Advertisement

- United States

- /

- Packaging

- /

- NYSE:MYE

Semler Scientific And 2 Other Undervalued Small Caps With Insider Action In US

Simply Wall St

Reviewed by Simply Wall St

In the last week, the United States market has stayed flat, yet it is up 24% over the past year with earnings forecasted to grow by 15% annually. In this context, identifying small-cap stocks with insider action can be an intriguing strategy for investors seeking potentially undervalued opportunities amidst stable market conditions.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| ProPetro Holding | NA | 0.7x | 22.27% | ★★★★★☆ |

| OptimizeRx | NA | 1.1x | 43.45% | ★★★★★☆ |

| Quanex Building Products | 32.1x | 0.8x | 40.10% | ★★★★☆☆ |

| First United | 12.9x | 2.9x | 47.11% | ★★★★☆☆ |

| McEwen Mining | 4.1x | 2.1x | 46.58% | ★★★★☆☆ |

| Innovex International | 8.8x | 2.0x | 49.92% | ★★★★☆☆ |

| German American Bancorp | 14.8x | 4.9x | 48.28% | ★★★☆☆☆ |

| Franklin Financial Services | 10.4x | 2.0x | 33.63% | ★★★☆☆☆ |

| Delek US Holdings | NA | 0.1x | -72.89% | ★★★☆☆☆ |

| Sabre | NA | 0.4x | -35.48% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

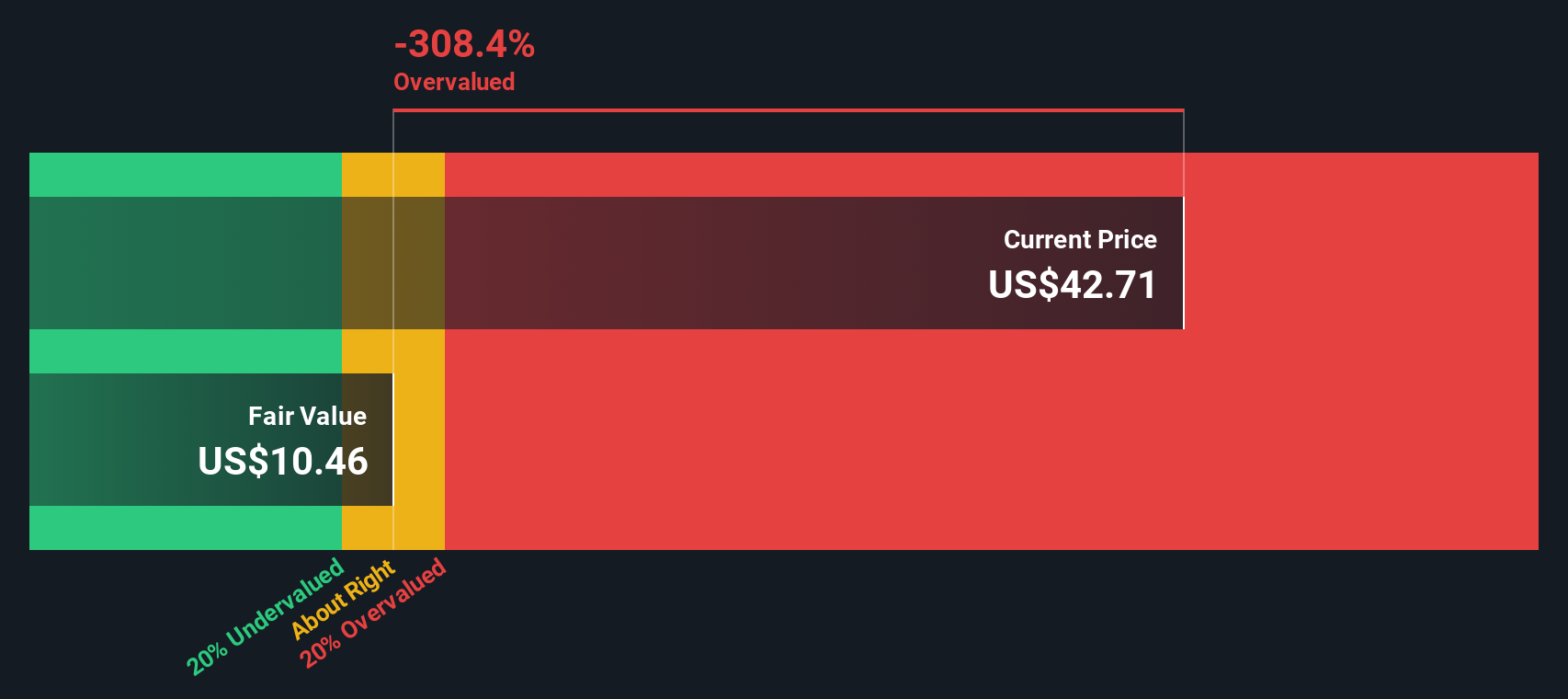

Semler Scientific (NasdaqCM:SMLR)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Semler Scientific specializes in developing and marketing diagnostic kits and equipment, with a market capitalization of approximately $0.21 billion.

