Amylyx Pharmaceuticals (AMLX) just landed a spot in the S&P Pharmaceuticals Select Industry Index, and that news is turning heads for good reason. Being added to an industry index is more than a headline. It usually means new institutional eyes on the stock and the possibility of more trading volume ahead. This change could be a game changer in terms of how Wall Street views Amylyx and its place in the pharma landscape.

The timing is interesting too. Over the past year, Amylyx Pharmaceuticals has seen its stock rise around 4%, with momentum especially strong in the past month and through the recent quarter, with returns topping 43% and 108% respectively. That follows not just the index news but a recent $175 million equity offering, showing the company is raising capital at a time when confidence seems to be building. All of this comes on the heels of annual revenue growth, though profitability remains out of reach.

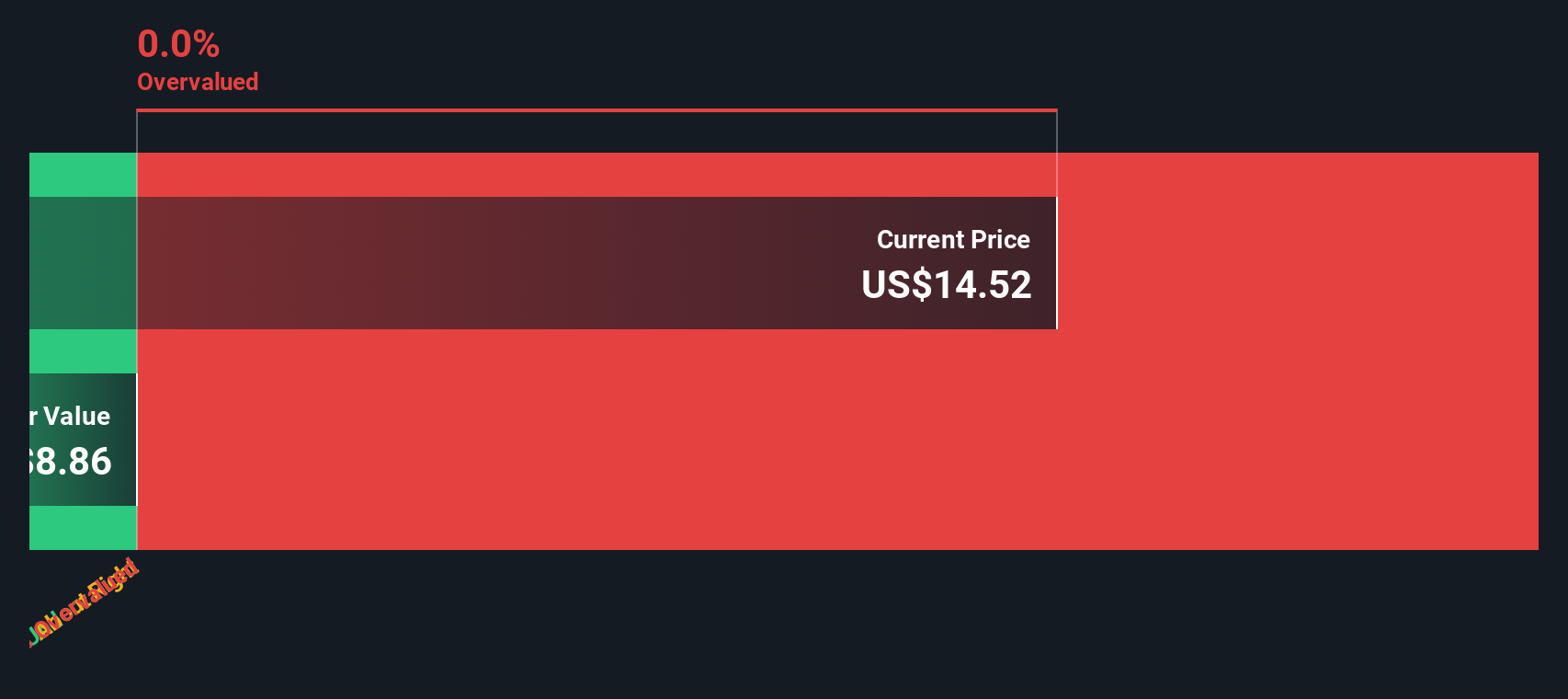

So after a stretch of steady upward price action and a major nod from the index committee, is this a real buying opportunity, or has the market already priced in the next phase of Amylyx’s growth?

Advertisement

Price-to-Book of 8.5x: Is it justified?

Based on the latest data, Amylyx Pharmaceuticals is trading at a Price-to-Book (P/B) ratio of 8.5x. This is notably higher than both the US Pharmaceuticals industry average of 2.1x and its peer group average of 2.5x. The current market price is therefore much higher than the book value of the company's assets.

The Price-to-Book ratio measures a company's market value compared to its book value. This metric is commonly used for asset-heavy industries like pharmaceuticals and biotech. A high P/B ratio can reflect investor confidence in future growth. However, for unprofitable companies, it may raise concerns about overvaluation.

Amylyx is not profitable and has minimal revenue, yet trades at a high multiple. Investors could be paying a premium for anticipated future growth or pipeline developments that may not occur as quickly as expected. The elevated ratio indicates that the market is pricing in significant optimism.

However, challenges remain if Amylyx's revenue growth slows or if clinical trials face setbacks. Either of these could undermine the current market optimism.

Our DCF model takes future cash flows into account. However, right now, there is not enough data to calculate a fair value using this approach. As a result, the high market price is supported only by current market optimism. Could this signal risk ahead, or is the market seeing something more?

If you have a different take on these numbers or want to dig into the details yourself, it's easy to craft your own view in just a few minutes. Do it your way

A great starting point for your Amylyx Pharmaceuticals research is our analysis highlighting 1 key reward and 4 important warning signs that could impact your investment decision.

Ready for Your Next Investment Move?

Don’t let opportunity pass you by. If you want to be ahead of the curve, Simply Wall Street’s tailored screeners make finding standout stocks quick and effective.

Spot companies shaking up artificial intelligence by jumping straight into AI penny stocks for a look at tomorrow’s game changers today.

Chase higher income potential and stability by starting with dividend stocks with yields > 3% to find stocks offering attractive yields over 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks

A clinical-stage pharmaceutical company, engages in the discovery and development of treatment options for neurodegenerative diseases and endocrine conditions in the United States.