- United States

- /

- Interactive Media and Services

- /

- NYSE:KIND

What Nextdoor Holdings, Inc.'s (NYSE:KIND) 27% Share Price Gain Is Not Telling You

Nextdoor Holdings, Inc. (NYSE:KIND) shares have continued their recent momentum with a 27% gain in the last month alone. Looking further back, the 14% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

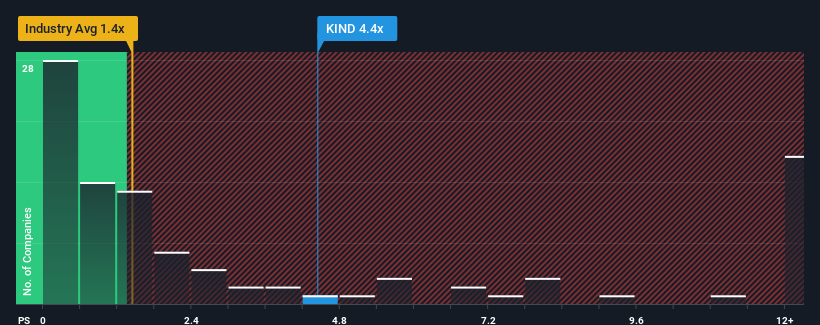

Since its price has surged higher, given around half the companies in the United States' Interactive Media and Services industry have price-to-sales ratios (or "P/S") below 1.4x, you may consider Nextdoor Holdings as a stock to avoid entirely with its 4.4x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

See our latest analysis for Nextdoor Holdings

How Nextdoor Holdings Has Been Performing

Nextdoor Holdings could be doing better as it's been growing revenue less than most other companies lately. One possibility is that the P/S ratio is high because investors think this lacklustre revenue performance will improve markedly. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think Nextdoor Holdings' future stacks up against the industry? In that case, our free report is a great place to start.How Is Nextdoor Holdings' Revenue Growth Trending?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Nextdoor Holdings' to be considered reasonable.

Taking a look back first, we see that the company managed to grow revenues by a handy 4.8% last year. Pleasingly, revenue has also lifted 66% in aggregate from three years ago, partly thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Looking ahead now, revenue is anticipated to climb by 11% each year during the coming three years according to the six analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 12% per annum, which is not materially different.

In light of this, it's curious that Nextdoor Holdings' P/S sits above the majority of other companies. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. Although, additional gains will be difficult to achieve as this level of revenue growth is likely to weigh down the share price eventually.

What We Can Learn From Nextdoor Holdings' P/S?

Shares in Nextdoor Holdings have seen a strong upwards swing lately, which has really helped boost its P/S figure. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Given Nextdoor Holdings' future revenue forecasts are in line with the wider industry, the fact that it trades at an elevated P/S is somewhat surprising. The fact that the revenue figures aren't setting the world alight has us doubtful that the company's elevated P/S can be sustainable for the long term. Unless the company can jump ahead of the rest of the industry in the short-term, it'll be a challenge to maintain the share price at current levels.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for Nextdoor Holdings that you should be aware of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Nextdoor Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:KIND

Nextdoor Holdings

Operates a neighborhood network that connects neighbors, businesses, and public services in the United States and internationally.

Excellent balance sheet and slightly overvalued.