- United States

- /

- Insurance

- /

- NYSE:MMC

Marsh McLennan (MMC) Margin Decline Raises Questions on Sustained Premium Valuation

Reviewed by Simply Wall St

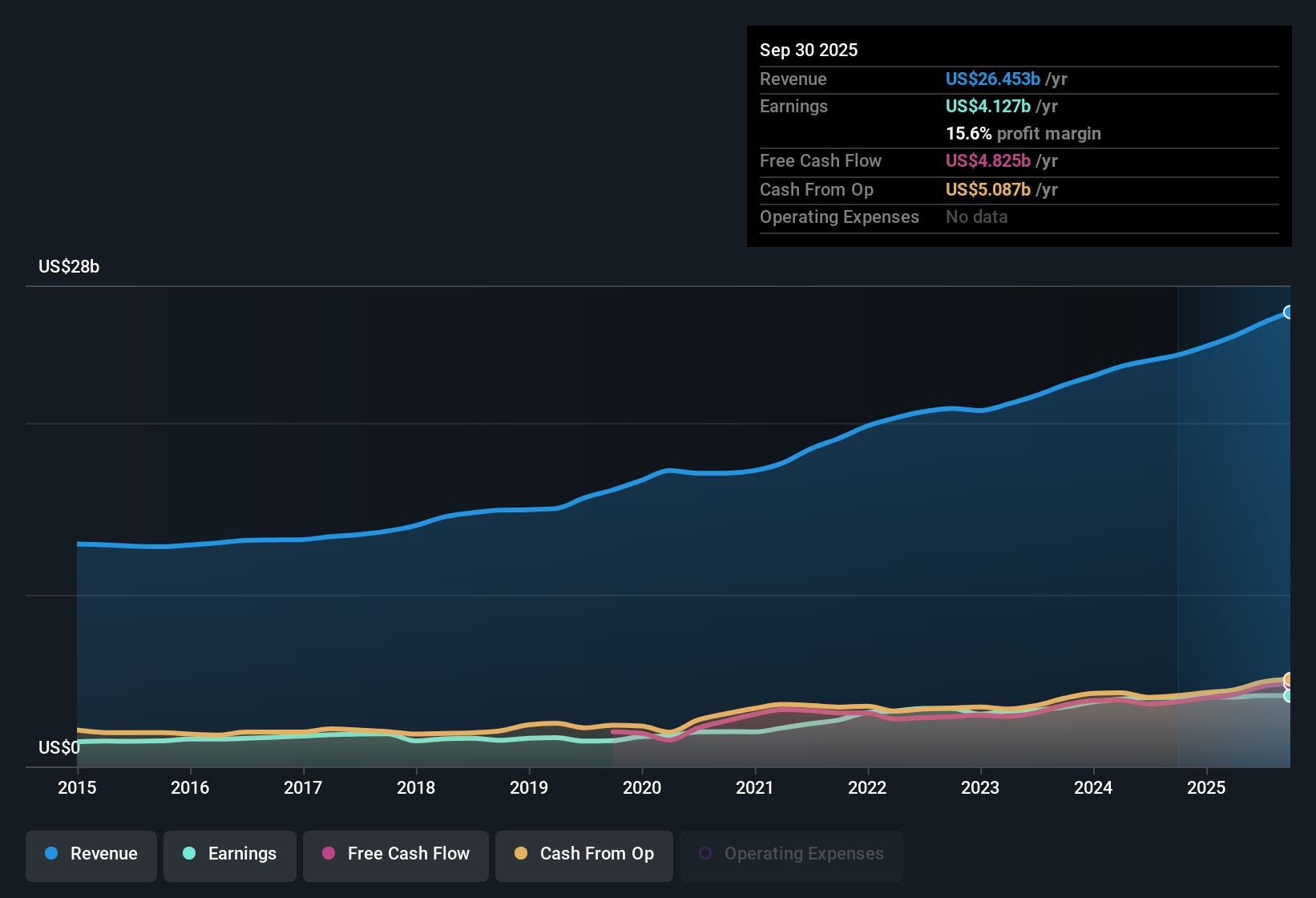

Marsh & McLennan Companies (MMC) reported annual earnings growth of 2.9%, a notable slowdown versus its five-year average of 13.4%. Profit margins also edged lower to 16%, down from 17% the previous year. Analysts forecast earnings growth of 8.4% per year going forward, trailing expectations for the broader US market. With the shares trading at $186.48, investors are focused on the company’s sustained profitability and favorable valuation against analyst price targets and long-term fair value estimates, even as margins and earnings growth show signs of moderation.

