Advertisement

- United States

- /

- Interactive Media and Services

- /

- NasdaqGM:RUM

Analysts Have Been Trimming Their Rumble Inc. (NASDAQ:RUM) Price Target After Its Latest Report

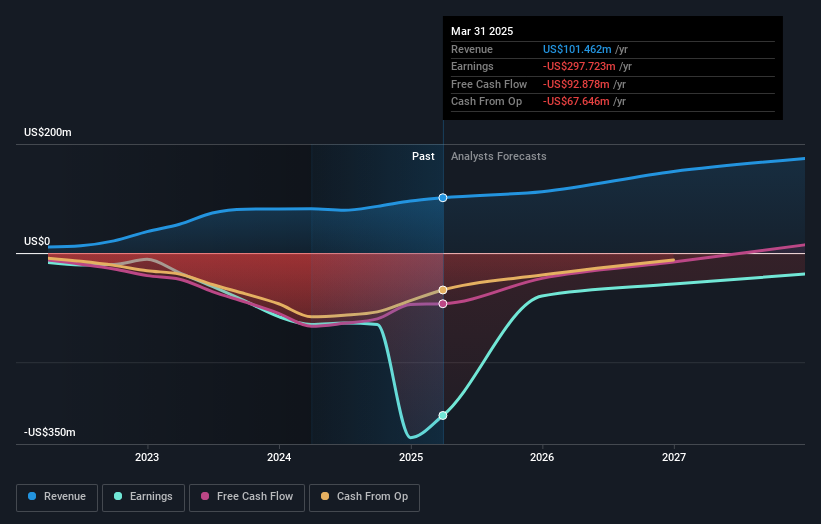

Rumble Inc. (NASDAQ:RUM) defied analyst predictions to release its quarterly results, which were ahead of market expectations. Results overall were solid, with revenues arriving 4.1% better than analyst forecasts at US$24m. Higher revenues also resulted in substantially lower statutory losses which, at US$0.01 per share, were 4.1% smaller than the analysts expected. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

We've discovered 3 warning signs about Rumble. View them for free.

Taking into account the latest results, the most recent consensus for Rumble from three analysts is for revenues of US$112.6m in 2025. If met, it would imply a notable 11% increase on its revenue over the past 12 months. Losses are predicted to fall substantially, shrinking 64% to US$0.32. Before this latest report, the consensus had been expecting revenues of US$109.6m and US$0.31 per share in losses. Overall it looks as though the analysts were a bit mixed on the latest consensus updates. Although there was a nice uplift to revenue, the consensus also made a modest increase to its losses per share forecasts.

View our latest analysis for Rumble

It will come as no surprise that expanding losses caused the consensus price target to fall 6.7% to US$14.00with the analysts implicitly ranking ongoing losses as a greater concern than growing revenues. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on Rumble, with the most bullish analyst valuing it at US$20.00 and the most bearish at US$8.00 per share. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would highlight that Rumble's revenue growth is expected to slow, with the forecast 15% annualised growth rate until the end of 2025 being well below the historical 48% p.a. growth over the last three years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 10% per year. So it's pretty clear that, while Rumble's revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The most important thing to take away is that the analysts increased their loss per share estimates for next year. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Rumble's future valuation.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Rumble analysts - going out to 2027, and you can see them free on our platform here.

Plus, you should also learn about the 3 warning signs we've spotted with Rumble .

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:RUM

Rumble

Operates video sharing platforms and cloud services in the United States, Canada, and internationally.

Excellent balance sheet low.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor