Advertisement

- United States

- /

- Insurance

- /

- NYSE:CB

Do Chubb’s (CB) Buybacks and Digital Push Mark a Shift in Global Strategy?

Simply Wall St

Reviewed by Sasha Jovanovic

- Chubb Limited recently reported third-quarter results, posting net income of US$2.80 billion, up from US$2.32 billion a year earlier, and completed a US$1.23 billion buyback program repurchasing 4,429,719 shares.

- The company also launched new digital insurance solutions and strengthened international leadership, highlighting ongoing efforts to expand global reach and operational efficiency.

- We'll explore how Chubb's record core operating income and premium growth influence its future investment narrative.

The latest GPUs need a type of rare earth metal called Dysprosium and there are only 37 companies in the world exploring or producing it. Find the list for free.

Chubb Investment Narrative Recap

Owning Chubb means believing in its ability to sustain premium growth and underwriting excellence across global markets, even as competition and rate pressure challenge its margins. The recent strong earnings report and share buyback reinforce capital strength, but do not materially change the short-term catalyst of premium growth or the ongoing risk from pricing softness and margin pressure in large account property lines.

Of the latest announcements, the launch of the digital-first Travel Pro insurance suite stands out as most relevant for the premium growth theme. By embedding tailored travel coverage through digital channels and strategic distribution partnerships, Chubb is aligning with the catalyst of expanding reach and efficiency in high-growth consumer markets.

Yet, in contrast to this innovation, rising cost pressures and softer rates in large property lines remain a concern that investors cannot afford to overlook...

Read the full narrative on Chubb (it's free!)

Chubb's narrative projects $49.6 billion in revenue and $9.8 billion in earnings by 2028. This requires a 4.8% annual revenue decline and a $0.6 billion increase in earnings from $9.2 billion.

Uncover how Chubb's forecasts yield a $303.50 fair value, a 13% upside to its current price.

Exploring Other Perspectives

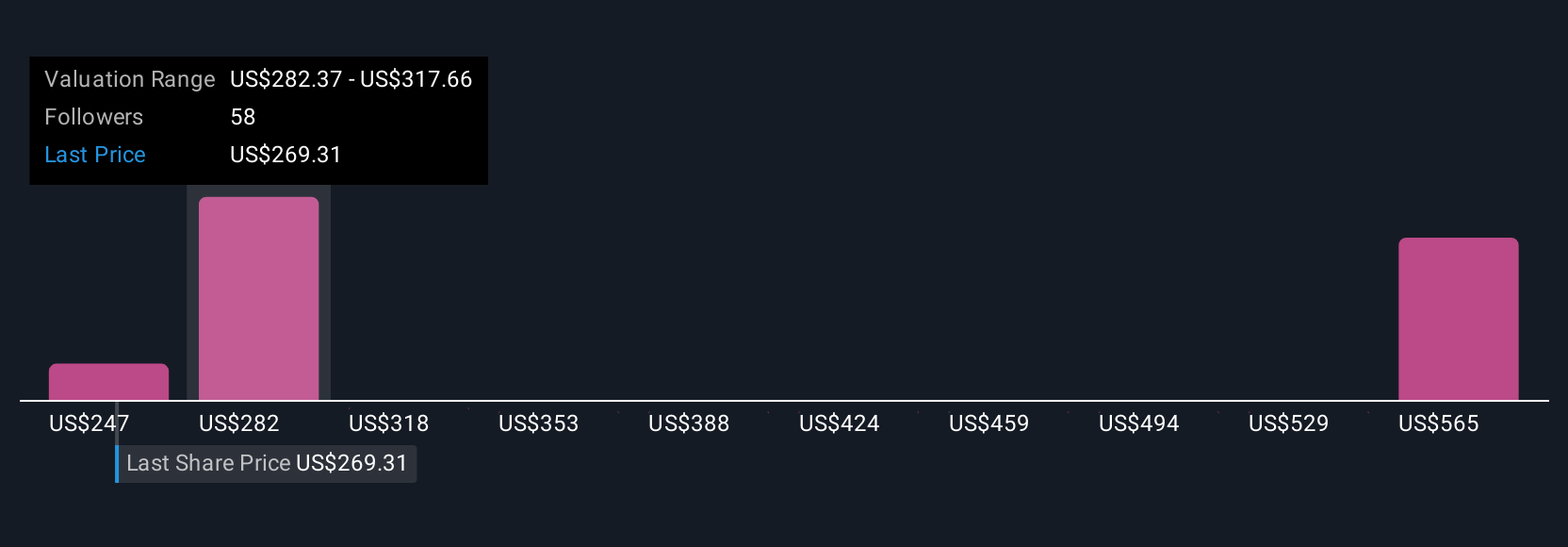

Eight members of the Simply Wall St Community estimate Chubb’s fair value between US$247 and US$598 per share, showing a broad spectrum of expectations. While optimism around international premium growth persists, the community's varied views reflect ongoing debate about future margin performance and growth potential, explore these diverse outlooks and form your own informed perspective.

Explore 8 other fair value estimates on Chubb - why the stock might be worth over 2x more than the current price!

Build Your Own Chubb Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Chubb research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Chubb research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Chubb's overall financial health at a glance.

Looking For Alternative Opportunities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CB

Good value with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|7.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.8% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.4% undervalued

GM

Community Contributor