Advertisement

- United States

- /

- Interactive Media and Services

- /

- NasdaqGS:META

Facebook's (NASDAQ:FB) US and EU Growth has Peaked and Advertising Revenue is under Pressure from Competitors

As you might know, Facebook, Inc. ( NASDAQ:FB ) just posted their latest second-quarter results with some very strong numbers. When looking at the company, three things come to mind. The "sell high" part from the cliché phrase "buy low, sell high", diminishing future growth rates, and very high margins.

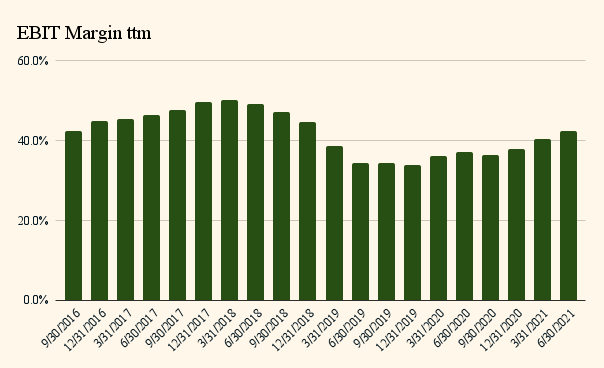

Let's open up with margins, because when you look at them, they are quite hard to wrap one's head around:

From the chart above, we can see that Facebook has been regaining profitability in the last two years, this seems to be due to daily active user growth on a global scale, an increase of average dollars per user and the general expansion in Asia Pacific and the rest of the world.

You will also notice, that below I start making some quite pessimistic points, I would however, like to comment that Facebook has impeccable free cash flows, and on-point cash outflows regarding investing and financing. They prioritize R&D spending, which is exactly what investors would like to see in a tech company : Heavy capital and research & development investments. On a qualitative note, their advertisement platform has improved in functionality and efficacy quite a bit from a year ago, and their global reach has stayed in a leading position with the contributions from Instagram and WhatsApp.

Now let's see how Facebook has been growing thus far and what challenges lie ahead.

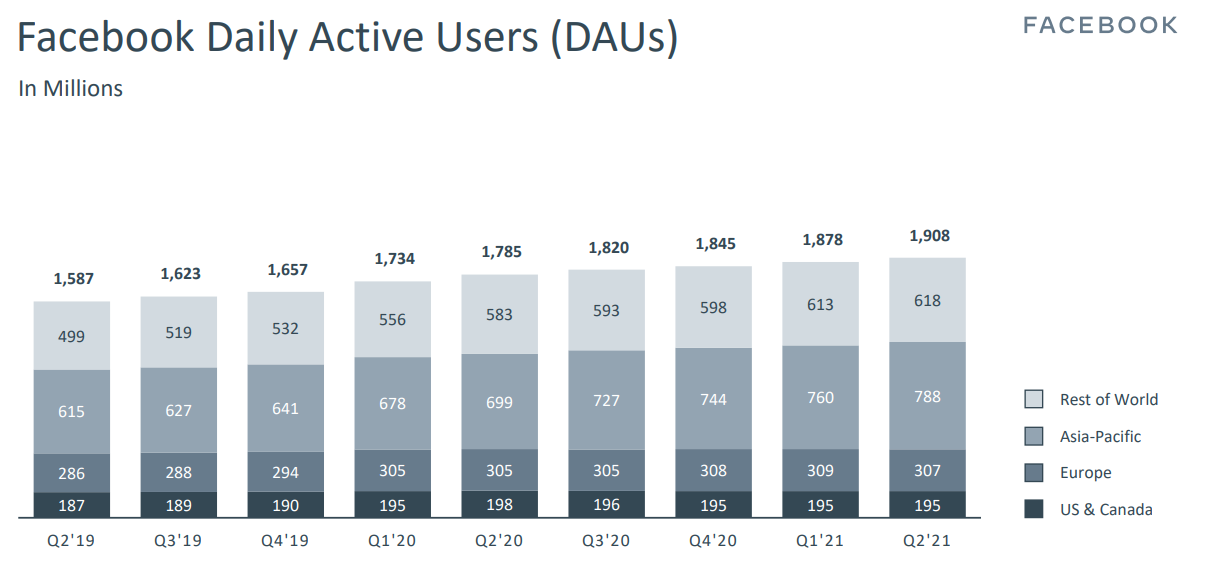

The chart above is interesting as it already showcases the stagnation of US and European daily user growth. You can find these results in their Q2 quarterly report. Facebook's CFO comments that there might be a bump in the future:

"In the third and fourth quarters of 2021, we expect year-over-year total revenue growth rates to decelerate significantly on a sequential basis... (We) expect increased ad targeting headwinds in 2021 from regulatory and platform changes, notably the recent iOS updates, which we expect to have a greater impact in the third quarter..."

