- United States

- /

- Metals and Mining

- /

- NYSE:CLF

Cleveland-Cliffs (CLF) Reports Q2 2025 Sales Decline to US$4934 Million

Reviewed by Simply Wall St

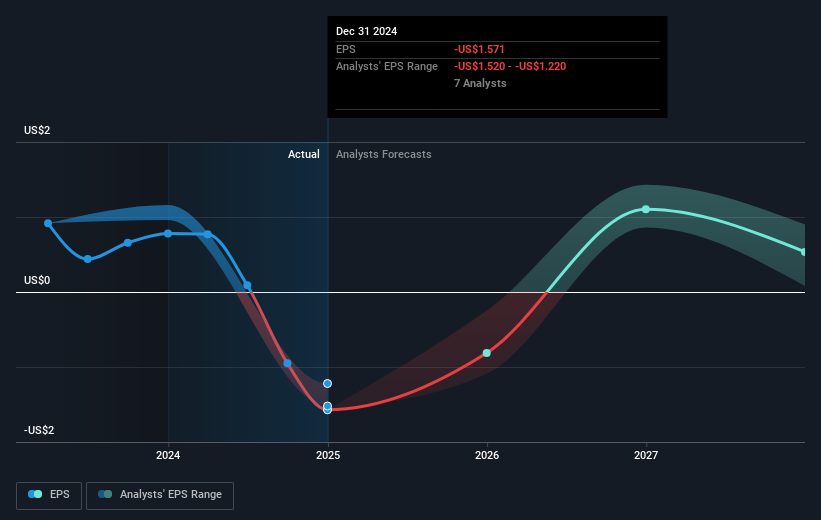

Cleveland-Cliffs (CLF) recently faced challenges as their second-quarter 2025 earnings revealed sales declined to USD 4,934 million, while registering a net loss of USD 483 million compared to a modest net income last year. Despite these disappointing financial results, Cleveland-Cliffs's share price rose by 15% over the past month. This performance unfolded against the backdrop of a broader market that saw similar gains in July, although markets experienced a downturn due to economic concerns fueled by weak U.S. jobs data and renewed tariff policies. The company's operational struggles might have tempered the overall positive market momentum.

Find companies with promising cash flow potential yet trading below their fair value.

The recent earnings report highlighting Cleveland-Cliffs' net loss of US$483 million amidst sales of US$4.93 billion presents a challenging landscape for the company. Despite this, shares have climbed 15% in the past month, reflecting broader market trends, though these gains might be vulnerable to ongoing economic uncertainties, such as the U.S. jobs data concerns. Addressing this financial strain is crucial as Cleveland-Cliffs navigates its reliance on U.S. steel tariffs and OEM reshoring, central to its growth narrative.

Over a longer five-year period, Cleveland-Cliffs' total shareholder return, encompassing both share price appreciation and dividends, marked an impressive increase of 83.58%. This growth sharply contrasts with the company's recent underperformance against the US Metals and Mining industry over the past year. The industry saw returns of 13.4%, surpassing Cleveland-Cliffs' performance during the same one-year period.

Future revenue and earnings projections are aligned with anticipated benefits from reshoring and tariff protections, yet the magnitude of the recent loss highlights potential vulnerabilities. Analysts anticipate the revenue will rise, with margins eventually reaching profitability. However, any shifts in trade policies or market conditions could alter these forecasts. With the current share price at US$10.06, close to the target of US$10.99, the upward movement suggests market confidence, yet analysts see limited upside relative to the target, indicating cautious optimism about hitting expected milestones.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CLF

Cleveland-Cliffs

Operates as a flat-rolled steel producer in the United States, Canada, and internationally.

Good value with moderate growth potential.

Similar Companies

Market Insights

Community Narratives