Advertisement

- United States

- /

- Metals and Mining

- /

- NYSE:HCC

Warrior Met Coal (HCC) Starts Blue Creek Sales Early—What Does This Mean for Its Growth Strategy?

Simply Wall St

Reviewed by Simply Wall St

- Warrior Met Coal recently released its second quarter 2025 results, reporting revenue of US$297.52 million and net income of US$5.61 million, as well as the first commercial sales from its Blue Creek mine ahead of schedule. The company also maintained its quarterly dividend, updated full-year production guidance, and amended its bylaws regarding stockholder meeting notices.

- Achieving earlier-than-expected sales from the Blue Creek mine marks a milestone for Warrior Met Coal, transitioning the project from capital investment to revenue generation amidst ongoing challenging market conditions for steelmaking coal.

- We'll examine how the ahead-of-schedule Blue Creek mine sales and Q2 results affect Warrior Met Coal’s investment narrative and outlook.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 20 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Warrior Met Coal Investment Narrative Recap

To be a shareholder in Warrior Met Coal, you need to believe that investments like the Blue Creek mine can help counter persistent weakness in global steelmaking coal markets and position the business for eventual margin and profitability improvement. The early Blue Creek sales are encouraging for future growth, but the short-term catalyst, ramping up production without a recovery in coal prices, remains tied to external demand, and the biggest risk continues to be pressured pricing and weak global steel demand, which are not materially changed by the Q2 results.

The company’s recent affirmation of its regular quarterly cash dividend at US$0.08 per share stands out, especially given ongoing market pressures and lower earnings. Sustaining shareholder distributions amid these headwinds ties back to the central question of whether cost controls, operational improvements, and early Blue Creek output can support the business until sector conditions improve, or if persistent market challenges might eventually force a shift in capital allocation priorities.

By contrast, investors should also be aware of the ongoing risks around steelmaking coal prices and the effects these could have if global demand does not recover...

Read the full narrative on Warrior Met Coal (it's free!)

Warrior Met Coal's outlook anticipates $2.0 billion in revenue and $395.2 million in earnings by 2028. This scenario assumes annual revenue growth of 15.7% and a $289.8 million increase in earnings from the current $105.4 million.

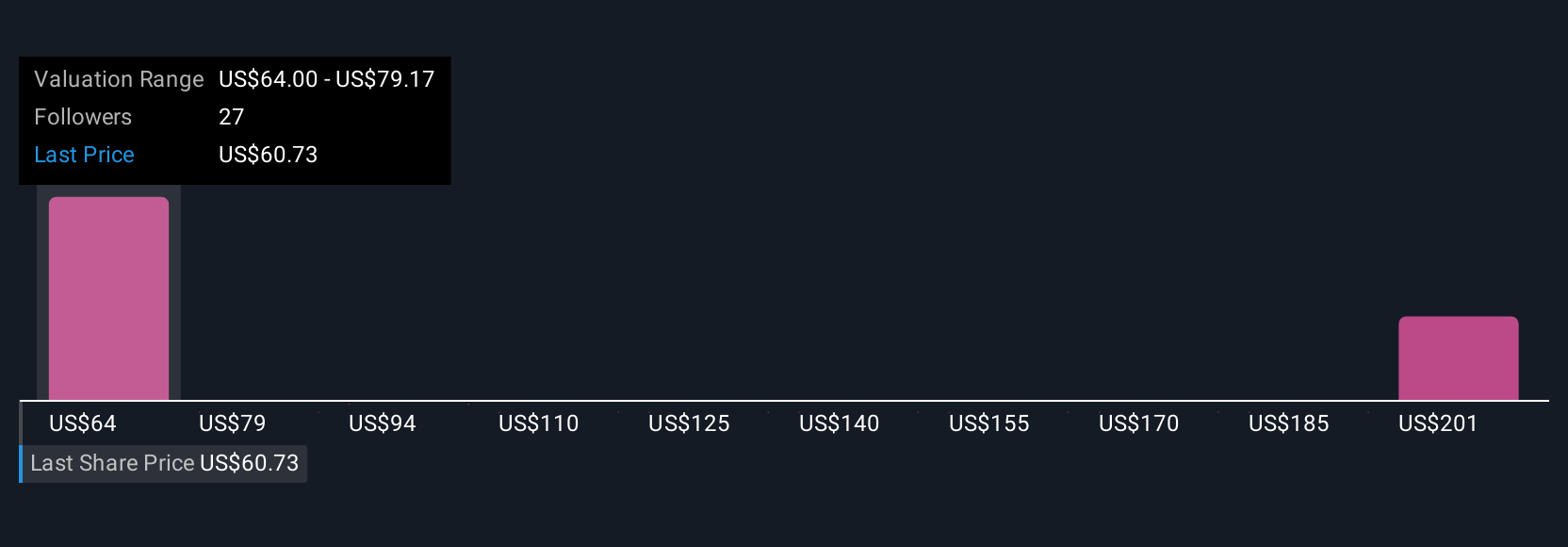

Uncover how Warrior Met Coal's forecasts yield a $64.00 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Five Simply Wall St Community fair value estimates for Warrior Met Coal range from US$64 to US$215, with most clustering below US$155. While these diverse views reflect sharply different expectations, persistent market headwinds remain a clear concern for future performance. Explore the full range of opinions and see how your own outlook compares.

Explore 5 other fair value estimates on Warrior Met Coal - why the stock might be worth over 3x more than the current price!

Build Your Own Warrior Met Coal Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Warrior Met Coal research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Warrior Met Coal research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Warrior Met Coal's overall financial health at a glance.

Contemplating Other Strategies?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 24 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Warrior Met Coal might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HCC

Warrior Met Coal

Engages in the production and export of non-thermal steelmaking coal for the steel production by metal manufacturers in Europe, South America, and Asia.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|57.7% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|20.6% undervalued

ZW

Community Contributor