Operations: The company generates revenue primarily from diagnostic kits and equipment, with a recent gross profit margin of 88.05%. Operating expenses are significant, with sales and marketing expenses being the largest component. Net income margin has shown fluctuations, most recently recorded at 27.00%.

PE: 30.5x

Semler Scientific, a small-cap company in the U.S., recently completed an $85 million fixed-income offering with convertible notes due in 2030. Despite volatile share prices and reliance on external borrowing, they show insider confidence through recent purchases. Earnings have been stable, with third-quarter net income at US$5.61 million compared to US$5.51 million last year, although revenue decreased to US$13.51 million from US$16.32 million. Future earnings are projected to decline annually by 5.6% over the next three years, highlighting potential challenges amidst its undervalued status.

- Navigate through the intricacies of Semler Scientific with our comprehensive valuation report here.

Understand Semler Scientific's track record by examining our Past report.

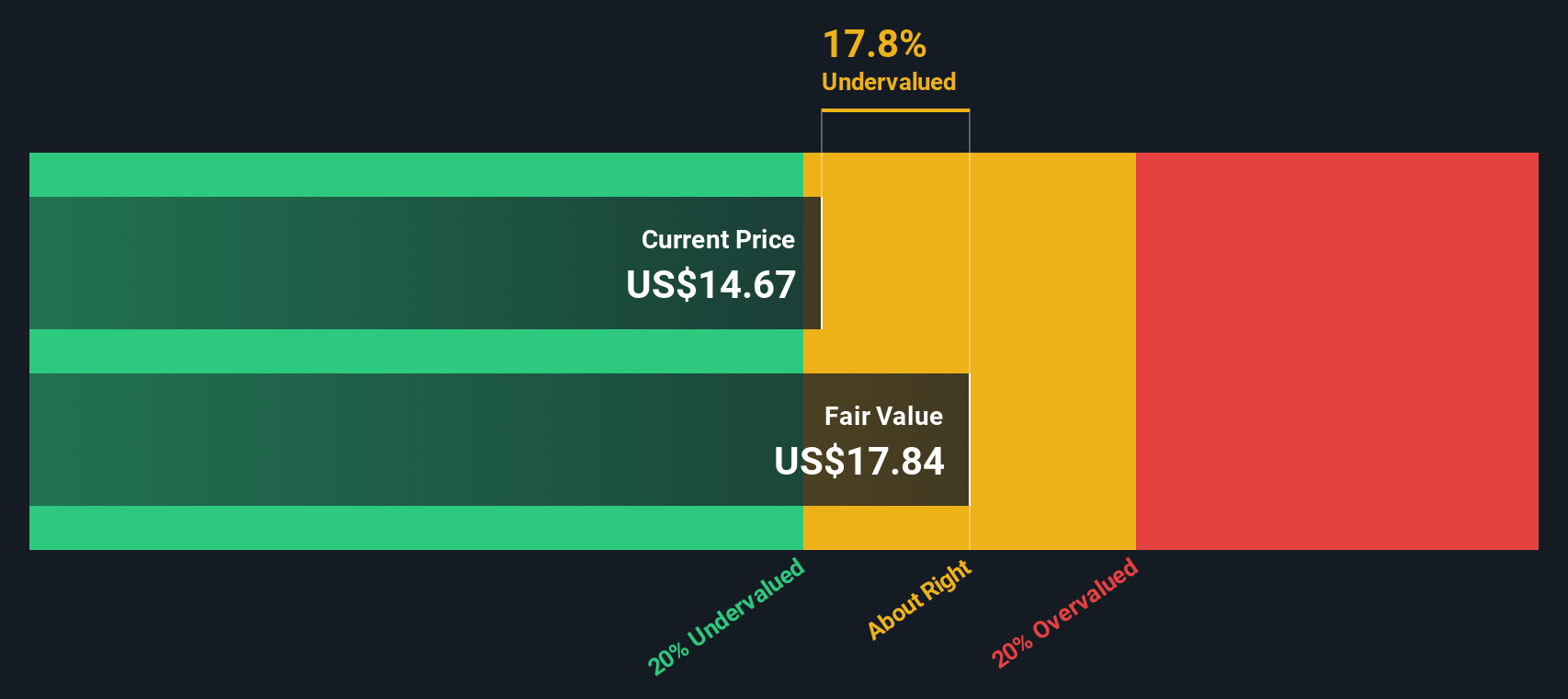

Myers Industries (NYSE:MYE)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Myers Industries is a diversified manufacturing and distribution company primarily focused on material handling and distribution products, with a market cap of approximately $0.85 billion.

Operations: The company generates revenue primarily through its Material Handling and Distribution segments, with the former contributing significantly more. Over recent periods, the gross profit margin has shown a trend of fluctuation, reaching 32.34% in September 2024. Operating expenses have been a consistent part of the cost structure, impacting net income margins which varied notably over time.

PE: 29.1x

Myers Industries, a smaller U.S. company, faces challenges with profit margins dropping from 6% to 1.9% and a net loss of US$10.88 million in Q3 2024. Despite these setbacks, earnings are projected to grow significantly by 72.92% annually, indicating potential upside for investors seeking value opportunities in smaller firms. Leadership changes bring Aaron Schapper as CEO and President from January 2025, potentially revitalizing strategy with his extensive industrial experience at Valmont Industries.

