- United States

- /

- Interactive Media and Services

- /

- NasdaqGS:TBLA

Taboola (TBLA) Turns Profitable, Defies Skeptics with Rapid Earnings Growth and High Valuation

Reviewed by Simply Wall St

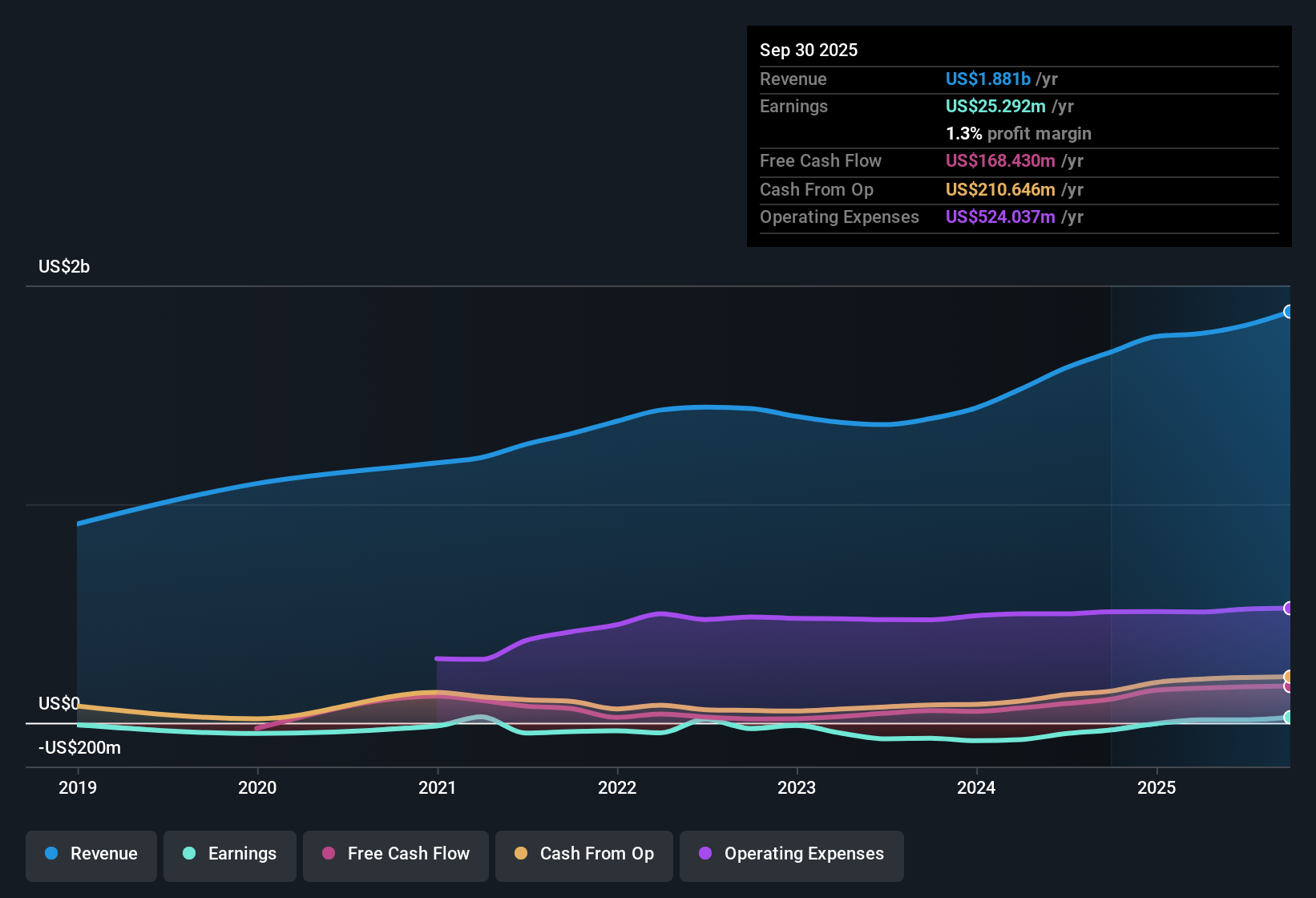

Taboola (TBLA) has turned profitable for the first time, with its net profit margin showing clear improvement over the past year. The company’s earnings are forecast to grow at an impressive 32.4% per year, more than double the US market’s average, while revenue is expected to grow at 6.9% annually, trailing the broader market’s 10.5%. Shares recently traded at $3.71, which is well below an estimated fair value of $10.05. The current Price-To-Earnings Ratio stands at a hefty 80.9x, indicating a premium compared to industry peers.

See our full analysis for Taboola.com.With the latest earnings on the table, it's time to see how these results stack up against the market's prevailing narratives and whether the consensus view holds up to fresh data.

See what the community is saying about Taboola.com

Profit Margins Edging Up from 0.7% to 1.7%

- Taboola's profit margin is expected to climb from 0.7% today to 1.7% within three years, highlighting a push toward leaner operations and higher efficiency.

- Analysts' consensus view anticipates stronger future profits, with improved margins driven by:

- AI-powered targeting and new advertising platforms, such as Realize, that could boost high-margin revenue streams.

- Broader customer reach via global partnerships and better first-party data, both of which support sustained margin gains as privacy changes favor Taboola's approach.

- Consensus narrative sees margin growth improving the profit outlook, but success depends on scaling Realize and publisher partnerships while maintaining margin discipline. 📊 Read the full Taboola.com Consensus Narrative.

Share Buybacks to Lift Earnings Per Share

- Taboola has bought back 12% of its shares in the first half of 2025 and has approval to continue, with analysts expecting share count to fall by 7% per year over the next three years.

- Consensus narrative suggests buybacks will materially boost earnings per share, reinforcing management's confidence in long-term value even if core revenue growth (excluding Realize platform) remains subdued at 3 to 5%.

- Share repurchases lower outstanding share count, amplifying the impact of any future earnings growth on EPS.

