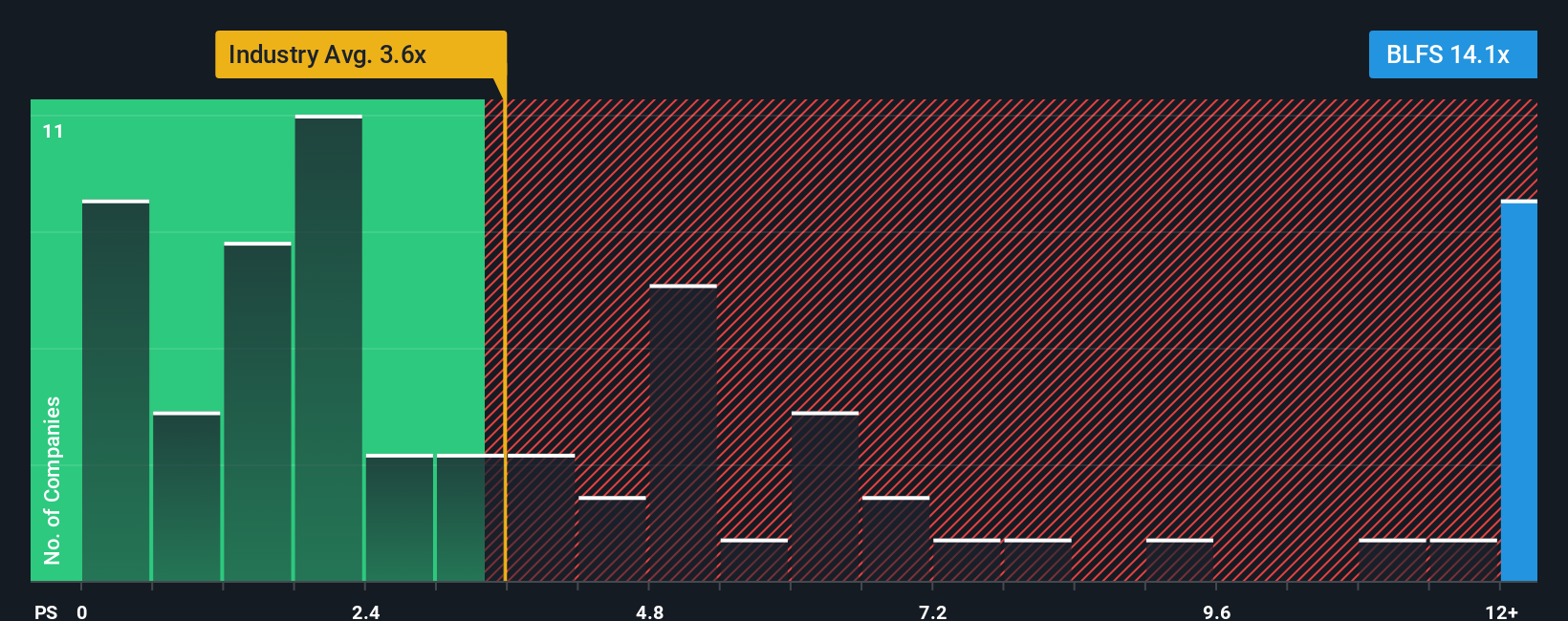

BioLife Solutions currently trades at a P/S ratio of 14.0x, which is significantly higher than both the life sciences industry average of 3.4x and the peer group average of 2.0x. At first glance, this premium might suggest overvaluation, but headline comparisons only tell part of the story.

Simply Wall St’s proprietary Fair Ratio aims to give a smarter benchmark. Unlike a simple peer or industry average, the Fair Ratio for BioLife Solutions, calculated at 4.9x for this company, blends in considerations like future growth forecasts, profit margins, business risks, and even factors such as industry characteristics and market cap. Because it adapts to the company’s specific profile, it is a much more targeted assessment of fair value than a one-size-fits-all average.

Comparing the Fair Ratio of 4.9x to the current P/S of 14.0x, BioLife Solutions is trading well above what our model considers justified for its situation right now.

Result: OVERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your BioLife Solutions Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. A Narrative is your unique investment story, connecting the facts and forecasts behind BioLife Solutions with your own assumptions about fair value, future revenue, earnings, and margins.

Narratives make investing easier and more approachable by letting you translate a company’s story into clear financial forecasts and a resulting fair value, all in one place. Available to millions of investors right inside Simply Wall St’s Community page, Narratives help you see not just what a company is worth, but why, based on your convictions or different perspectives from other investors.

When you create a Narrative, you can instantly compare your estimated Fair Value to today’s share price, so you will know if it is time to buy, hold, or sell according to your view. Best of all, Narratives are dynamic. If new information comes in, like earnings updates or industry news, your Narrative updates automatically, ensuring your forecasts and decisions stay current.

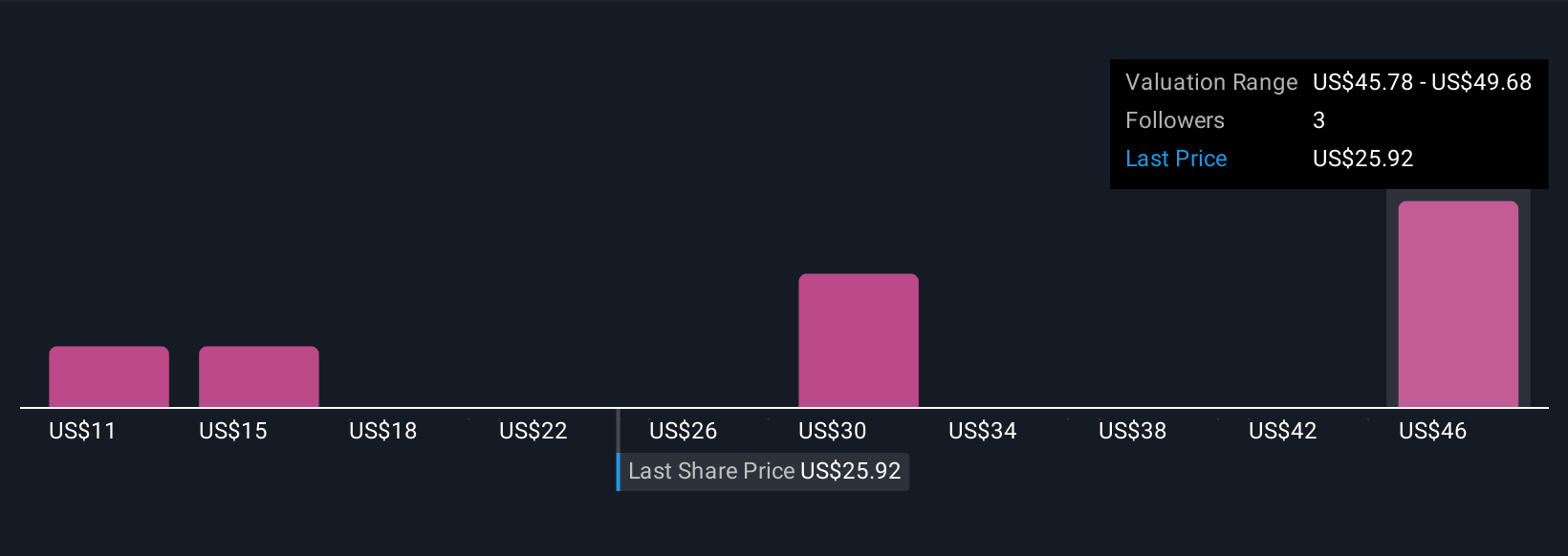

For example, one investor might believe BioLife Solutions is poised for long-term growth from its regenerative medicine opportunities and set a high fair value of $31.3, while a more cautious perspective could highlight risks around customer concentration and margin pressure, leading to a much more conservative estimate.

Do you think there's more to the story for BioLife Solutions? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if BioLife Solutions might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:BLFS

BioLife Solutions

Develops, manufactures, and markets bioproduction products and services for the cell and gene therapy (CGT) industry in the United States, Europe, the Middle East, Africa, and internationally.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Salesforce Stock: AI-Fueled Growth Is Real — But Can Margins Stay This Strong?

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)