Advertisement

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Corteva, Inc. (NYSE:CTVA) does carry debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Corteva

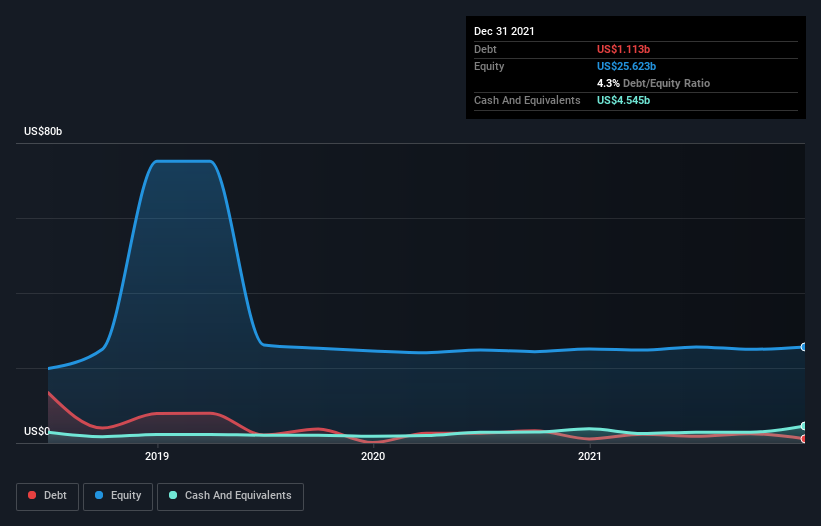

What Is Corteva's Net Debt?

The chart below, which you can click on for greater detail, shows that Corteva had US$1.11b in debt in December 2021; about the same as the year before. However, its balance sheet shows it holds US$4.55b in cash, so it actually has US$3.43b net cash.

A Look At Corteva's Liabilities

The latest balance sheet data shows that Corteva had liabilities of US$9.56b due within a year, and liabilities of US$7.16b falling due after that. Offsetting this, it had US$4.55b in cash and US$4.84b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$7.34b.

Of course, Corteva has a titanic market capitalization of US$42.4b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. While it does have liabilities worth noting, Corteva also has more cash than debt, so we're pretty confident it can manage its debt safely.

Better yet, Corteva grew its EBIT by 118% last year, which is an impressive improvement. If maintained that growth will make the debt even more manageable in the years ahead. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Corteva's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Corteva has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, Corteva produced sturdy free cash flow equating to 75% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

Although Corteva's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$3.43b. And it impressed us with its EBIT growth of 118% over the last year. So is Corteva's debt a risk? It doesn't seem so to us. Another factor that would give us confidence in Corteva would be if insiders have been buying shares: if you're conscious of that signal too, you can find out instantly by clicking this link.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:CTVA

Excellent balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|36.3% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor