- United States

- /

- Interactive Media and Services

- /

- NYSE:PINS

Pinterest (NYSE:PINS) Sees 7% Rise Over Last Quarter With Taste Of Home Partnership

Reviewed by Simply Wall St

Pinterest (NYSE:PINS) gained attention with its partnership with Taste of Home, launching a unique video series that potentially contributed to its 7% price increase over the past quarter. This collaboration highlights a blend of culinary storytelling and digital engagement, aiming to enhance Pinterest’s content strategy. The company's strong growth in earnings and share buybacks further painted a positive picture for investors. Meanwhile, broader market conditions showed mixed results, with volatile trading and tariff concerns impacting sentiment. Despite the market's recent fluctuations, Pinterest's strategic initiatives and favorable earnings results stood out in the tech space.

Over the last five-year period, Pinterest achieved a total shareholder return of 105.84%, reflecting a significant performance milestone. This impressive return is partly attributed to Pinterest's focused investments in AI, enhancing user experience and advertising effectiveness, and a series of lucrative international partnerships with major players like Amazon Ads and Google. Additionally, monetization strategies, such as optimizing lower-funnel advertising tools and increasing shoppability, contributed to higher global revenue streams and bolstered earnings capacity.

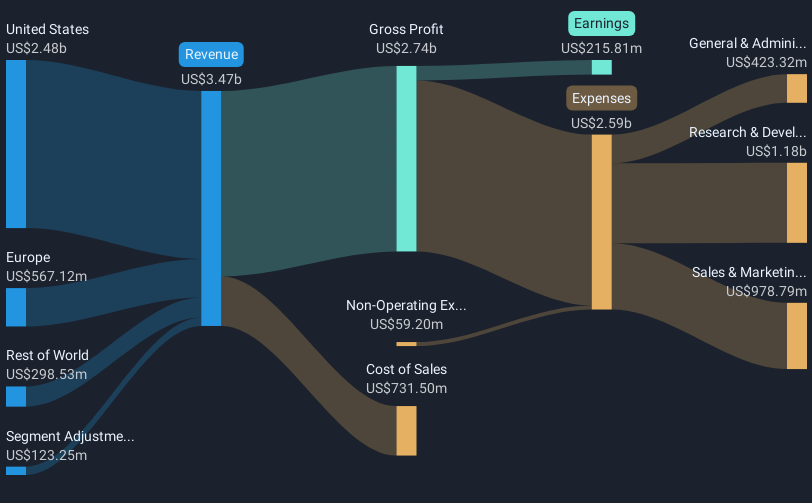

As market conditions fluctuated, Pinterest's aggressive share buyback programs provided a further boost, reducing the number of shares outstanding and enhancing shareholder value. The company's robust earnings growth in 2024, with net income soaring to US$1.86 billion, highlights improved financial health compared to previous years. Despite broader market volatility, these efforts underscore Pinterest's resilience, though it lagged the US Interactive Media and Services industry and broader market over the past year. Performance was affected by shifts in auction mix, which could pressure pricing, adding complexity to its valuation story.

Explore Pinterest's analyst forecasts in our growth report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Pinterest, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PINS

Operates as a visual search and discovery platform in the United States, Canada, Europe, and internationally.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Community Narratives