- United States

- /

- Basic Materials

- /

- NYSE:EXP

Eagle Materials (EXP) Valuation After L1 Capital’s Exit on Housing and Wallboard Demand Concerns

Reviewed by Simply Wall St

L1 Capital International’s decision to fully exit Eagle Materials (EXP) puts a spotlight on brewing headwinds, from a softer housing cycle and affordability strain to weaker expectations for wallboard demand and cement pricing.

See our latest analysis for Eagle Materials.

Those worries have hit sentiment, with Eagle Materials’ share price now at $222.76 and showing a negative year to date share price return. Its five year total shareholder return remains strongly positive, suggesting long term momentum is intact but fading in the near term.

If you are weighing whether this housing linked weakness signals risk or opportunity, it is a good moment to broaden your search and discover fast growing stocks with high insider ownership.

With earnings still growing and the shares trading at a sizeable discount to some intrinsic value estimates, investors now face a key question: is Eagle Materials a mispriced cyclical buy, or has the market already factored in its future growth?

Most Popular Narrative Narrative: 11.5% Undervalued

With Eagle Materials last closing at $222.76 against a most popular narrative fair value near $251.70, the valuation hinges on steady growth and resilient margins.

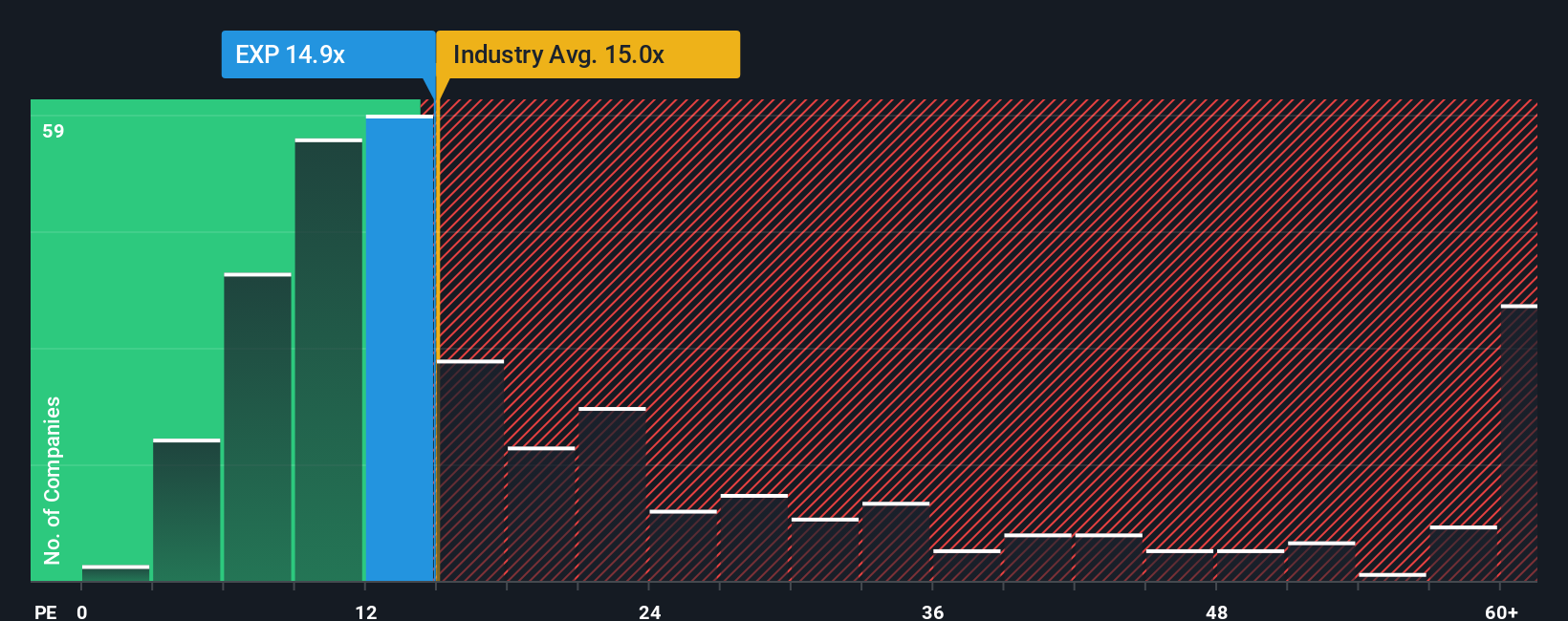

In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 17.3x on those 2028 earnings, up from 16.4x today. This future PE is lower than the current PE for the US Basic Materials industry at 24.1x.

Curious how modest revenue growth, firmer margins and shrinking share count can still support a richer earnings multiple than today? The narrative math might surprise you.

Result: Fair Value of $251.70 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, prolonged housing affordability pressures and regional concentration mean that weaker wallboard demand or localized slowdowns could still derail this undervaluation narrative.

Find out about the key risks to this Eagle Materials narrative.

Another View: Market Multiples Send a Different Signal

On simple earnings multiples, Eagle Materials looks less generous. Its P E ratio of about 16 times is slightly above the global Basic Materials average of 15 times, yet still below peers at 26.7 times and our own fair ratio estimate of 18.2 times.

That mix of modest premium to the wider industry but discount to peers and the fair ratio hints at a middle ground, not a screaming bargain or a clear bubble. It leaves investors to ask whether the next move in sentiment tilts toward risk or opportunity.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Eagle Materials Narrative

If this view does not quite match your own, or you prefer to dig into the numbers yourself, you can build a custom narrative in minutes: Do it your way.

A great starting point for your Eagle Materials research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Do not stop at one opportunity. Your next outperformer could be hiding in plain sight among tailored sets of stocks built around the themes that matter most to you.

- Capture potential multi baggers early by scanning these 3625 penny stocks with strong financials with strong balance sheets and fundamentals before broader markets catch on.

- Ride structural trends in automation and data by targeting these 25 AI penny stocks positioned to benefit from demand for intelligent software and infrastructure.

- Secure quality at a sensible price by focusing on these 909 undervalued stocks based on cash flows that current market sentiment may be mispricing relative to their long term cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Eagle Materials might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EXP

Eagle Materials

Through its subsidiaries, manufactures and sells heavy construction products and light building materials in the United States.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)