What we can incorporate from this, is that US and EU revenues will be under pressure, as iOS users will be given a choice to turn tracking on and off, which is estimated to diminish the returns from advertising. It won't be directly impacted per se, it's the ad targeting algorithm that is under threat, and Facebook will have to find a different heuristic or alternative approach to increase advertising revenue per user. US and EU users are particularly important, because they bring in US$51.5 and US$17.2 respectively per user, versus the world average of US$9.95.

This is partly the reason why the stock may be approaching a peak - Yes, there is still upside, but investors are now involved with a timing issue as the primary question starts being "When?", rather than "If?".

Now, we will take a step back and put history in context with analysts forecasts for the future.

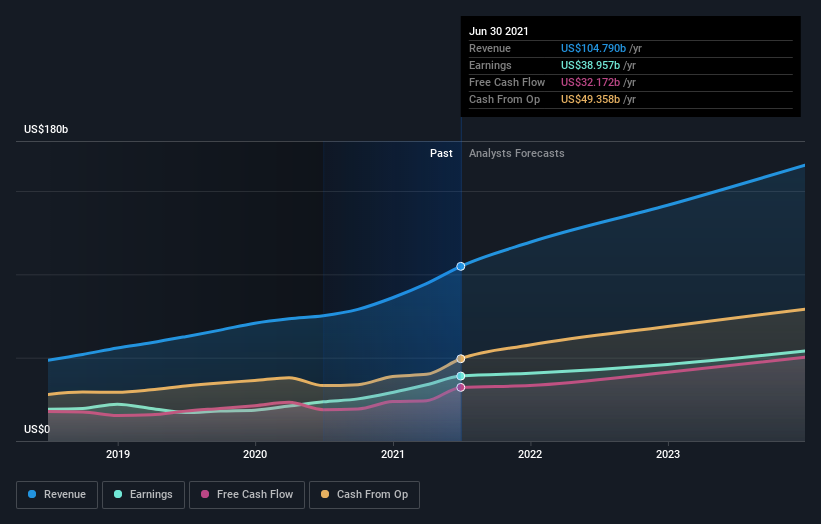

Q2 earnings represented an overall positive result, with revenues beating expectations by 4.2% to hit US$29b. Facebook also reported a statutory profit of US$3.61, which was an impressive 20% above what the analysts had forecasted.

View our latest analysis for Facebook

Following the latest results, Facebook's 45 analysts are now forecasting revenues of US$119.2b in 2021. This would be a meaningful 14% improvement in sales compared to the last 12 months. Statutory earnings per share are predicted to increase 2.9% to US$14.09.

The analysts reconfirmed their price target of US$414.

Conclusion

Facebook is and continues to be a high margin, cash delivery company. However, the financial market is a forward-looking weighing machine, and the future suggests a possible change in direction.

The company is stable and competently managed. Future challenges imply a revision of advertising practices, discovering new heuristics or improving on the existing algorithm, delivering further growth from the developing world and maintaining user engagement without sacrificing on margins.

For investors that had a very good run thus far, it is hard to ask for pause, but the past does not dictate, and I post two "common sense" questions:

- Will the future bring more people to Apple's iOS? (look at the performance of the new iPhone)

- When talking to people, are they bragging or trying to hide their time spent on any of Facebook's platforms?

The consensus price target held steady at US$414, with the latest estimates not enough to have an impact on their price targets.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have forecasts for Facebook going out to 2023, and you can see them free on our platform here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NasdaqGS:META

Meta Platforms

Engages in the development of products that enable people to connect and share with friends and family through mobile devices, personal computers, virtual reality and mixed reality headsets, augmented reality, and wearables worldwide.

Outstanding track record and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets