- United States

- /

- Insurance

- /

- NYSE:WRB

Earnings Growth and Product Enhancements Might Change The Case For Investing In W. R. Berkley (WRB)

Reviewed by Simply Wall St

- W. R. Berkley recently reported its second quarter 2025 earnings, announcing revenue of US$3.67 billion and net income of US$401.29 million, both higher than the same period last year, while also unveiling product enhancements for collector vehicle insurance in Georgia and confirming no new shares repurchased in the latest buyback tranche.

- Among several policy updates, Berkley One Classics increased savings for multi-car and collector vehicle accounts, expanded coverage for newly acquired vehicles, and introduced new endorsements to adapt to evolving customer needs.

- We’ll explore how W. R. Berkley’s quarter of revenue and net income growth could influence the company’s longer-term investment outlook.

W. R. Berkley Investment Narrative Recap

To be a W. R. Berkley shareholder, you need to believe in the company’s ability to manage disciplined specialty insurance underwriting and capitalize on ongoing demand for tailored risk solutions. The latest quarter’s revenue and net income growth help reinforce this, but the news does not materially change the most important near-term catalyst, continued premium rate strength, or the biggest risk from growing pricing competition and reinsurance capacity in the property market.

Among the recent updates, Berkley One Classics’ enhancements to collector vehicle policies in Georgia stand out for their potential to keep policyholders engaged and meet evolving customer needs. While this is an example of Berkley’s specialty focus, it does not directly address the broader competitive pressure in core insurance segments, which remains the key variable for both earnings and shareholder returns.

However, investors should also be aware that, as competition intensifies particularly in property and reinsurance lines, the stability of future underwriting profitability will increasingly depend on...

Read the full narrative on W. R. Berkley (it's free!)

W. R. Berkley's narrative projects $14.2 billion revenue and $2.0 billion earnings by 2028. This requires a 0.1% annual revenue decline and a $0.2 billion earnings increase from $1.8 billion today.

Uncover how W. R. Berkley's forecasts yield a $70.70 fair value, in line with its current price.

Exploring Other Perspectives

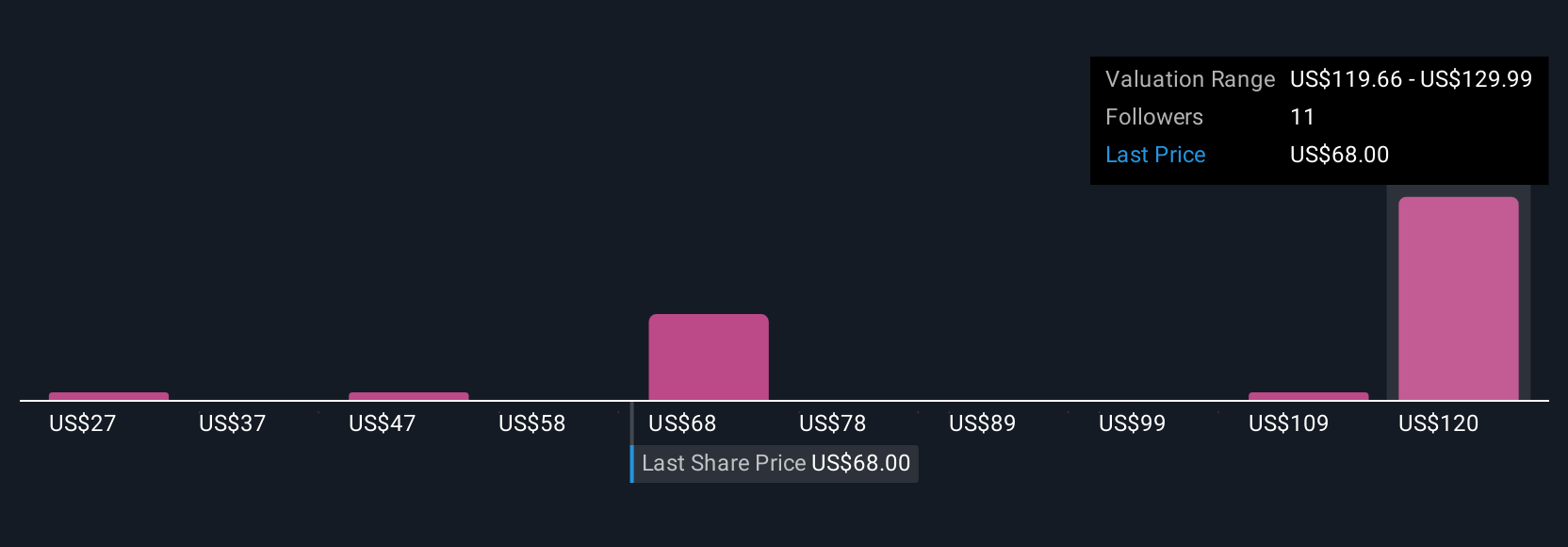

Six Simply Wall St Community fair value estimates for W. R. Berkley range from US$26.69 to US$130.53 per share, capturing a striking spread of expectations. As you consider these contrasting valuations, weigh how broadening competition in insurance markets could influence future profitability and examine several alternative viewpoints for a balanced perspective.

Build Your Own W. R. Berkley Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your W. R. Berkley research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free W. R. Berkley research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate W. R. Berkley's overall financial health at a glance.

No Opportunity In W. R. Berkley?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 25 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Uncover 13 companies that survived and thrived after COVID and have the right ingredients to survive Trump's tariffs.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if W. R. Berkley might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WRB

W. R. Berkley

An insurance holding company, operates as a commercial line writer worldwide.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)