- These actions are welcomed by bullish investors as a meaningful return of capital and vote of confidence by management during a new phase of growth.

High Valuation Premium vs. Peers

- Taboola trades at an 80.9x Price-To-Earnings Ratio, dwarfing both the US Interactive Media and Services sector average (16.1x) and the peer group (11.6x), revealing significant multiple expansion.

- Analysts' consensus view flags this lofty valuation as a double-edged sword, as rapid profit growth and new platform adoption must continue at a fast pace to justify paying over 7 times the sector average:

- Current share price of $3.71 remains a discount to its DCF fair value of $10.05, but also stands 15% below the consensus price target of $4.38, indicating some upside if growth trends deliver as expected.

- However, sticky risks linger. Revenue outside of Realize is growing far slower than historical double digits, putting extra pressure on early-stage platform ramp-up to validate premium multiples.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Taboola.com on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Have a different take on the figures? Share your outlook and contribute your perspective in just a few minutes by Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Taboola.com.

See What Else Is Out There

Despite impressive headline growth, Taboola’s core revenue is slowing and its lofty valuation depends on new platforms gaining traction quickly enough to justify investor optimism.

If you want to focus on stocks that are attractively priced without relying on ambitious growth targets, check out these 836 undervalued stocks based on cash flows for companies trading well below their fair value today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Taboola.com might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TBLA

Taboola.com

Operates an artificial intelligence-based algorithmic engine platform in Israel, the United States, the United Kingdom, Germany, and internationally.

Excellent balance sheet with acceptable track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion

<html><head></head><body><div dir="auto">This is true here, but always true in the case of Alpha leaders. Often is takes a turn or two to get it right, like Gates to Nardella,  or Anton to Pinchar. This is when succession planning has failed or never happened. </div><div><br></div> </body></html>