Advertisement

- United States

- /

- Insurance

- /

- NYSE:AFL

Weighing Aflac’s Long Term Surge and Recent Pullback Around $108.83

Simply Wall St

Reviewed by Bailey Pemberton

- If you have been wondering whether Aflac is still a buy at around $108.83, you are not alone. This stock has quietly turned into a valuation puzzle that is worth unpacking.

- Despite a modest 6.3% gain year to date and a 4.2% return over the last 12 months, the bigger story is its powerful long term trajectory, with the share price up 63.6% over 3 years and 170.2% over 5 years, even after a recent 2.5% dip in the last week and a 1.5% rise over the past month.

- Recent headlines around Aflac have highlighted its steady position in supplemental health and life insurance, as well as ongoing capital returns through buybacks and dividends that keep income focused investors interested. At the same time, broader market debates about interest rates and financial sector risk have kept insurance names like Aflac on investors' watchlists as potential defensive plays.

- On our checks, Aflac currently earns a value score of 2/6, suggesting only limited signs of outright undervaluation. In the rest of this article we will walk through different valuation approaches to see what they are really telling us about Aflac today and finish with a more nuanced way of thinking about value that goes beyond the usual ratios.

Aflac scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Aflac Excess Returns Analysis

The Excess Returns model looks at how effectively Aflac turns shareholder equity into profits above its cost of capital, then capitalizes those surplus returns into an intrinsic value per share.

On this view, Aflac starts from a Book Value base of $54.57 per share and is expected to generate Stable EPS of $10.66 per share, based on the median return on equity from the past 5 years. With an Average Return on Equity of 18.99% and a Cost of Equity of $3.90 per share, the model estimates an Excess Return of $6.75 per share. This implies the company is consistently creating value over and above investors required return.

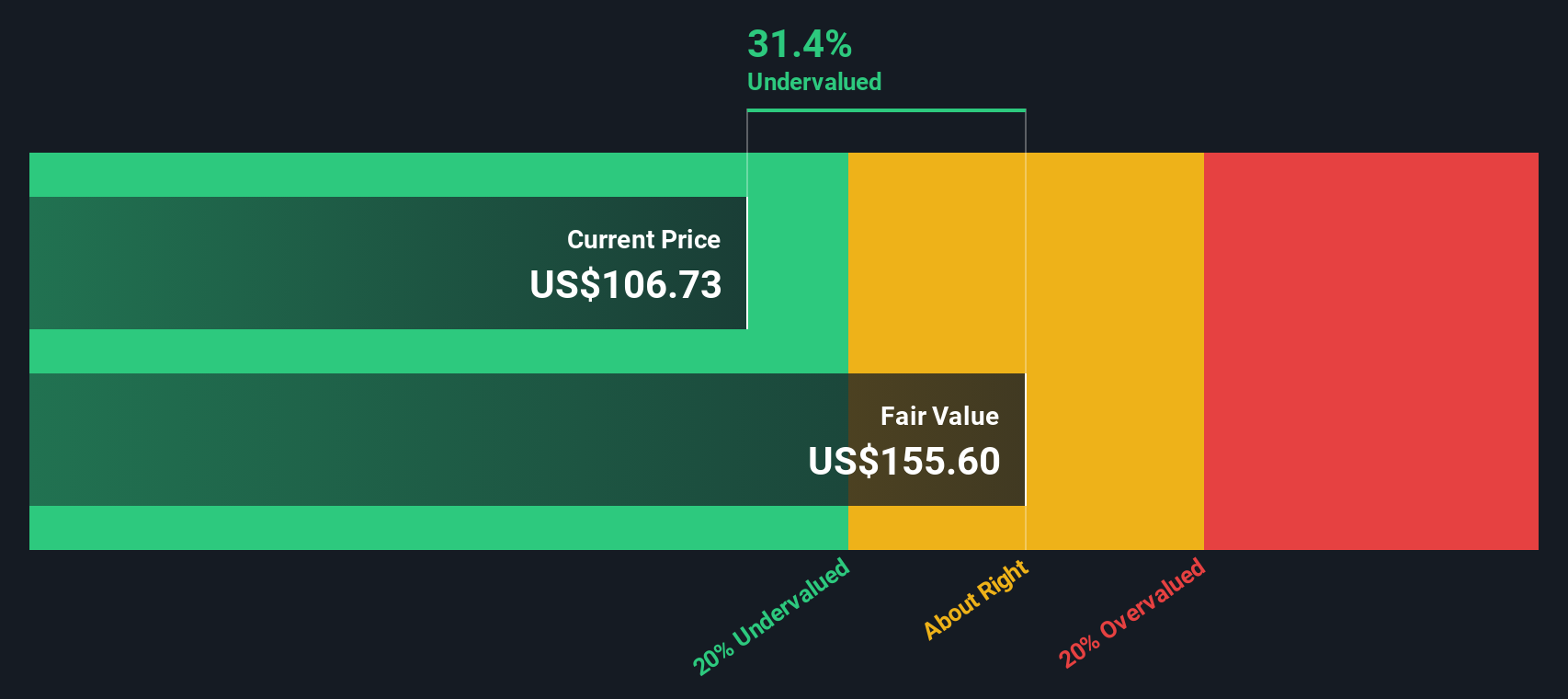

The Stable Book Value is projected at $56.11 per share, using weighted future Book Value estimates from 7 analysts. Capitalizing those excess returns and growth dynamics leads to an intrinsic value estimate of about $238.85 per share. This implies the stock is roughly 54.4% undervalued versus the current price near $108.83.