See our full analysis for Marsh & McLennan Companies.Next, we’ll see how these headline results stack up against the prevailing market narratives and analyst expectations. This provides a clear look at where the story is confirmed and where it might shift.

See what the community is saying about Marsh & McLennan Companies

Analyst Price Target Sits 21% Above Current Price

- With Marsh & McLennan Companies shares at $186.48, the consensus analyst price target stands at $225.37, representing a potential upside of 21% if analyst growth and profitability estimates are achieved.

- Analysts’ consensus view notes the price target incorporates projected annual revenue growth of 5.9% and an increase in profit margins from 16.0% currently to 17.4% by 2028.

- The target assumes MMC’s price-to-earnings ratio will rise to 26.1x on future 2028 earnings, which is above today’s P/E of 22.2x and higher than the current industry average of 14.2x. This highlights the premium required for the growth story to develop as expected.

- Despite a slowdown in recent annual profit growth to just 2.9%, the consensus is still relying on forward growth and margin improvement to justify a higher valuation than both current sector peers and historic averages.

See how analysts’ expectations stack up in the full Consensus Narrative for Marsh & McLennan Companies and find out what could shift this target.📊 Read the full Marsh & McLennan Companies Consensus Narrative.

P/E Ratio Undercuts Peers, Still Rich Versus Industry

- MMC trades at a price-to-earnings ratio of 22.2x, which is well below the peer average of 54.2x but remains notably elevated compared to the broader US Insurance sector average of 14.2x.

- The consensus narrative notes the interesting tension where, on one hand, MMC’s valuation appears a bargain versus its specialty peer group. On the other hand, it comes at a clear premium to the mainstream insurance sector.

- This premium, despite softening growth trends, reflects the market’s confidence in MMC’s proven track record of high-quality earnings and broad-based consulting, insurance, and advisory exposure.

- Investors weighing sector averages may question whether future earnings and profit margin expansion can fully justify the current price, or if there is risk of valuation compression if expectations are not met.

DCF Fair Value Estimate $80 Above Market

- MMC’s internally estimated DCF fair value is $267.27, which is $80.79 above the current share price. This represents a sizeable discount compared to the analytical calculation of future cash flows.

- The consensus perspective points out that closing this gap would require not only achieving consensus growth rates, but also re-rating the stock above historic and sector multiples. This is an ambitious goal, especially after recent margin slippage.

- For fundamental investors, this gap highlights both upside potential if long-term growth executes as planned and underlying risk if today’s more capital-constrained environment limits expansion or profitability.

- The divergence between the analyst target ($225.37) and DCF fair value ($267.27) highlights an ongoing debate over whether MMC’s best years are yet to come or if the market is rightly discounting execution uncertainty.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Marsh & McLennan Companies on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Think the numbers tell a different story? Put your perspective into action and craft your own unique view in under three minutes. Do it your way

A great starting point for your Marsh & McLennan Companies research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

See What Else Is Out There

While Marsh & McLennan Companies shows slowing earnings growth and premium valuation, its current performance relies heavily on future profit and margin expansion to meet expectations.

If you want to sidestep that uncertainty, check out stable growth stocks screener (2097 results) for companies demonstrating steady, reliable earnings and revenue growth that you can count on through any cycle.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MMC

Marsh & McLennan Companies

A professional services company, provides advisory services and insurance solutions to clients in the areas of risk, strategy, and people worldwide.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion