- United States

- /

- Media

- /

- NYSE:GTN

Gray Television, Inc. (NYSE:GTN) Looks Inexpensive After Falling 25% But Perhaps Not Attractive Enough

Gray Television, Inc. (NYSE:GTN) shareholders won't be pleased to see that the share price has had a very rough month, dropping 25% and undoing the prior period's positive performance. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 45% share price drop.

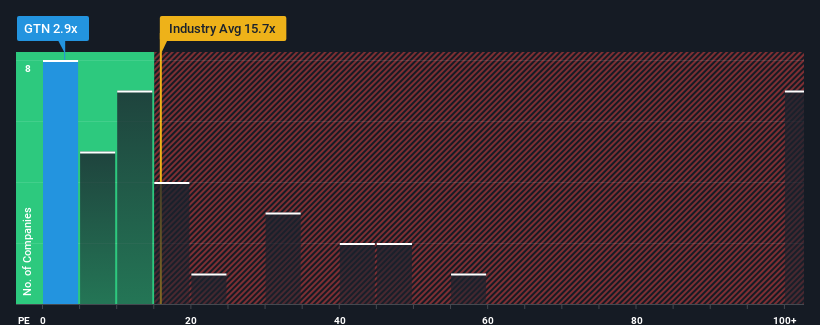

Following the heavy fall in price, Gray Television's price-to-earnings (or "P/E") ratio of 2.9x might make it look like a strong buy right now compared to the market in the United States, where around half of the companies have P/E ratios above 20x and even P/E's above 36x are quite common. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

With earnings growth that's superior to most other companies of late, Gray Television has been doing relatively well. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Check out our latest analysis for Gray Television

Does Growth Match The Low P/E?

There's an inherent assumption that a company should far underperform the market for P/E ratios like Gray Television's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 110% gain to the company's bottom line. However, this wasn't enough as the latest three year period has seen a very unpleasant 39% drop in EPS in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Turning to the outlook, the next three years should bring diminished returns, with earnings decreasing 34% per annum as estimated by the seven analysts watching the company. Meanwhile, the broader market is forecast to expand by 11% each year, which paints a poor picture.

In light of this, it's understandable that Gray Television's P/E would sit below the majority of other companies. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

The Bottom Line On Gray Television's P/E

Gray Television's P/E looks about as weak as its stock price lately. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Gray Television maintains its low P/E on the weakness of its forecast for sliding earnings, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

You need to take note of risks, for example - Gray Television has 3 warning signs (and 2 which are significant) we think you should know about.

If these risks are making you reconsider your opinion on Gray Television, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:GTN

Gray Media

A multimedia company, owns and/or operates television stations and digital assets in the United States.

Undervalued with proven track record and pays a dividend.

Similar Companies

Market Insights

Community Narratives