Advertisement

- United States

- /

- Biotech

- /

- NasdaqGS:BEAM

Industry Analysts Just Made A Massive Upgrade To Their Beam Therapeutics Inc. (NASDAQ:BEAM) Revenue Forecasts

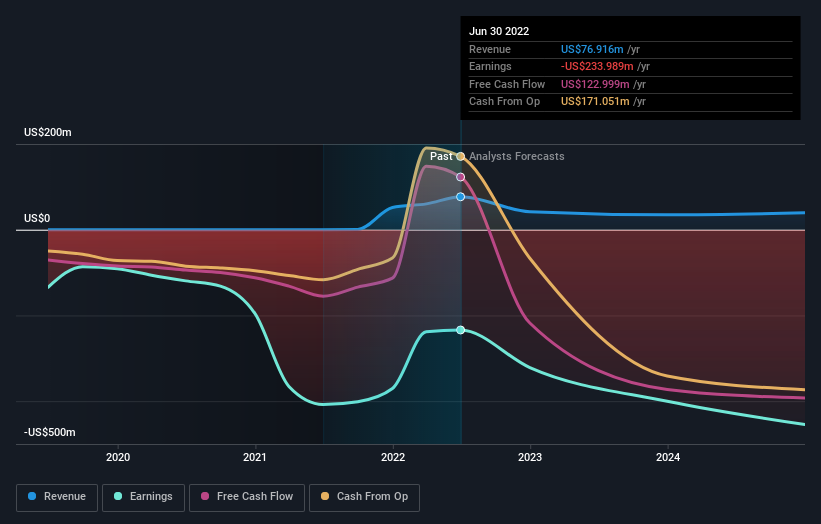

Beam Therapeutics Inc. (NASDAQ:BEAM) shareholders will have a reason to smile today, with the analysts making substantial upgrades to next year's statutory forecasts. The analysts have sharply increased their revenue numbers, with a view that Beam Therapeutics will make substantially more sales than they'd previously expected.

Following the latest upgrade, the twelve analysts covering Beam Therapeutics provided consensus estimates of US$47m revenue in 2023, which would reflect a disturbing 39% decline on its sales over the past 12 months. Losses are supposed to balloon 59% to US$5.41 per share. Yet before this consensus update, the analysts had been forecasting revenues of US$35m and losses of US$5.39 per share in 2023. So there's definitely been a change in sentiment in this update, with the analysts upgrading next year's revenue estimates, while at the same time holding losses per share steady.

Check out the opportunities and risks within the US Biotechs industry.

The consensus price target held steady at US$86.50 despite the upgrade to revenue forecasts and ongoing losses. Analysts seem to think the business is otherwise performing roughly in line with expectations. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic Beam Therapeutics analyst has a price target of US$145 per share, while the most pessimistic values it at US$60.00. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Beam Therapeutics' past performance and to peers in the same industry. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 33% by the end of 2023. This indicates a significant reduction from annual growth of 155% over the last three years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 14% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Beam Therapeutics is expected to lag the wider industry.

The Bottom Line

The highlight for us was that the consensus reduced its estimated losses next year, perhaps suggesting Beam Therapeutics is moving incrementally towards profitability. Pleasantly, analysts also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow slower than the wider market. Seeing the dramatic upgrade to next year's forecasts, it might be time to take another look at Beam Therapeutics.

Analysts are definitely bullish on Beam Therapeutics, but no company is perfect. Indeed, you should know that there are several potential concerns to be aware of, including dilutive stock issuance over the past year. For more information, you can click through to our platform to learn more about this and the 3 other concerns we've identified .

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if Beam Therapeutics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:BEAM

Beam Therapeutics

A biotechnology company, engages in the development of precision genetic medicines for patients suffering from serious diseases in the United States.

Flawless balance sheet with limited growth.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|22.7% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|14.2% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor