Advertisement

- United States

- /

- Packaging

- /

- NYSE:MYE

We Ran A Stock Scan For Earnings Growth And Myers Industries (NYSE:MYE) Passed With Ease

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Myers Industries (NYSE:MYE). While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

Our analysis indicates that MYE is potentially undervalued!

How Quickly Is Myers Industries Increasing Earnings Per Share?

The market is a voting machine in the short term, but a weighing machine in the long term, so you'd expect share price to follow earnings per share (EPS) outcomes eventually. So it makes sense that experienced investors pay close attention to company EPS when undertaking investment research. Impressively, Myers Industries has grown EPS by 29% per year, compound, in the last three years. As a general rule, we'd say that if a company can keep up that sort of growth, shareholders will be beaming.

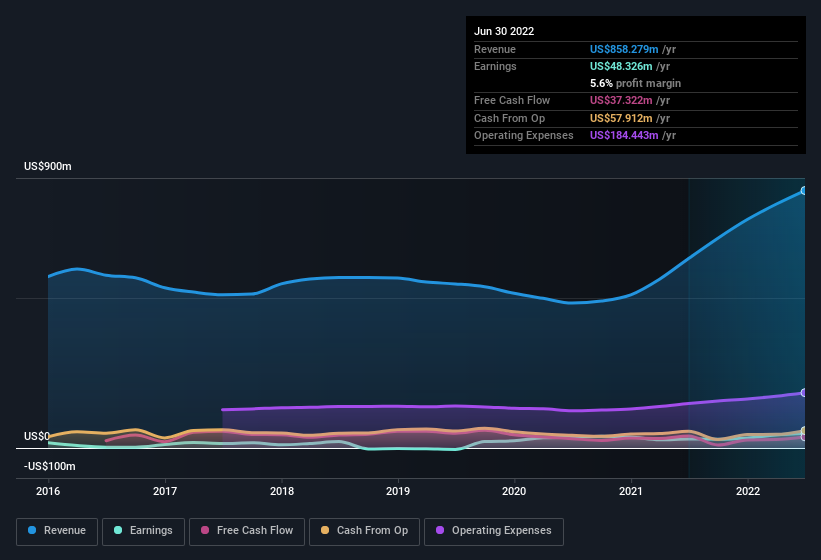

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. Myers Industries maintained stable EBIT margins over the last year, all while growing revenue 36% to US$858m. That's progress.

You can take a look at the company's revenue and earnings growth trend, in the chart below. For finer detail, click on the image.

While we live in the present moment, there's little doubt that the future matters most in the investment decision process. So why not check this interactive chart depicting future EPS estimates, for Myers Industries?

Are Myers Industries Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

It's good to see Myers Industries insiders walking the walk, by spending US$549k on shares in just twelve months. And when you consider that there was no insider selling, you can understand why shareholders might believe that there are brighter days ahead. We also note that it was the Independent Director, Ronald De Feo, who made the biggest single acquisition, paying US$185k for shares at about US$18.49 each.

It's reassuring that Myers Industries insiders are buying the stock, but that's not the only reason to think management are fair to shareholders. To be specific, the CEO is paid modestly when compared to company peers of the same size. The median total compensation for CEOs of companies similar in size to Myers Industries, with market caps between US$400m and US$1.6b, is around US$4.0m.

The Myers Industries CEO received US$2.7m in compensation for the year ending December 2021. That comes in below the average for similar sized companies and seems pretty reasonable. While the level of CEO compensation shouldn't be the biggest factor in how the company is viewed, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. It can also be a sign of good governance, more generally.

Is Myers Industries Worth Keeping An Eye On?

For growth investors, Myers Industries' raw rate of earnings growth is a beacon in the night. And that's not the only positive either. We have both insider buying and reasonable and remuneration to consider. The overriding message from this quick rundown is yes, this stock is worth investigating further. Of course, just because Myers Industries is growing does not mean it is undervalued. If you're wondering about the valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Myers Industries, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:MYE

Myers Industries

Engages in distribution of tire service supplies in Ohio.

Average dividend payer slight.

Market Insights

Advertisement

Community Narratives

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value US$31.72|41.9% undervalued

KI

Community Contributor

EasyJet weirdly unloved by investors in spite of relatively attractive metrics

Fair Value UK£6.95|31.9% undervalued

PI

Community Contributor

HEXPOL AB: Sustained Long Term Growth, Stable Margins, and Strategic M&A

Fair Value SEK 122.27|24.9% undervalued

MA

Community Contributor