Advertisement

- United States

- /

- Chemicals

- /

- NYSE:ECL

Does Ecolab (ECL) Justify Its Rich Valuation After Strong Multi‑Year Share Price Gains?

Reviewed by Bailey Pemberton

- If you are wondering whether Ecolab’s current share price really matches what you are getting as an investor, this article walks through the key numbers so you can judge value for yourself.

- Ecolab’s stock recently closed at US$271.53, with returns of 2.7% over 7 days, 4.6% over 30 days, 3.4% year to date, 18.5% over 1 year, 84.2% over 3 years and 28.5% over 5 years that many investors may want to put in context.

- Recent news coverage around Ecolab has largely focused on its role in water, hygiene and infection prevention solutions, as these remain core themes for many institutional and retail investors. This backdrop helps explain why some market participants are paying closer attention to the stock’s long term potential and risk profile.

- Despite this interest, Ecolab currently has a valuation score of 0 out of 6, so we will look at what different valuation methods say about the stock’s pricing and then finish with a way to think about value that goes beyond the usual models.

Ecolab scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

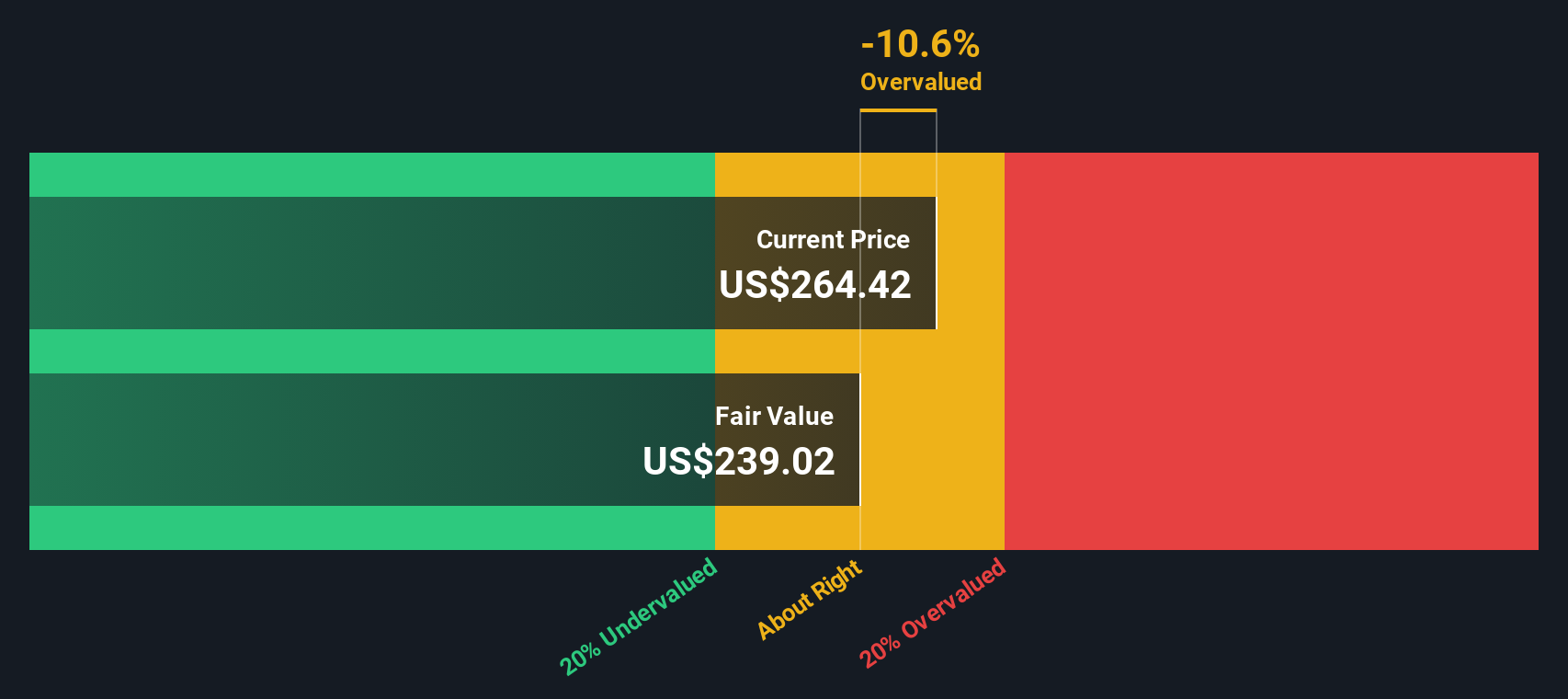

Approach 1: Ecolab Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes the cash Ecolab is expected to generate in the future and then discounts those cash flows back into today’s dollars to estimate what the business might be worth right now.

For Ecolab, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections. The latest twelve month free cash flow is about $1.71b. Analyst inputs cover several years ahead, for example a projected free cash flow of $2.71b in 2028, with further years extrapolated by Simply Wall St out to 2035.

When these projected cash flows are discounted back to today, the resulting estimated intrinsic value from this DCF is US$227.96 per share. Compared with the recent share price of US$271.53, the model implies the stock is about 19.1% above this estimate, which points to Ecolab trading at a premium to this particular cash flow based view of value.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Ecolab may be overvalued by 19.1%. Discover 877 undervalued stocks or create your own screener to find better value opportunities.

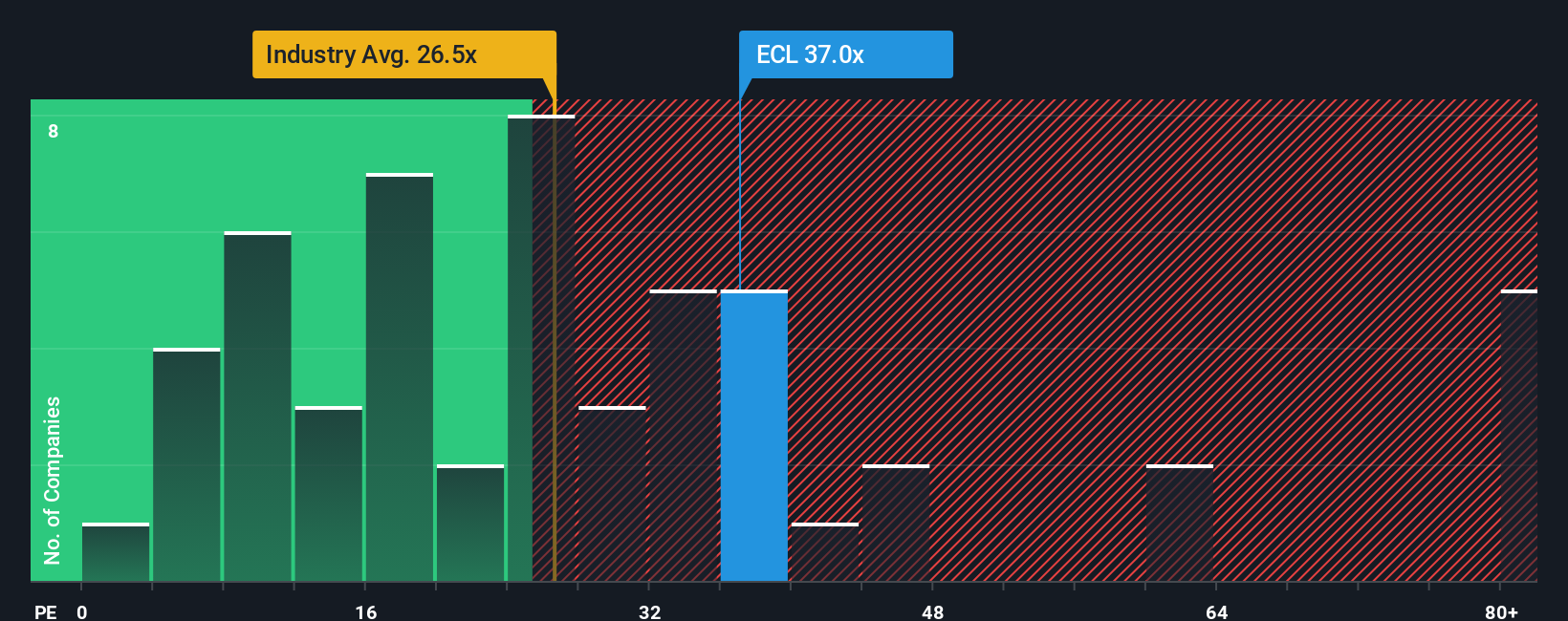

Approach 2: Ecolab Price vs Earnings

For a profitable company like Ecolab, the P/E ratio is a useful way to think about what you are paying for each dollar of current earnings. Investors typically accept a higher P/E when they expect stronger growth or see lower risk, and a lower P/E when growth expectations are more modest or the risk profile is higher.

Ecolab currently trades on a P/E of 38.75x. This sits above the Chemicals industry average P/E of 24.86x and the peer average of 24.09x, which indicates the market is placing a richer price on Ecolab’s earnings than on many of its sector peers.

Simply Wall St’s Fair Ratio for Ecolab is 25.33x. This is a proprietary estimate of what a more normal P/E might look like after considering factors such as earnings growth, industry, profit margins, market cap and company specific risks. Because it blends these drivers together, the Fair Ratio can be a more tailored yardstick than a simple comparison to peers or the industry average. Setting the current P/E of 38.75x against the Fair Ratio of 25.33x suggests the shares are trading above this customised view of fair value.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1450 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Ecolab Narrative

Earlier we mentioned that there is an even better way to think about value, and on Simply Wall St that starts with Narratives. You set out your own story for Ecolab, link that story to specific assumptions for future revenue, earnings and margins, and then see how that feeds into a Fair Value that you can compare with today’s share price. Narratives on the Community page update automatically when new news or earnings arrive. For example, one Ecolab investor might build a Narrative close to the more bullish US$325 fair value, while another might anchor on the more cautious US$243 view. You can see your own Narrative, and others, side by side without needing to build a full spreadsheet model yourself.

Do you think there's more to the story for Ecolab? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Ecolab might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ECL

Ecolab

Provides water, hygiene, and infection prevention solutions and services in the United States and internationally.

Average dividend payer with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5362.1% undervalued

132 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

DE

Degen_GCR on Everpure ·

Second order memory play likely to double in a year

Fair Value:US$18053.7% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

DO

Double_Bubbler on Intuitive Machines ·

Intuitive Machines: To The Moon and Beyond!

Fair Value:US$42.324.1% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

YI

yiannisz on AppLovin ·

AppLovin’s AI Engine Is Printing Profit

Fair Value:US$989.2450.4% undervalued

22 followersusers have followed this narrative

1 commentusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

OI

Oily on MV Oil Trust ·

Poor analysis here will mislead investors

Fair Value:US$2.11.0% undervalued

0 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ZH

zhalia on Lynas Rare Earths ·

Lynas Rare Earths to Shine with 281% Future P/E Surge

Fair Value:AU$22.8714.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Roche Holding ·

Roche is a cash-generating, defensive large-cap pharma, with upside driven by pipeline execution.

Fair Value:CHF 353.349.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.1% undervalued

108 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.227.7% undervalued

70 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74018.5% undervalued

35 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative