Hagerty (HGTY) has delivered steady gains lately, with shares rising 8% over the past month and 19% in the past 3 months. Investors are watching closely to see what is behind the momentum.

Looking at the bigger picture, Hagerty’s 1-year total shareholder return of 16% outpaces recent share price moves, which hints that positive sentiment has been building over time. Compared to its recent months, momentum seems to be accelerating as investors respond to improving fundamentals and consistent results.

With shares trending upward, the key question is whether Hagerty is trading below its true value or if the market has already factored in its future growth prospects, leaving little room for upside from this point.

Advertisement

Most Popular Narrative: 7.9% Undervalued

The most popular narrative currently values Hagerty at $13.17 per share, which is about 8% above its recent close of $12.13. This modest upside suggests a measured optimism, highlighting both compelling growth drivers and some ongoing operational challenges for the company.

The ramping State Farm partnership is expected to significantly accelerate new business growth, providing access to over 500,000 current program vehicles and thousands of motivated agents. This is expected to materially expand Hagerty's customer acquisition funnel and recurring commission revenues at attractive margins over the next several years.

Curious what assumptions justify this premium? One growth engine stands out in the narrative, powered by accelerating revenues and a bold expansion of high-margin business lines. Ready to see which critical financial forecasts shape that price target? Explore the surprising backbone behind Hagerty's fair value.

However, Hagerty’s path ahead could be challenged if evolving customer demographics or weaker demand for classic car insurance slows expected premium growth.

Another View: Multiple-Based Valuation Tells a Different Story

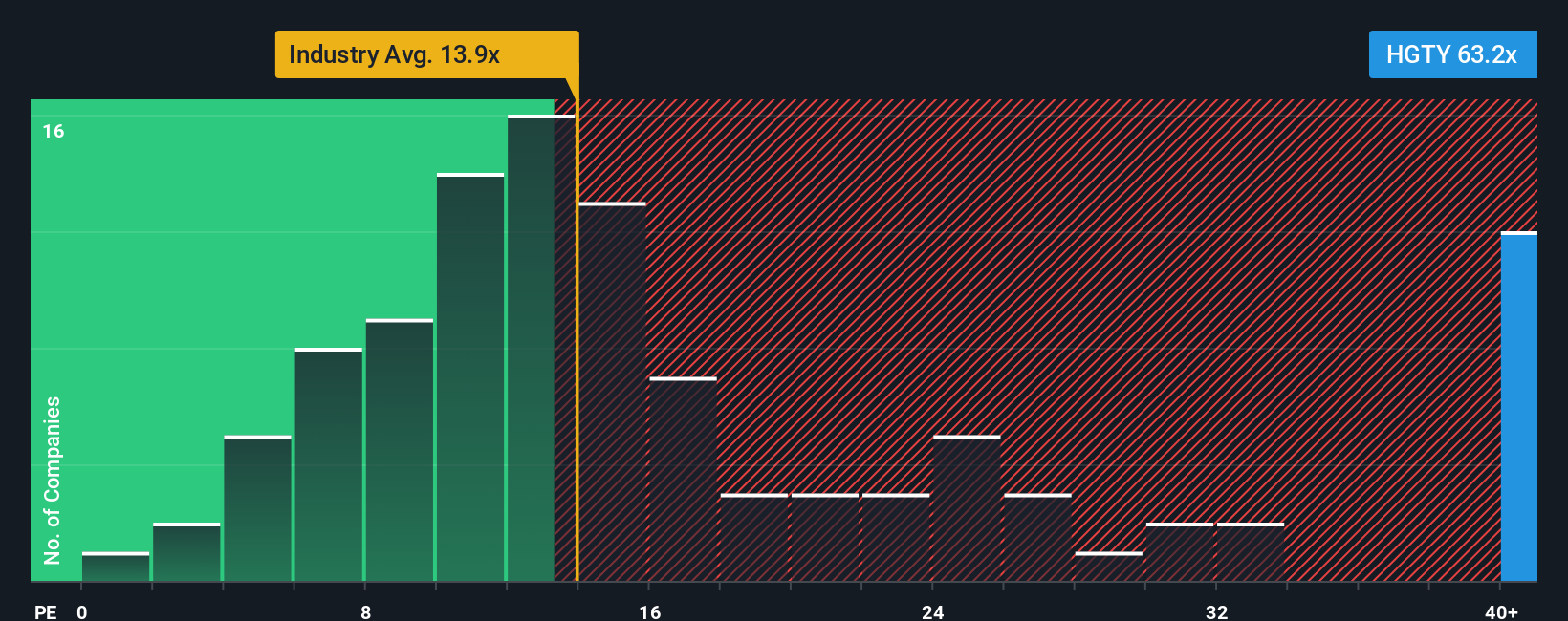

While the most popular narrative suggests Hagerty is undervalued, a look through the lens of price-to-earnings shows a less optimistic picture. The company trades at 65.2 times earnings, far above the US Insurance industry average of 13.7 and even the sector peer average of 80.1. The fair ratio sits at 55.1x, suggesting Hagerty remains expensive by this measure. Such a premium implies investors expect consistently stronger growth. However, there could be implications if these forecasts do not play out.

If you see the story differently or want to dig into the numbers yourself, you can build a custom Hagerty outlook in just a few minutes, your way with Do it your way.

Smart investing means looking beyond a single stock. Broaden your perspective and capture the biggest opportunities the market has to offer with these high-potential stock collections on Simply Wall Street.

Catch the wave of innovation in artificial intelligence by checking out these 24 AI penny stocks and see which businesses could shape tomorrow's technology landscape.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hagerty might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.