Advertisement

- United States

- /

- Insurance

- /

- NYSE:STC

Is It Too Late to Consider Stewart Information Services After Its Strong Recent Share Price Run?

Simply Wall St

Reviewed by Bailey Pemberton

- If you are wondering whether Stewart Information Services is still good value after its run up, or if most of the upside is already priced in, you are not alone.

- The stock has climbed 11.4% over the last month and is up 16.2% year to date, adding to gains of 96.9% over three years.

- Recently, investors have been watching sector wide shifts in real estate activity and transaction volumes, which directly influence demand for Stewart's title and closing services. Broader optimism around property markets and interest rate expectations has also helped re rate many companies in the space, and Stewart has been part of that move.

- Yet despite this backdrop, Simply Wall St's valuation checks give Stewart Information Services a value score of 0/6. This suggests the market may be paying up relative to traditional metrics. In this article, we will unpack what that really means, compare different valuation approaches, and finish with a more holistic way to think about the stock's overall worth.

Stewart Information Services scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Stewart Information Services Excess Returns Analysis

The Excess Returns model examines whether a company is generating a meaningful return above its cost of equity, based on its book value and sustainable earnings power. Rather than focusing on short term earnings swings, it asks if each dollar of shareholder equity is compounding at an attractive rate over time.

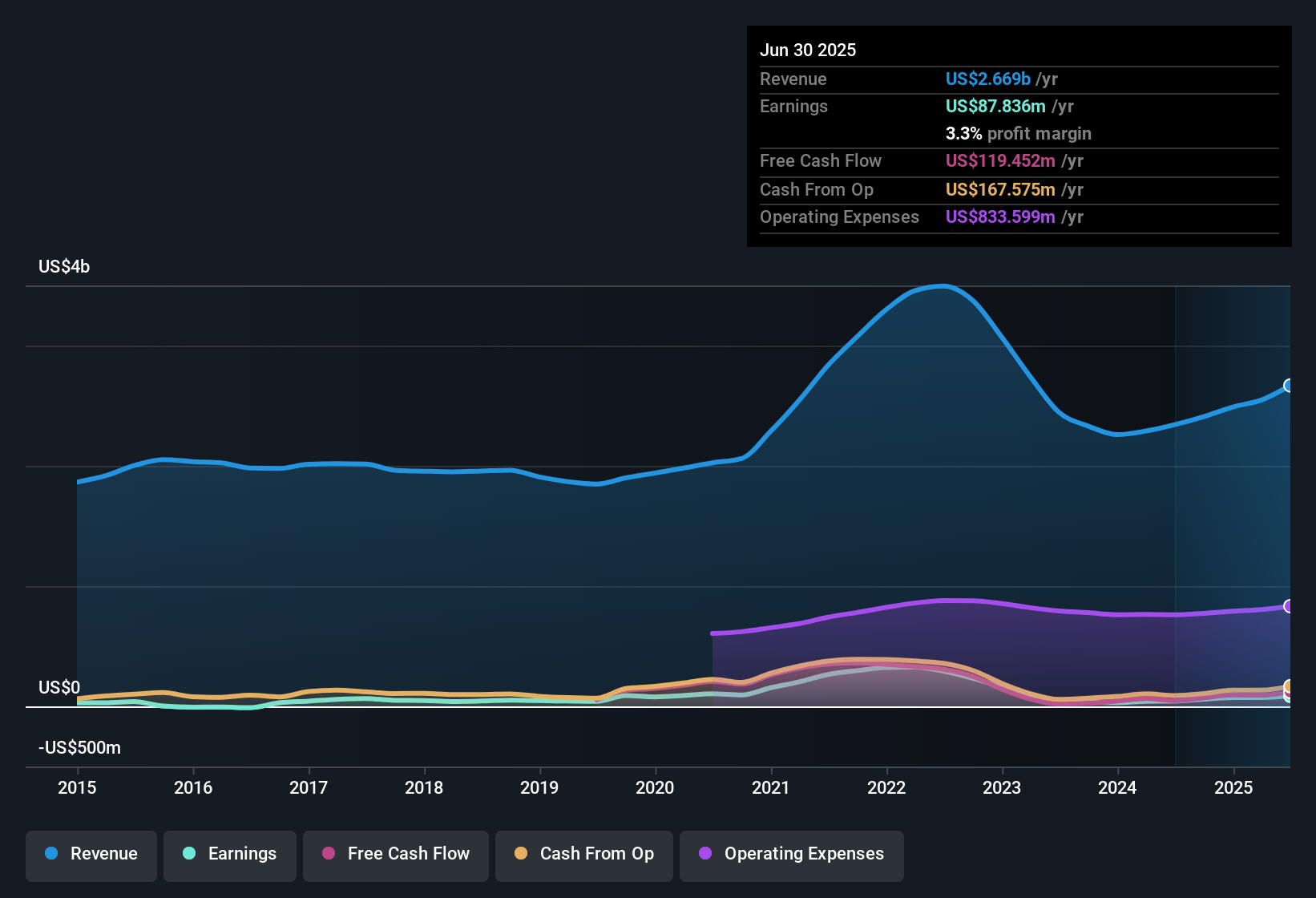

For Stewart Information Services, the model uses a Book Value of $52.59 per share and a Stable EPS estimate of $3.19 per share, derived from the median return on equity over the past 5 years. Against a Cost of Equity of $3.49 per share, this translates into an Excess Return of $-0.29 per share, implying the business is not expected to consistently earn more than its equity cost. The Average Return on Equity of 6.37% and Stable Book Value of $50.11 per share reinforce a view of modest long term compounding rather than high value creation.

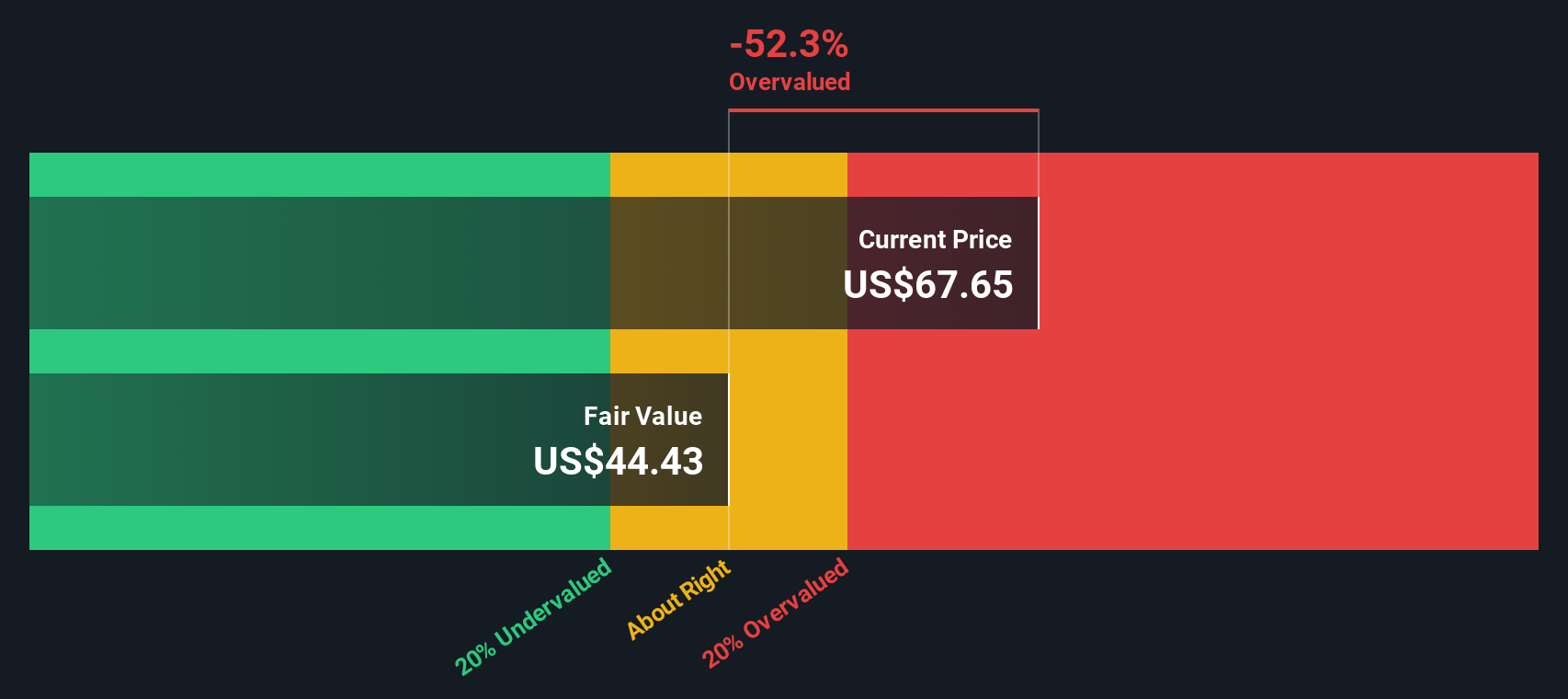

On this basis, the Excess Returns valuation implies the stock is around 81.3% overvalued relative to its estimated intrinsic worth, suggesting the current price builds in much stronger profitability than the historical record supports.

Result: OVERVALUED

Our Excess Returns analysis suggests Stewart Information Services may be overvalued by 81.3%. Discover 925 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Stewart Information Services Price vs Earnings

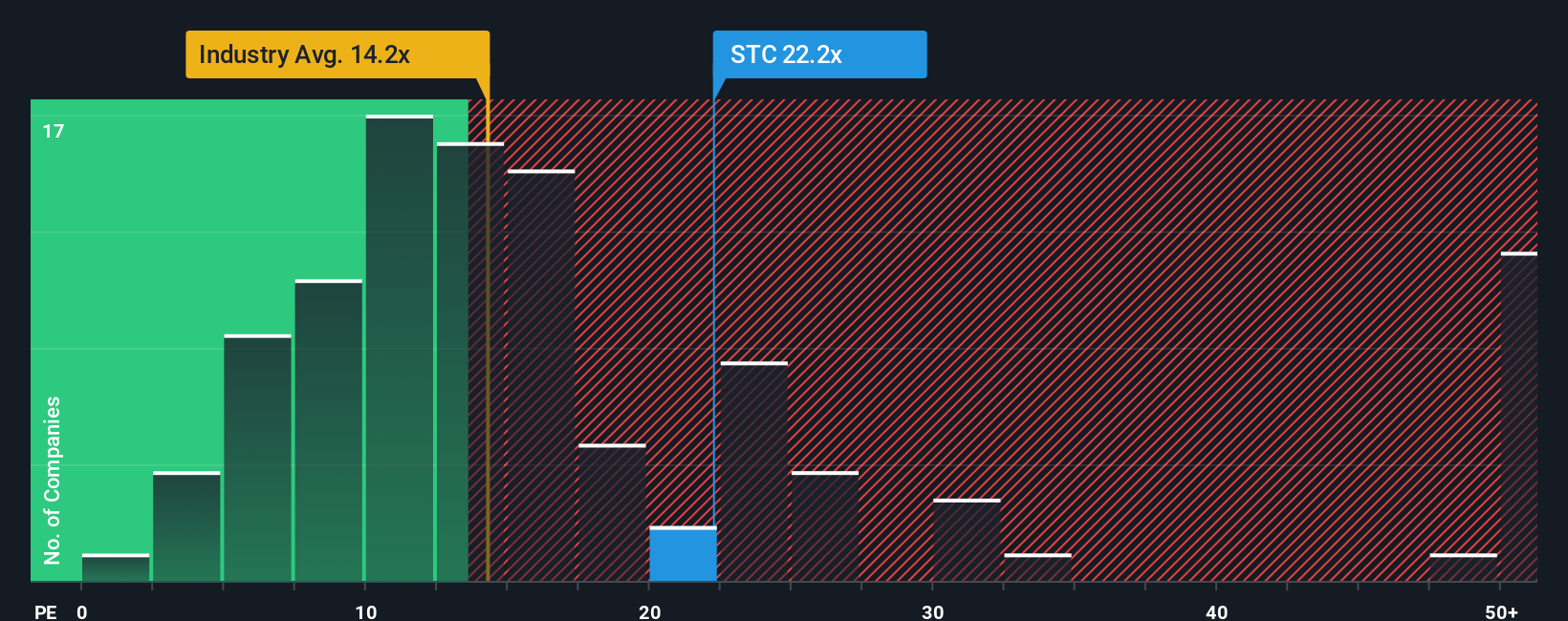

For profitable companies like Stewart Information Services, the price to earnings (PE) ratio is a useful way to gauge how much investors are willing to pay for each dollar of current earnings. A higher PE can be justified when a business is expected to grow faster or is viewed as lower risk. By contrast, slower growth or higher uncertainty usually warrants a lower, more conservative multiple.

Stewart currently trades on a PE of 21.0x, which is comfortably above the broader Insurance industry average of about 13.1x and also ahead of the peer group average of 16.5x. Simply Wall St goes a step further by estimating a Fair Ratio of 20.2x, a proprietary measure that adjusts the PE you would expect for Stewart based on its specific earnings growth profile, margins, risk factors, industry and market cap. This makes it more tailored than simple industry or peer comparisons, which can miss important company level nuances.

Comparing the actual PE of 21.0x with the Fair Ratio of 20.2x suggests the stock is trading at a modest premium to what its fundamentals justify, pointing to a somewhat rich valuation rather than a clear bargain.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1441 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Stewart Information Services Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, a simple framework on Simply Wall St’s Community page that lets you attach a clear story and set of assumptions to a company’s numbers. This allows you to see exactly how its business outlook links to a financial forecast, then to a fair value, and finally to a buy or sell decision as you compare that fair value to the current price and watch it update automatically when new earnings, news, or guidance come in. For Stewart Information Services, for example, one optimistic Narrative might assume mid single digit revenue growth, expanding margins from new digital services like FINCEN Reporting Services, and a steady dividend hike to arrive at a fair value around $80 per share. A more cautious Narrative might assume a weaker housing recovery, stubbornly high costs, and a lower future PE multiple to justify a fair value closer to the low $60s. This clearly shows how different investors can look at the same company and reach very different, but fully transparent, conclusions.

Do you think there's more to the story for Stewart Information Services? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:STC

Stewart Information Services

Through its subsidiaries, provides title insurance and real estate transaction related services in the United States and internationally.

Established dividend payer with proven track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

24 followersusers have followed this narrative

6 commentsusers have commented on this narrative

7 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1919.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5200.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Applied Digital ·

Staggered by dilution; positions for growth

Fair Value:US$35.4520.9% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.5% undervalued

949 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.1% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative