Advertisement

- United States

- /

- Packaging

- /

- NYSE:SW

Dividend Investors: Don't Be Too Quick To Buy Smurfit Westrock Plc (NYSE:SW) For Its Upcoming Dividend

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Smurfit Westrock Plc (NYSE:SW) is about to go ex-dividend in just four days. The ex-dividend date is one business day before a company's record date, which is the date on which the company determines which shareholders are entitled to receive a dividend. It is important to be aware of the ex-dividend date because any trade on the stock needs to have been settled on or before the record date. Accordingly, Smurfit Westrock investors that purchase the stock on or after the 14th of February will not receive the dividend, which will be paid on the 18th of March.

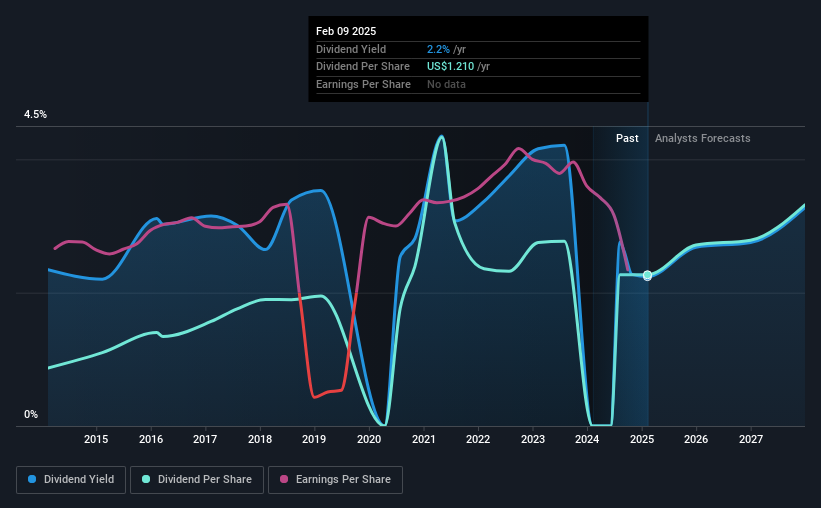

The company's next dividend payment will be US$0.4308 per share, on the back of last year when the company paid a total of US$1.21 to shareholders. Last year's total dividend payments show that Smurfit Westrock has a trailing yield of 2.2% on the current share price of US$54.00. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. As a result, readers should always check whether Smurfit Westrock has been able to grow its dividends, or if the dividend might be cut.

Check out our latest analysis for Smurfit Westrock

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Last year, Smurfit Westrock paid out 288% of its profit to shareholders in the form of dividends. This is not sustainable behaviour and requires a closer look on behalf of the purchaser. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. Over the last year, it paid out dividends equivalent to 395% of what it generated in free cash flow, a disturbingly high percentage. It's pretty hard to pay out more than you earn, so we wonder how Smurfit Westrock intends to continue funding this dividend, or if it could be forced to cut the payment.

Cash is slightly more important than profit from a dividend perspective, but given Smurfit Westrock's payouts were not well covered by either earnings or cash flow, we would be concerned about the sustainability of this dividend.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. With that in mind, we're encouraged by the steady growth at Smurfit Westrock, with earnings per share up 9.2% on average over the last five years. Earnings per share have been growing comfortably, although unfortunately the company is paying out more of its profits than we're comfortable with over the long term.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Smurfit Westrock has delivered 10% dividend growth per year on average over the past 10 years. We're glad to see dividends rising alongside earnings over a number of years, which may be a sign the company intends to share the growth with shareholders.

The Bottom Line

Is Smurfit Westrock an attractive dividend stock, or better left on the shelf? The dividends are not well covered by either income or free cash flow, although at least earnings per share are slowly increasing. With the way things are shaping up from a dividend perspective, we'd be inclined to steer clear of Smurfit Westrock.

With that in mind though, if the poor dividend characteristics of Smurfit Westrock don't faze you, it's worth being mindful of the risks involved with this business. Be aware that Smurfit Westrock is showing 6 warning signs in our investment analysis, and 3 of those don't sit too well with us...

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:SW

Smurfit Westrock

Manufactures, distributes, and sells containerboard, corrugated containers, and other paper-based packaging products.

Moderate and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.3% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor