If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Speaking of which, we noticed some great changes in Altice USA's (NYSE:ATUS) returns on capital, so let's have a look.

Return On Capital Employed (ROCE): What Is It?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on Altice USA is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.063 = US$1.9b ÷ (US$32b - US$2.2b) (Based on the trailing twelve months to March 2023).

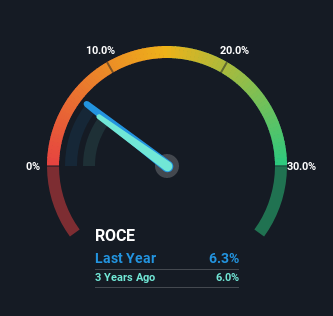

So, Altice USA has an ROCE of 6.3%. In absolute terms, that's a low return and it also under-performs the Media industry average of 9.5%.

Check out our latest analysis for Altice USA

Above you can see how the current ROCE for Altice USA compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

SWOT Analysis for Altice USA

- No major strengths identified for ATUS.

- Earnings declined over the past year.

- Interest payments on debt are not well covered.

- Annual earnings are forecast to grow faster than the American market.

- Trading below our estimate of fair value by more than 20%.

- Debt is not well covered by operating cash flow.

- Total liabilities exceed total assets, which raises the risk of financial distress.

- Annual revenue is expected to decline over the next 3 years.

How Are Returns Trending?

Altice USA has not disappointed with their ROCE growth. More specifically, while the company has kept capital employed relatively flat over the last five years, the ROCE has climbed 110% in that same time. So our take on this is that the business has increased efficiencies to generate these higher returns, all the while not needing to make any additional investments. The company is doing well in that sense, and it's worth investigating what the management team has planned for long term growth prospects.

In Conclusion...

To sum it up, Altice USA is collecting higher returns from the same amount of capital, and that's impressive. However the stock is down a substantial 85% in the last five years so there could be other areas of the business hurting its prospects. In any case, we believe the economic trends of this company are positive and looking into the stock further could prove rewarding.

If you'd like to know more about Altice USA, we've spotted 5 warning signs, and 2 of them make us uncomfortable.

While Altice USA may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:ATUS

Altice USA

Provides broadband communications and video services in the United States, Canada, Puerto Rico, and the Virgin Islands.

Undervalued low.

Similar Companies

Market Insights

Community Narratives