Advertisement

- United States

- /

- Chemicals

- /

- NYSE:HUN

Is Huntsman’s (HUN) Dividend Strategy Entering a New Chapter After Recent Downgrade?

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this week, Bank of America downgraded Huntsman to underperform and flagged potential dividend risks, citing a challenging US chemicals landscape marked by oversupply, soft demand, and continued destocking pressures.

- This signals mounting concerns about Huntsman’s ability to maintain its dividend coverage as sector-wide earnings pressure and cash flow challenges intensify.

- To assess what this means for investors, we’ll analyze how concerns over Huntsman’s dividend coverage impact its broader investment narrative.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Huntsman Investment Narrative Recap

To be a Huntsman shareholder today, you need faith in the company’s ability to reposition toward higher-margin specialty chemicals despite sector-wide pressure. The Bank of America downgrade introduces fresh concerns about Huntsman’s near-term dividend sustainability, which is now the most important short-term catalyst as well as the stock’s biggest risk. For investors, this warning cannot be ignored, as dividend coverage may directly impact confidence and share price stability.

The most relevant recent announcement is the Q3 2025 dividend declaration, where Huntsman’s board maintained its quarterly US$0.25 payout. This move comes in the context of negative earnings and sector headwinds, intensifying attention on how well the company can balance shareholder returns with cash flow discipline. With ongoing macroeconomic weakness and coverage concerns, investors will likely scrutinize upcoming results and guidance for any signal of change.

But while Huntsman continues to signal stability, mounting pressure on margins and dividend coverage should remind investors that...

Read the full narrative on Huntsman (it's free!)

Huntsman's narrative projects $6.4 billion revenue and $43.7 million earnings by 2028. This requires 2.7% yearly revenue growth and a $353.7 million earnings increase from -$310.0 million.

Uncover how Huntsman's forecasts yield a $10.73 fair value, a 31% upside to its current price.

Exploring Other Perspectives

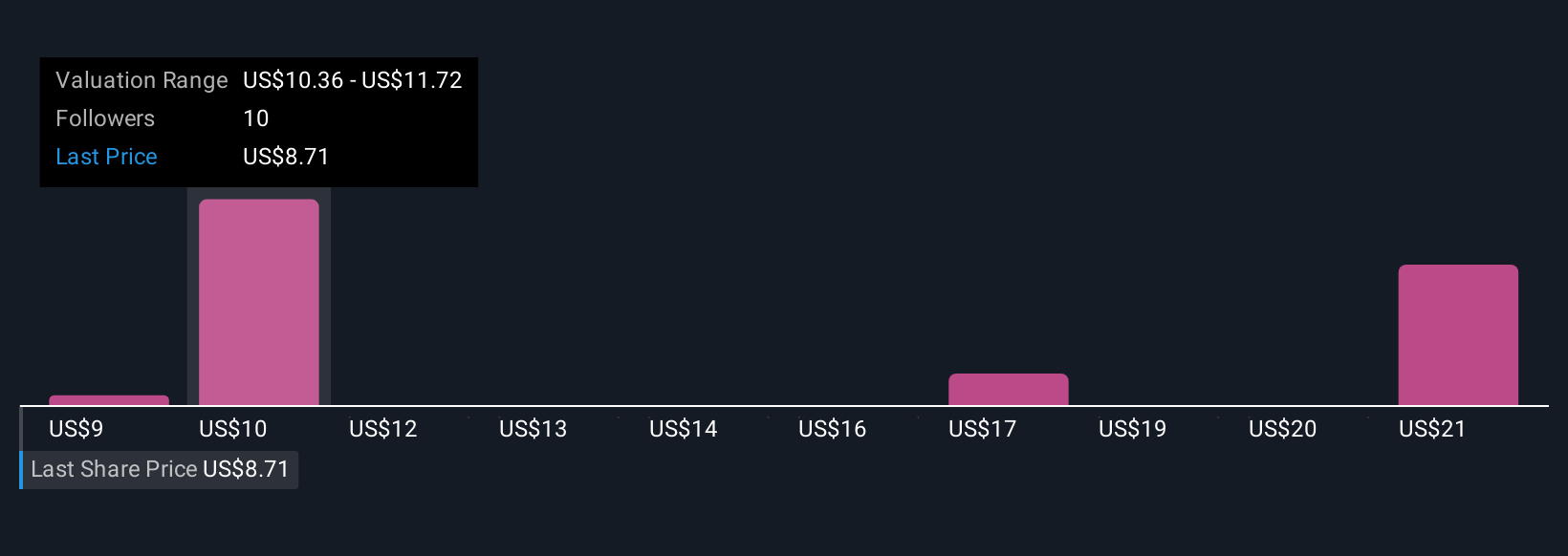

Five Simply Wall St Community fair value estimates for Huntsman range from US$9.00 to US$21.45, reflecting significant uncertainty around intrinsic value. In light of new warnings on dividend sustainability, it’s clear that views on business risk and margin pressure can lead to sharply different opinions, explore why the outlook varies so widely.

Explore 5 other fair value estimates on Huntsman - why the stock might be worth over 2x more than the current price!

Build Your Own Huntsman Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Huntsman research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Huntsman research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Huntsman's overall financial health at a glance.

Looking For Alternative Opportunities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 38 best rare earth metal stocks of the very few that mine this essential strategic resource.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Huntsman might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HUN

Huntsman

Manufactures and sells diversified organic chemical products worldwide.

Undervalued average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.1% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|11.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|39.4% undervalued

TR

Community Contributor