Advertisement

- United States

- /

- Entertainment

- /

- NYSE:SKLZ

Investors might want to Weigh the Potential of Skillz (NYSE:SKLZ) Before their New Titles Start Selling

Skillz Inc. (NYSE:SKLZ) has lost a significant portion of market cap and is down some 74% from its February highs. When we look at situations like this, we want to know if the shift is permanent or temporary, and what are the possible catalysts that can change the outcome. In this article, we will look at some of Skillz's fundamentals and try to weigh the risks with the opportunities for growth.

With a market capitalization of US$4.5b, Skillz is rather large, while EpicGames, a competitor that focuses on the mobile gaming industry, has been recently valued at US$29b and raised more than US$1b in private investments. This shows us what potentially Skillz aspires to become, and for investors this shows the possible upside if some good things happen in the future.

One aspect, which the CEO of Skillz mentioned on CNBC, is that the mobile gaming industry is a growing market and that the company will derive some growth just by being a part of that market. He noted that the industry is expected to increase from a US$86b in 2020, to US$ 160b in 2025. While it is great to be a part of a growing market, generating meaningful revenues might prove a bit harder than expected. In regard to being in a large market, the CEO also mentioned that they expect to enter India's market by Q4 2021, which should give them access to a rather large, albeit a low margin customer base.

One of the possible catalysts for future growth might come from the launch of their sports NFL mobile game, which is set to launch before the opening of NFL's 2022 (April) season. In the development of the NFL game, they had a 100+ game proposals and accepted 14 semifinalists in their shortlist to developers.

Currently, the highest hope resides in their Big Buck Hunter: Marksman title, which is available on iOS.

When looking at their product portfolio, it seems that most of the value of the company lays in the future. Additionally, the mobile gaming industry seems to be quite unpredictable, and it is hard to estimate which games will take off to be major winners.

In both Android and Apple app stores, we can see that there is a short selection of highly popular games which are financially viable, and a very long-tailed distribution of failed projects. While Skillz's business model suggests some innovation, it has not been proven beyond card games, and it seems that investors are starting to value the company closer to what it is currently worth, rather than to what it can potentially become.

While predicting the success of a title is difficult, investors that enter at a lower valuation and wait out a possible success, can be surprised by a high return. Otherwise, it is hard to see the market cap moving any higher without a hit title.

Looking at the fundamentals, we can gain more insight as to how the company is planning to achieve growth. First, let's see where the company is at the moment:

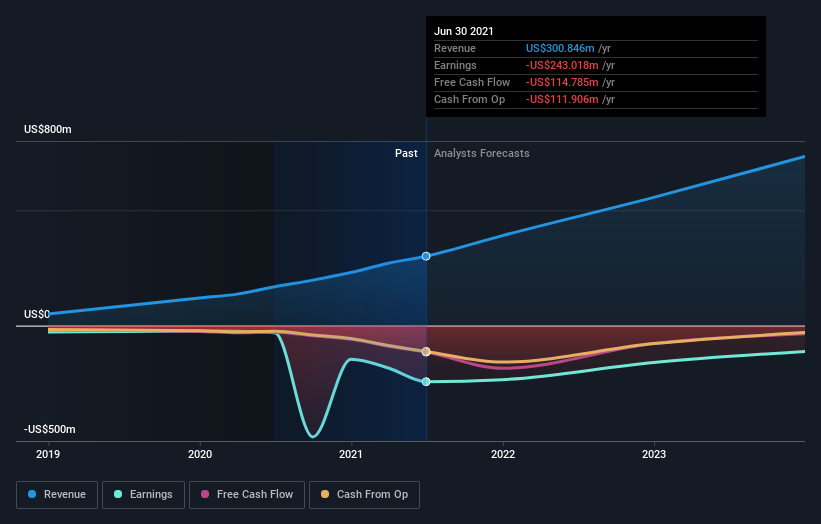

Current trailing 12 month revenue is at US$300m, analysts seem to be uncertain of the future, and just opted to extrapolate past growth.

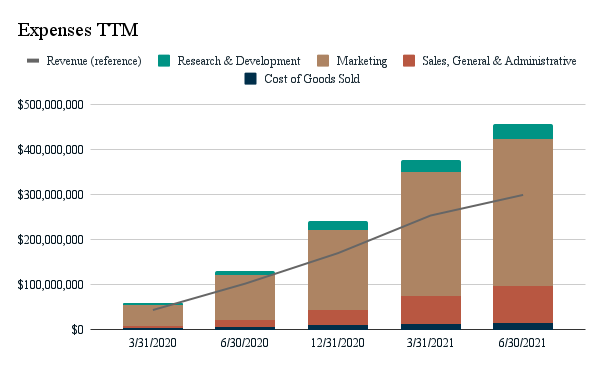

The cost structure is also important for the company, because it will give us a picture of the growth strategy for Skillz and how long can they keep up current operations.

The chart above outlines a heavy tilt towards marketing spend, which can be good if the new users have high lifetime value (they stick with the games for a long time), but could be problematic if the company's best games are yet to come, and they are spending - in a possibly inefficient manner, a lot of funds which could be utilized in better days.

The marketing spend opens the question of cash burn. We want to be confident that the company can develop and continue operating for enough time in order to maximize the chances that it finds one or more hit games. When looking at the cash balance, it seems that Skillz has US$692m and is loosing around US$115m in free cash flows. This means that without additional financing and expenses ramp up, the company has cash reserves for about 6 more years. This calms down the concerns for long term operations, but leaves the question of efficient investing still open.

Lastly, a few words on share movements. There are 2 things of note recently:

- The company used a shelf registration to issue new shares between the 16th and 20th August. The shares were issued at US$10.5 per share, which could mean that the company needs the funds, or that they do not see much upside in the near future. Any of these options may not be good for investors.

- The ARKK innovation ETF, was considered one of the loudest promotors of the company. However, their most recent filings suggest that they have further decreased their position in Skillz and now own 13m shares, down from 24m in 30 Jun.

If you want to know the latest big moves by insiders (and there are some), you can click here to see if those insiders have been buying or selling.

Key Takeaways

Skillz is in front of a very uncertain landscape. The company has its hopes placed on a few new and upcoming titles, along with the enlargement of the mobile gaming industry.

Investors seem to be taking a more cautionary approach regarding the company, and may be waiting for signals that will allow them to better quantify the future of Skillz.

The expense structure of the company is heavily tilted towards marketing spending, however there is a risk that this might be more of an operating expense, rather than a capital expense which will yield long term growth in the future. The bright side is that the company has no debt and plenty of cash to finance even more aggressive expense policies.

Recent share related decisions, and insider moves indicate some pessimistic outlook for the future of the stock.

If you would prefer discover what analysts are predicting in terms of future growth, do not miss this free report on analyst forecasts.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NYSE:SKLZ

Skillz

Operates a mobile game platform in the United States, Israel, China, Malta, and internationally.

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|41.9% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|14.1% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$613.59|1.3% undervalued

AN

Based on Analyst Price Targets