Advertisement

- United States

- /

- Insurance

- /

- NYSE:CB

How Analyst Optimism and International Expansion Could Shape Chubb's (CB) Earnings Outlook

Simply Wall St

Reviewed by Sasha Jovanovic

- Chubb Limited (NYSE:CB) has seen renewed analyst optimism and strong investor attention ahead of its third-quarter earnings report scheduled for October 21, 2025, reflecting a pattern of recent earnings beats and expanded international partnerships.

- Analysts and investors are closely watching Chubb’s positive Earnings ESP and its latest Endeavor collaboration, which highlights the company’s continued progress in digital innovation and emerging market expansion.

- To understand how renewed expectations for another earnings beat might affect the outlook, we’ll examine the implications for Chubb’s investment narrative.

Rare earth metals are the new gold rush. Find out which 32 stocks are leading the charge.

Chubb Investment Narrative Recap

Investors in Chubb generally need to trust in the company's ability to drive premium growth internationally and leverage digital innovation, while managing sector headwinds like pricing pressure and elevated catastrophe losses. The recent wave of analyst optimism ahead of the Q3 earnings release points to the upcoming report as a key short-term catalyst, though longer-term risks around margin compression and claims inflation remain unchanged and continue to demand close attention.

The newly announced partnership with Endeavor stands out as most connected to the company’s emerging market ambitions, complementing Chubb’s strategy of expanding its customer base and distribution network globally, a central element for those watching international premium trends and digital channel growth.

In contrast, investors should also consider how rising catastrophe losses could increasingly pressure margins if severe weather events persist...

Read the full narrative on Chubb (it's free!)

Chubb's outlook anticipates $49.6 billion in revenue and $9.8 billion in earnings by 2028. This reflects a 4.8% annual revenue decline and a $0.6 billion increase in earnings from the current $9.2 billion level.

Uncover how Chubb's forecasts yield a $300.90 fair value, a 6% upside to its current price.

Exploring Other Perspectives

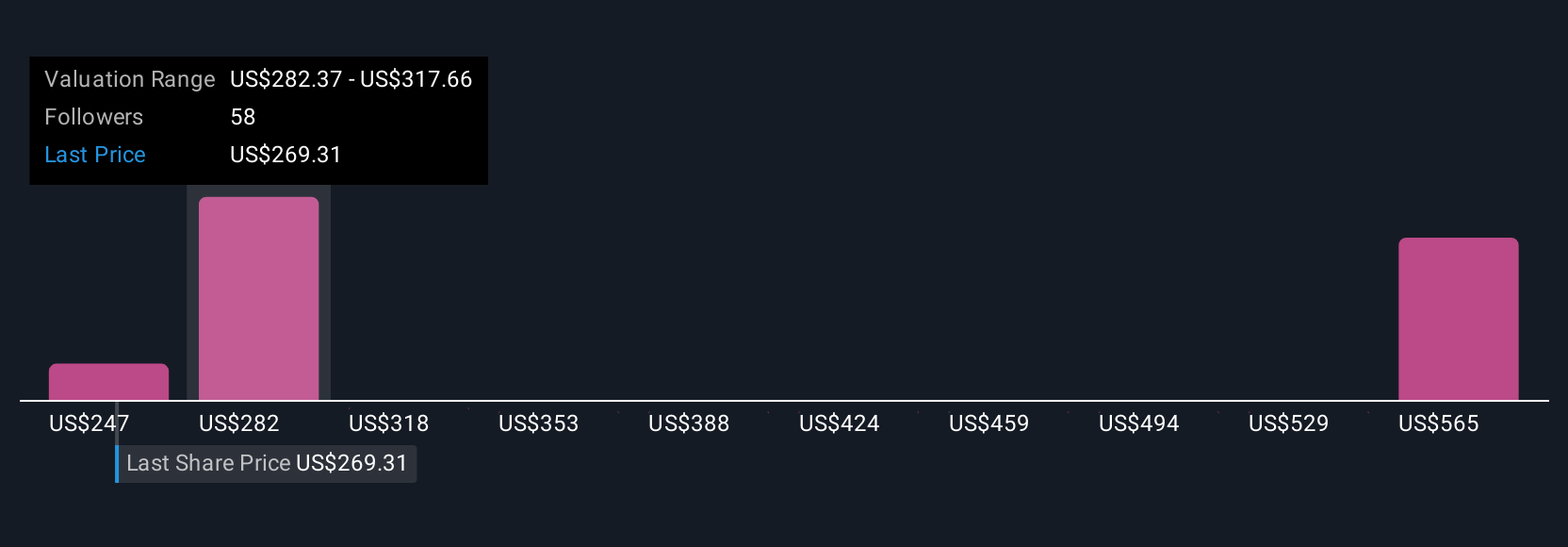

Ten members of the Simply Wall St Community project fair values for Chubb ranging from US$247 to US$610 per share. While some focus on international premium growth as key, others see risk in persistent cost pressures and market volatility, be sure to compare these diverging perspectives.

Explore 10 other fair value estimates on Chubb - why the stock might be worth 13% less than the current price!

Build Your Own Chubb Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Chubb research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Chubb research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Chubb's overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CB

Good value with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor