- United States

- /

- Interactive Media and Services

- /

- NYSE:PINS

Pinterest (NYSE:PINS) Reports Robust Q4 Earnings While Stock Dips 0.25%

Reviewed by Simply Wall St

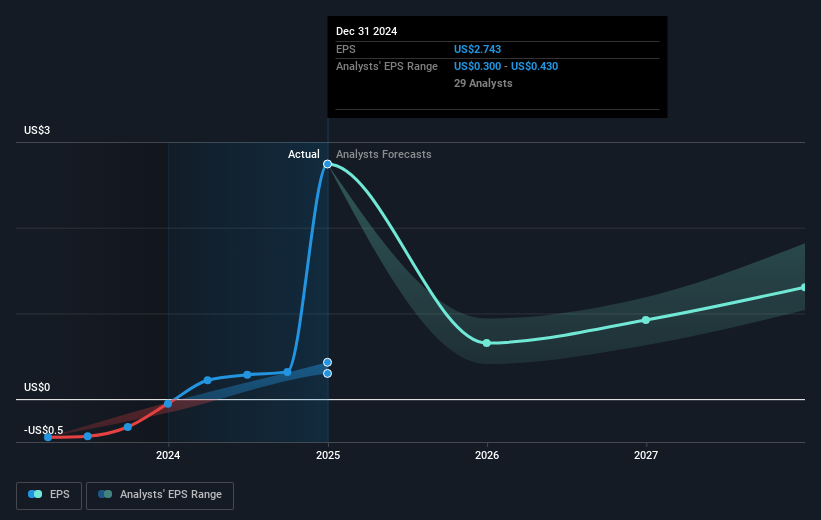

Pinterest (NYSE:PINS) recently launched a strategic partnership with Taste of Home to feature the "50 Plates Across the States" video series, expanding its content landscape. Despite this initiative marking a promising collaboration, Pinterest's stock price saw a 0.25% decline over the last quarter. This performance unfolded against a backdrop of broader market volatility, with the Nasdaq and other indexes slipping due to geopolitical uncertainties like new tariffs. Pinterest's Q4 2024 earnings report was robust, showing increased revenue and net income year-over-year, which could be seen as a mitigating factor in such a challenging market context. Contributing to shareholder returns, the company repurchased over three million shares, thus slightly enhancing shareholder value during a turbulent market environment. However, external market pressures maintained a dampening effect on Pinterest's share price stability, aligning with the prevailing market trends marked by a 4.6% recent market descent.

Click here and access our complete analysis report to understand the dynamics of Pinterest.

In the last five years, Pinterest's total shareholder return, including share price appreciation and dividends, surged impressively by 172.77%. This remarkable performance was driven by several key developments. Pinterest achieved significant growth in its earnings, with net income jumping from a net loss to US$1.86 billion in 2024. Strategic partnerships were instrumental, such as the collaboration with VTEX in 2024, enhancing its social commerce platform and amplifying consumer brand engagement. Furthermore, the company executed substantial share buybacks totaling US$500.05 million in late 2023, which contributed to shareholder value during times of market turbulence.

Despite the progress, Pinterest underperformed both the US Interactive Media and Services industry and the broader US market over the past year. However, its robust return on equity of 39.2% and business model adjustments, including corporate guidance for significant revenue growth in early 2025, reflect Pinterest's efforts to adapt to industry challenges and capitalize on new opportunities.

- Unlock the insights behind Pinterest's valuation and discover its true investment potential

- Analyze the downside risks for Pinterest and understand their potential impact—click to learn more.

- Shareholder in Pinterest? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PINS

Operates as a visual search and discovery platform in the United States, Canada, Europe, and internationally.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Community Narratives