- Click here to discover the nuances of Myers Industries with our detailed analytical valuation report.

Assess Myers Industries' past performance with our detailed historical performance reports.

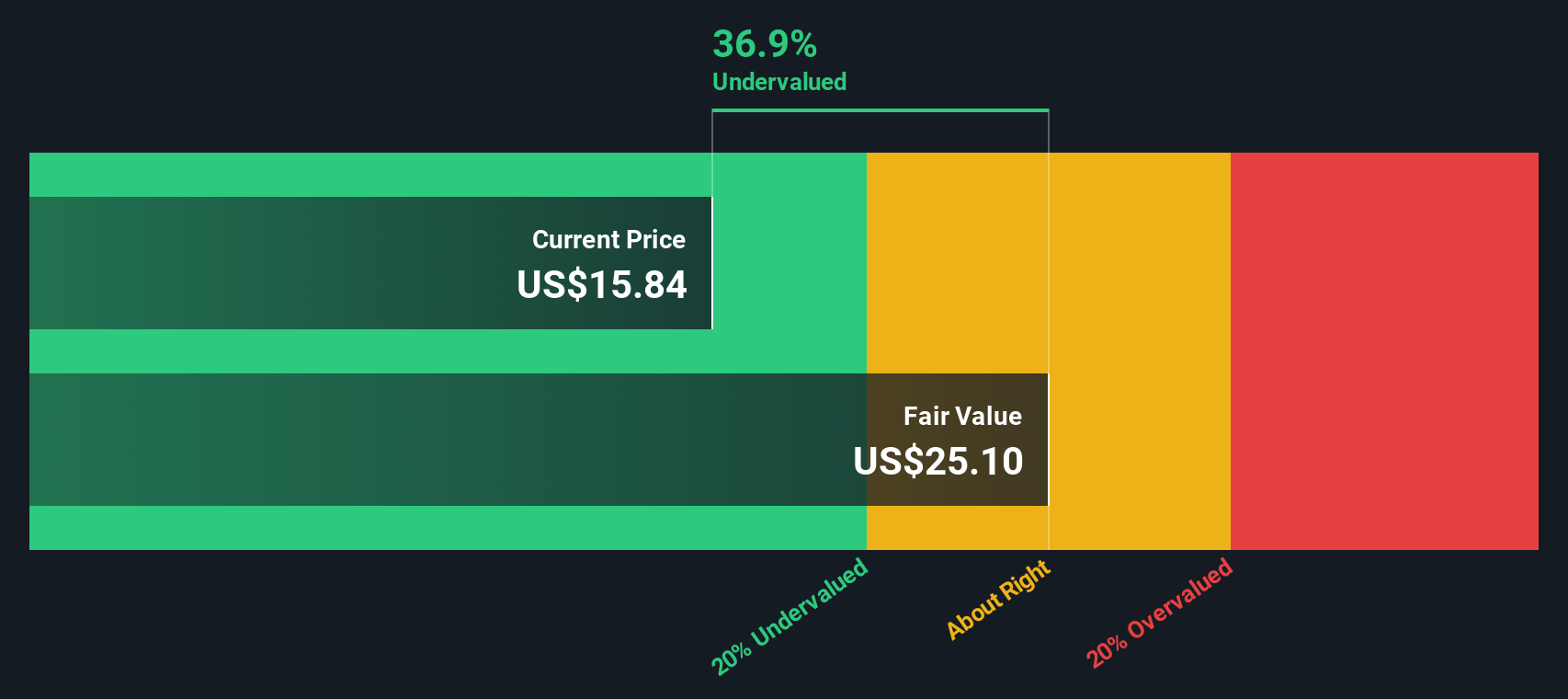

Plymouth Industrial REIT (NYSE:PLYM)

Simply Wall St Value Rating: ★★★★★☆

Overview: Plymouth Industrial REIT focuses on owning and operating industrial properties, with a market capitalization of approximately $1.13 billion.

Operations: The company primarily generates revenue from its industrial properties, with a recent gross profit margin of 68.88%. Operating expenses and non-operating expenses are significant components of the cost structure, impacting net income.

PE: 906.2x

Plymouth Industrial REIT, a small-cap player in the industrial real estate sector, has recently executed a significant two-year lease in St. Louis with an international client, enhancing its occupancy and revenue stream. The company acquired properties in Cincinnati for US$20.1 million with a promising yield of 6.8%, reflecting strategic expansion efforts. Despite reporting a net loss of US$15.6 million for Q3 2024, insider confidence is evident through share purchases over recent months, indicating potential future value recognition amidst current financial challenges.

- Unlock comprehensive insights into our analysis of Plymouth Industrial REIT stock in this valuation report.

Learn about Plymouth Industrial REIT's historical performance.

Seize The Opportunity

- Click here to access our complete index of 41 Undervalued US Small Caps With Insider Buying.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MYE

Myers Industries

Engages in distribution of tire service supplies in Ohio.

Average dividend payer slight.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor