Advertisement

- United States

- /

- Interactive Media and Services

- /

- NYSE:PINS

Will Analyst Optimism on Pinterest’s (PINS) Ad Growth Reveal a New Phase in Its Evolution?

Simply Wall St

Reviewed by Sasha Jovanovic

- Pinterest recently attracted positive analyst attention, with several firms expressing optimism about its prospects and raising their ratings ahead of the company's upcoming earnings report.

- This wave of favorable sentiment has centered on improved ad revenue forecasts and a growing user base, reflecting confidence in Pinterest’s evolving business model.

- We'll examine how surging analyst optimism, particularly around Pinterest's improving ad business, could reshape the company’s investment narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Pinterest Investment Narrative Recap

To be a shareholder in Pinterest, an investor needs to believe in the platform’s ability to drive sustained revenue growth through expanding user engagement, innovative ad products, and improvements in monetization, particularly as AI-powered ad tools gain traction. The latest wave of analyst optimism appears to reinforce the view that ad revenue improvements remain the key short-term catalyst, while ongoing competition from digital giants represents the most crucial risk; however, this news does not fundamentally alter those priorities.

Relevant to the upbeat analyst sentiment, Pinterest’s Q2 results delivered a 16.9% year-over-year sales increase and guidance for similarly strong Q3 revenue growth, with both metrics reinforcing market confidence in the company's expanding ad business. These financial trends provide a clearer backdrop for analyst upgrades and help validate improved ad revenue forecasts as a leading catalyst as earnings season approaches.

But on the flip side, investors should not overlook the ongoing pressure from rivals potentially eroding Pinterest’s user growth and...

Read the full narrative on Pinterest (it's free!)

Pinterest's outlook anticipates $5.9 billion in revenue and $1.0 billion in earnings by 2028. This scenario assumes a 14.6% annual revenue growth rate but a $0.9 billion decline in earnings from the current $1.9 billion.

Uncover how Pinterest's forecasts yield a $43.58 fair value, a 43% upside to its current price.

Exploring Other Perspectives

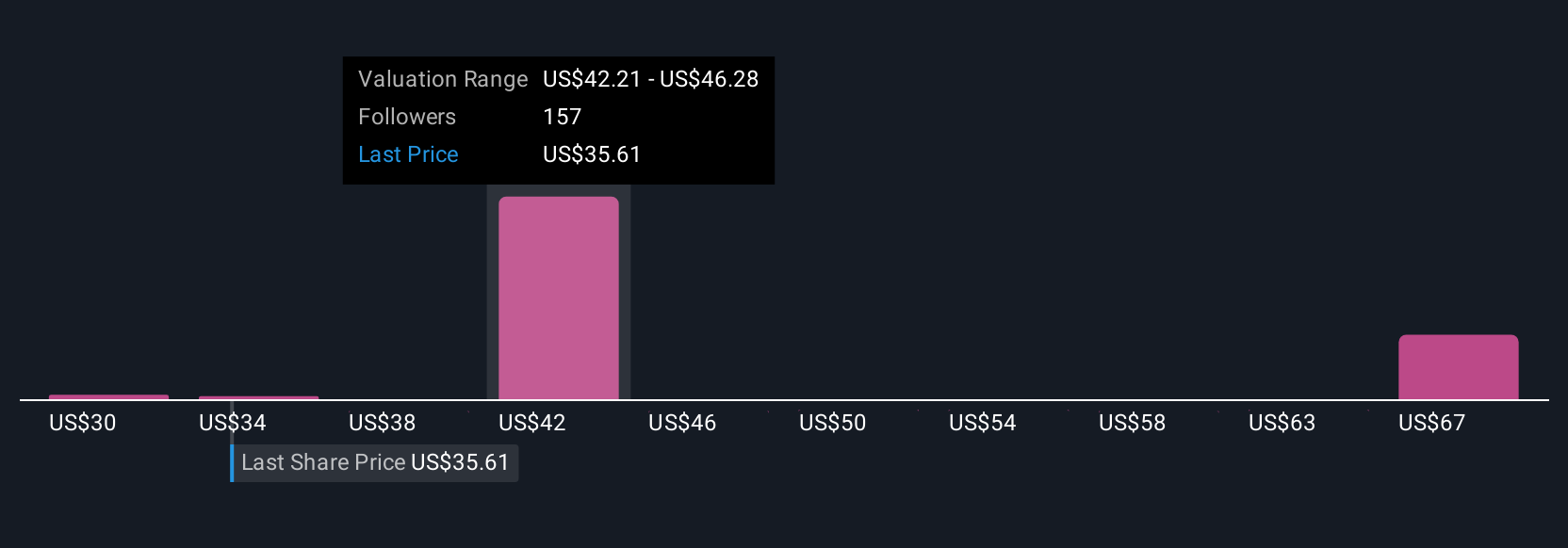

Fair value estimates from 19 Simply Wall St Community members span from US$30 to US$72.76 per share, with opinions clustering across nine price buckets. As you weigh these diverse outlooks, remember that heightened competition from other platforms could have significant implications for future earning power.

Explore 19 other fair value estimates on Pinterest - why the stock might be worth over 2x more than the current price!

Build Your Own Pinterest Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Pinterest research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Pinterest research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Pinterest's overall financial health at a glance.

Contemplating Other Strategies?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 35 companies in the world exploring or producing it. Find the list for free.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PINS

Operates as a visual search and discovery platform in the United States, Canada, Europe, and internationally.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|2.3% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|42.0% undervalued

TR

Community Contributor