Result: UNDERVALUED

Our Excess Returns analysis suggests Aflac is undervalued by 54.4%. Track this in your watchlist or portfolio, or discover 925 more undervalued stocks based on cash flows.

Approach 2: Aflac Price vs Earnings

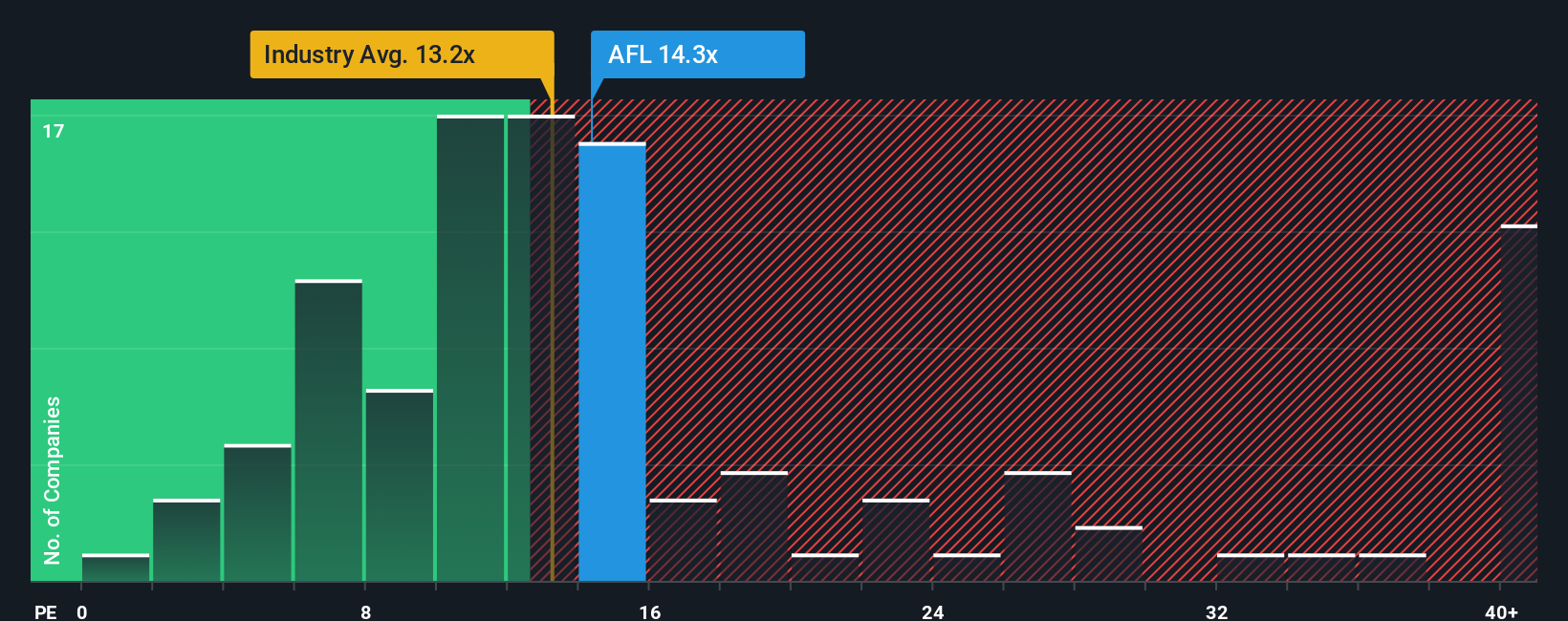

For a mature, consistently profitable insurer like Aflac, the price to earnings ratio is a sensible yardstick because it ties the share price directly to the company’s ongoing ability to generate profits for shareholders. In general, faster growth and lower perceived risk justify a higher PE ratio, while slower growth or higher risk should translate into a lower, more conservative multiple.

Aflac currently trades on a PE of about 13.68x, which is slightly above the Insurance industry average of 13.06x and broadly in line with the peer group average of 13.46x. Simply comparing those numbers might suggest the stock is priced roughly in step with its sector, with only a mild premium.

However, Simply Wall St’s Fair Ratio framework goes a step further by estimating what PE multiple Aflac should trade on, given its earnings growth profile, profitability, risk factors, industry and market cap. For Aflac, that Fair Ratio is 12.98x, implying the shares trade a bit richer than what those fundamentals alone would suggest. On this basis, the stock screens as slightly overvalued rather than outright cheap.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1441 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Aflac Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, a simple idea on Simply Wall St’s Community page where you connect your view of Aflac’s story to concrete numbers by setting your own expectations for future revenue, earnings and margins. You then turn that story into a forecast and then into a Fair Value you can compare with today’s price to decide whether to buy, hold or sell. The platform keeps your Narrative up to date as new news and earnings arrive. For example, one investor might build a bullish Aflac Narrative around product innovation, digital efficiency and stable margins that supports a Fair Value closer to $124 per share. Another investor might focus on Japan concentration, currency risk and sluggish US sales and land nearer $99, giving you a clear, dynamic range of plausible outcomes instead of a single static PE ratio.

Do you think there's more to the story for Aflac? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:AFL

Aflac

Through its subsidiaries, provides supplemental health and life insurance products.

Established dividend payer with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

18 followersusers have followed this narrative

5 commentsusers have commented on this narrative

5 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1919.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5200.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Applied Digital ·

Staggered by dilution; positions for growth

Fair Value:US$35.4520.9% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.5% undervalued

949 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.1% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative