- United States

- /

- Entertainment

- /

- NYSE:SKLZ

Skillz (NYSE:SKLZ) Is In Line with Growth, and has Enough Capital to Ramp Up Development

Young companies such as Skillz (NYSE:SKLZ), need capital in order to reach their full potential and profitability. Debt can often be risky and is more appropriate for already profitable companies. That is why cash from investors is a much better option while a company grows.

In this article, we will go over the highlights of Skillz's Q2 earnings and analyze their cash capacity for funding operations and growth.

Q2 Earnings Highlights

- Quarterly revenue grew to US$89.5m, up 52% from Q2 in 2020

- Gross Margin was 95%, in line with previous year

- Net Loss at US$79.6m, up from US$20.2m from Q2 in 2020

- Cash on balance sheet of US$692.8m and no debt

The company is in line and slightly exceeding analyst revenue estimates. It is worth noting that short term analyst estimates are almost a complete reflection of company guidance, which is sometimes set a bit lower just so that businesses can report a "beat" on estimates.

The Gross Margin signals a very low cost of goods sold - even though the margin is quite high, this is not that impressive since Skillz is in the software industry where the marginal cost to create an extra product is very low.

Net loss is increasing, as is expected with young companies that are funding growth. The question for investors is whether Skillz is investing efficiently in future growth? The no debt and available cash is a great composition for a young company!

Now let's analyze the cash runway for Skillz.

We define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth.

Let's start with an examination of the business' cash, relative to its cash burn.

See our latest analysis for Skillz

How Long Is Skillz's Cash Runway? - Updated to Q2

A cash runway is defined as the length of time it would take a company to run out of money if it kept spending at its current rate of cash burn.

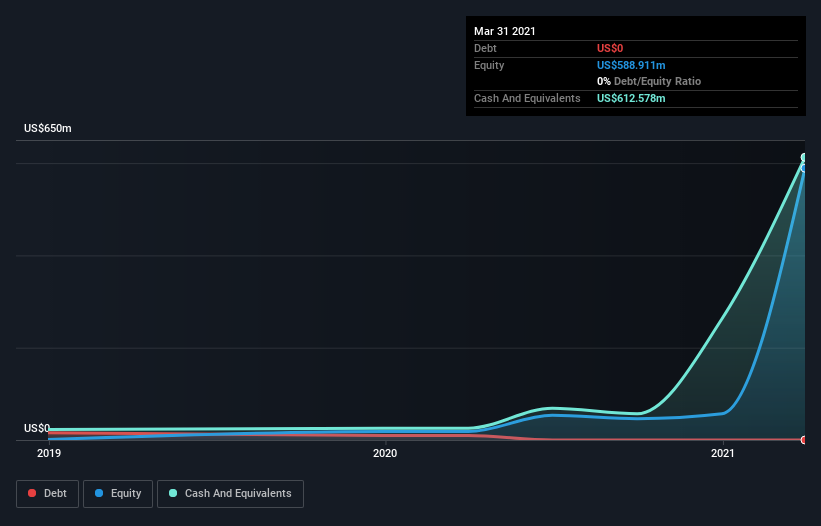

In Q2, 2021, Skillz had US$692m in cash, and was debt-free.

Looking at the last 4 quarters ending in June 2021, the company burnt through US$98.2m.

That means it had a cash runway of about 7 years as of June 2021.

Even though this is but one measure of the company's cash burn, the thought that the company can sustain itself for developing and growing another 7 years gives investors assurance of capability and flexibility.

The image below shows how its cash balance has been changing over the last few years.

How Well Is Skillz Growing?

Notably, Skillz actually ramped up its cash burn very hard and fast in 2020, by 187%, signifying heavy investment in the business.

While that certainly gives us pause for thought, we take a lot of comfort in the strong annual revenue growth of 98%, and the 2nd quarter revenue growth of 58% year over year.

Clearly, however, the crucial factor is whether the company will grow its business going forward. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

How Easily Can Skillz Raise Cash?

There's no doubt Skillz seems to be in a fairly good position, when it comes to managing its cash burn, but even if it's only hypothetical, it's always worth asking how easily it could raise more money to fund growth.

Companies can raise capital through either debt or equity. Many companies end up issuing new shares to fund future growth.

By comparing a company's annual cash burn to its total market capitalization, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Since it has a market capitalization of US$5.5b, Skillz's US$98.2m in cash burn equates to about 1.7% of its market value.

That means it could easily issue a few shares to fund more growth.

Key Takeaways

As you can probably tell by now, we're not too worried about Skillz's cash burn. The company has enough room to pick smart growth moves and invest in multiple aspects, such as development, research, marketing, etc.

However, when it comes to growth via new acquisitions, it can be hard to get right, and they are more a feature of older companies as young companies are pressured to grow within their own business model. There are success stories from acquisitions by young companies, but it does prompt caution for investors.

Looking at the big picture, Skillz is in line with expectations and revenue growth stands out as evidence that the company is well on top of its spending.

Taking an in-depth view of risks, we've identified 3 warning signs for Skillz that you should be aware of before investing.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies, and this list of stocks growth stocks (according to analyst forecasts)

If you're looking to trade Skillz, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NYSE:SKLZ

Skillz

Operates a mobile game platform in the United States, Israel, China, Malta, and internationally.

Excellent balance sheet low.

Similar Companies

Market Insights

Community Narratives