Advertisement

- United States

- /

- Media

- /

- NasdaqGS:FOXA

Fox FOXA Margin Compression Challenges Long Term Bullish Earnings Narrative After Q2 2026 Results

How Fox (FOXA) Has Been Performing Heading Into Q2 2026

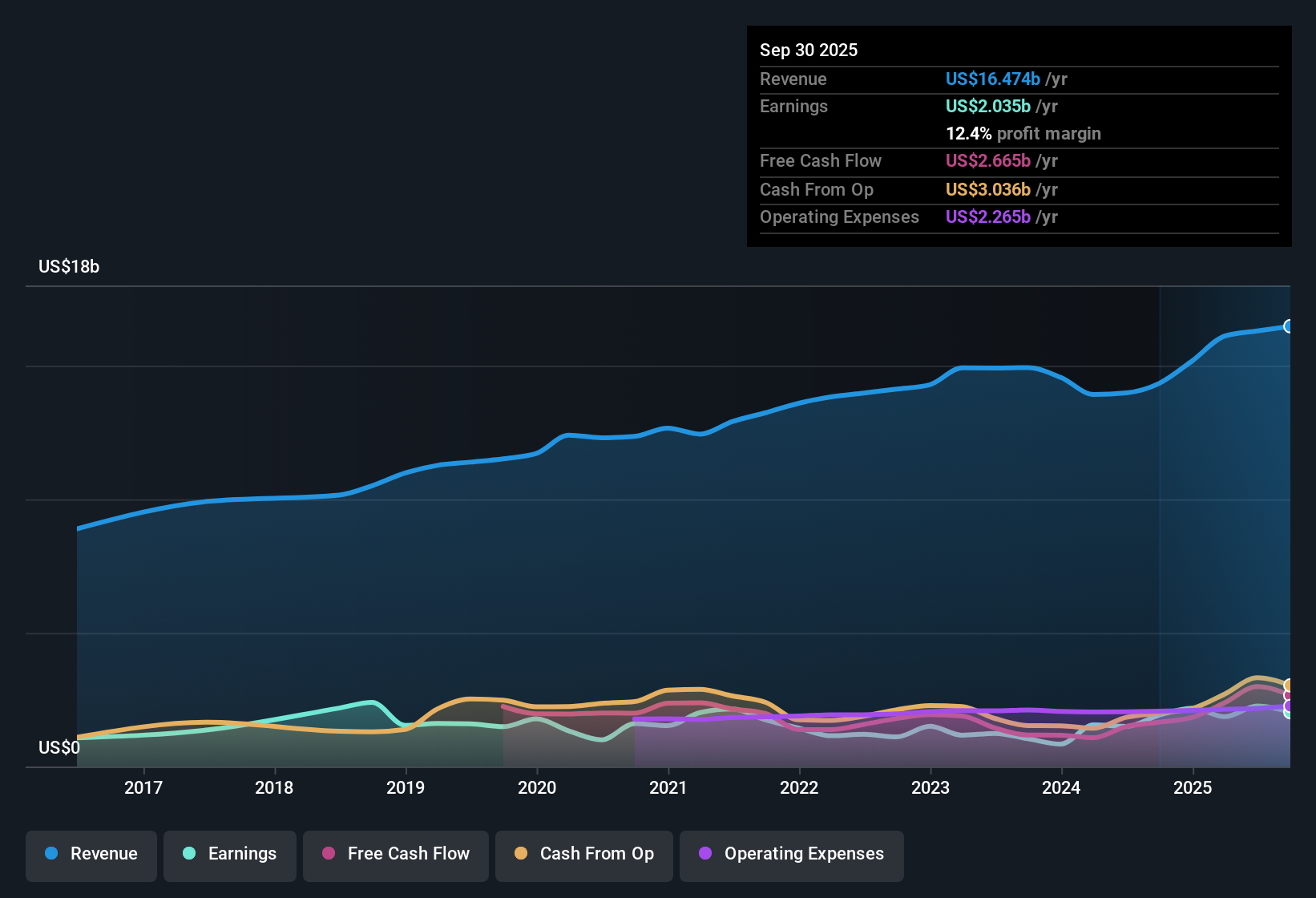

Fox (FOXA) just posted Q2 2026 revenue of US$5.2b with basic EPS of US$0.53, putting fresh numbers on the board for investors watching its media earnings story. The company has seen quarterly revenue move from US$5.1b in Q2 2025 to US$5.2b this quarter, while EPS shifted from US$0.82 to US$0.53 over the same period. On a trailing twelve month basis, EPS sits at US$4.24 on revenue of US$16.6b. With net profit margin over the last year at 11.4% compared to 14.4% previously, the latest results keep the focus squarely on how efficiently Fox is turning its top line into profit.

See our full analysis for Fox.With the latest quarter in hand, the next step is to set these numbers against the most common stories about Fox to see which narratives match the data and which ones the results start to challenge.

Curious how numbers become stories that shape markets? Explore Community Narratives

TTM EPS Slips From US$4.97 To US$4.24

- On a trailing twelve month basis, basic EPS is US$4.24, compared with US$4.97 at Q4 2025 and US$4.51 at Q1 2026, even though trailing revenue has moved from US$16.3b to US$16.6b across those same snapshots.

- What stands out for a bullish view that focuses on multi year earnings growth around 4.9% and forecast growth of about 5.3% per year is that the latest trailing EPS of US$4.24 and trailing net income of US$1.9b sit below the earlier US$2.3b level, which means:

- Supporters can still point to positive five year growth and mid single digit forecasts, but the recent EPS drift and lower trailing profit show that the growth path has not been perfectly smooth.

- At the same time, the company is still earning well over US$1b in profit on about US$16.6b of revenue, so the bullish story about an established earnings base with room for further compounding is grounded in real cash generating capacity rather than just theory.

Investors who want to see how this earnings trend fits into a broader long term story can step back and read the full narrative around growth, risks, and valuation in one place with 📊 Read the full Fox Consensus Narrative.

Margins Ease To 11.4% On Lower Trailing Profit

- Net profit margin over the last year is 11.4% compared to 14.4% previously, with trailing net income at US$1.9b on US$16.6b of revenue versus the earlier US$2.3b on US$16.3b, so profitability on each dollar of sales has been thinner than before.

- Critics highlight margin pressure as a key bearish angle, and the data backs that concern because:

- The move from a 14.4% margin to 11.4% translates to several hundred million dollars less profit on a revenue base that is a little higher, so the margin effect matters more than the top line change.

- With earnings growth over the past year described as negative and trailing EPS dropping from US$4.97 to US$4.24, bears can reasonably argue that recent profitability trends do not yet match the longer term growth story.

P/E Of 14.8x And DCF Gap Send Mixed Valuation Signal

- At a share price of US$65.92, Fox trades on a trailing P/E of 14.8x, above the 11x peer average and in line with the US media industry, while also sitting about 13% below a DCF fair value of roughly US$75.75.

- What is interesting for a bearish narrative that focuses on valuation and balance sheet risk is how the numbers pull in different directions:

- On the cautionary side, a 14.8x P/E that is higher than peers and a high level of debt suggest investors are paying more than similar companies while also accepting higher financial leverage.

- Set against that, the indicated 13% gap between the current share price and the DCF fair value means valuation models still see room between price and estimated worth, which softens the case that the stock is outright expensive based only on the P/E comparison.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Fox's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Fox is still generating solid revenue, but softer margins, lower trailing EPS and a relatively high P/E all point to pressure on value and profitability.

If those pressures make you want a stronger margin of safety, check out our 55 high quality undervalued stocks to quickly zero in on companies where the price tag looks more forgiving.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:FOXA

Fox

Operates as a news, sports, and entertainment company in the United States.

Undervalued with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0774.4% undervalued

220 followersusers have followed this narrative

1 commentusers have commented on this narrative

33 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22089.4% undervalued

55 followersusers have followed this narrative

2 commentsusers have commented on this narrative

21 likesusers have liked this narrative

YI

yiannisz on Hesai Group ·

The First Real Lidar Winner

Fair Value:US$27.0716.3% undervalued

14 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

TR

tripledub on Taiwan Semiconductor Manufacturing ·

The Most Wonderful Monopoly in the Most Dangerous Neighbourhood on Earth

Fair Value:US$3812.7% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

Recently Updated Narratives

AV

avt on TROPHY GAMES Development ·

TROPHY GAMES Development Will See Revenue Rise by 22% in the Next 3 Years

Fair Value:DKK 19.0727.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TH

Thomas_Regrettier on ASML Holding ·

ASML at €725: Geopolitical Risk Priced In, Moat Still Intact

Fair Value:€92038.0% overvalued

11 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

CG

CG86 on Bausch + Lomb ·

$BLCO & $COO The Silence BEFORE the AGM: A Retail Investor’s Timeline, Findings, and Opinion on SUSPICIOUS SILENCE!

Fair Value:US$39.2358.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3956.1% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

42 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

37 followersusers have followed this narrative

11 commentsusers have commented on this narrative

32 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$587.3136.9% undervalued

1352 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

EL

Element1 on Greatland Resources ·

I can’t believe how inaccurate and out of date this site is—and people rely on it. Greatland owns tw...

0

|0

MI

Mikeymike on Auxly Cannabis Group ·

Id like to understand why they believe the profit margin is going decline so dramatically. Is it ene...

0

|0