Advertisement

- United States

- /

- Metals and Mining

- /

- NYSE:CDE

Does Expanding Rochester and Las Chispas Change the Bull Case for Coeur Mining (CDE)?

Simply Wall St

Reviewed by Sasha Jovanovic

- In recent weeks, Coeur Mining's operational progress at the Rochester expansion and Las Chispas asset has drawn attention for sharply increasing its silver and gold production capabilities. This operational milestone has driven growing investor optimism about the company's potential for revenue growth and stronger margins in the near to medium term.

- An important implication of the Rochester and Las Chispas ramp-up is their significant impact on Coeur Mining’s future production outlook and investor confidence in its key projects.

- We'll examine how the successful integration of these major mining assets could strengthen Coeur's long-term investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 34 best rare earth metal stocks of the very few that mine this essential strategic resource.

Coeur Mining Investment Narrative Recap

To be a shareholder in Coeur Mining, you have to believe that recent operational success at the Rochester and Las Chispas mines can drive substantial, sustained growth in silver and gold production, fueling improved financial results. The surge in the share price and improving earnings position the company well for short-term performance, but the heightened risk of regulatory setbacks at key projects remains a factor that could materially affect growth if delays develop.

One of the most relevant updates to watch is Coeur's reaffirmation of its 2025 production guidance, which underscores management's confidence in executing its ramp-up at Rochester and Las Chispas. This provides a key reference point for investors monitoring whether the company can deliver on near-term output goals, a critical catalyst as expanded production will be central to the investment narrative moving forward.

By contrast, investors should also be aware of how unexpected regulatory or permitting issues could...

Read the full narrative on Coeur Mining (it's free!)

Coeur Mining’s outlook anticipates $2.1 billion in revenue and $676.1 million in earnings by 2028. This relies on an annual revenue growth rate of 12.8% and a $485.4 million increase in earnings from the current $190.7 million.

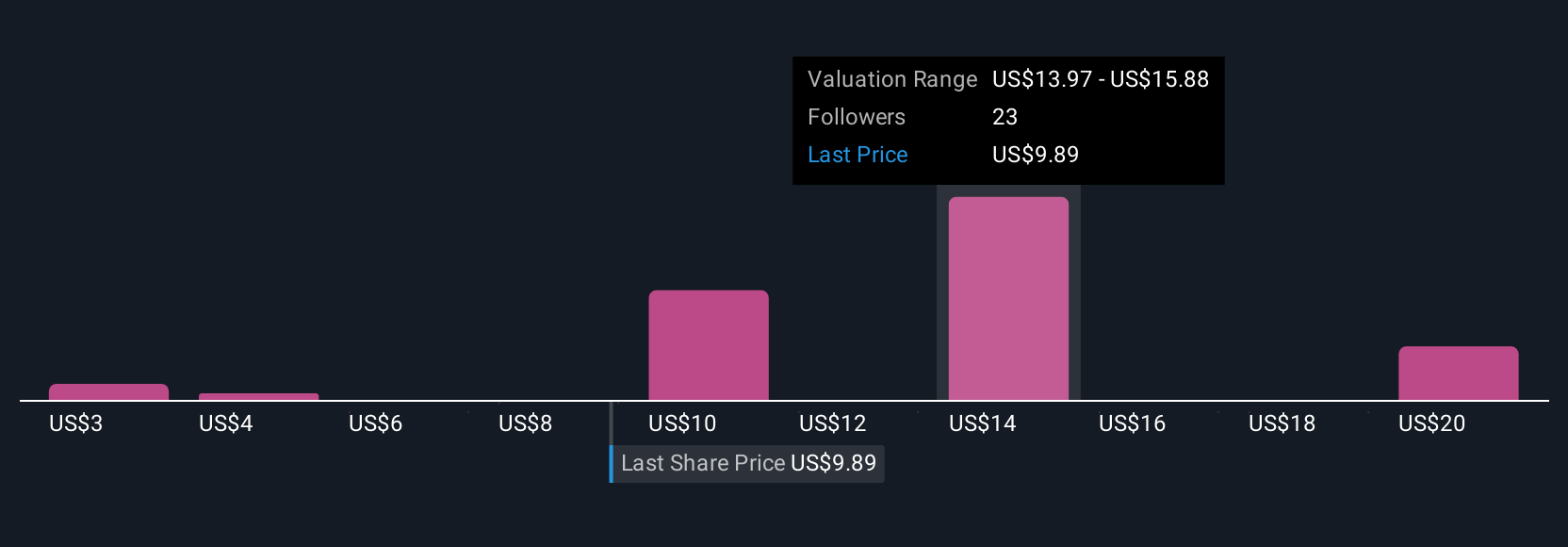

Uncover how Coeur Mining's forecasts yield a $17.03 fair value, a 9% downside to its current price.

Exploring Other Perspectives

Simply Wall St Community members shared nine fair value estimates for Coeur Mining, ranging widely from US$2.52 to US$21.60 per share. As production ramps up, investors should weigh whether regulatory and permitting risks could limit the company’s ability to capture revenue potential seen in these forecasts.

Explore 9 other fair value estimates on Coeur Mining - why the stock might be worth less than half the current price!

Build Your Own Coeur Mining Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Coeur Mining research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Coeur Mining research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Coeur Mining's overall financial health at a glance.

Curious About Other Options?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CDE

Coeur Mining

Operates as a gold and silver producer in the United States, Canada, and Mexico.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor