- United States

- /

- Insurance

- /

- NasdaqCM:KINS

Investors Still Aren't Entirely Convinced By Kingstone Companies, Inc.'s (NASDAQ:KINS) Revenues Despite 27% Price Jump

Despite an already strong run, Kingstone Companies, Inc. (NASDAQ:KINS) shares have been powering on, with a gain of 27% in the last thirty days. The last 30 days were the cherry on top of the stock's 436% gain in the last year, which is nothing short of spectacular.

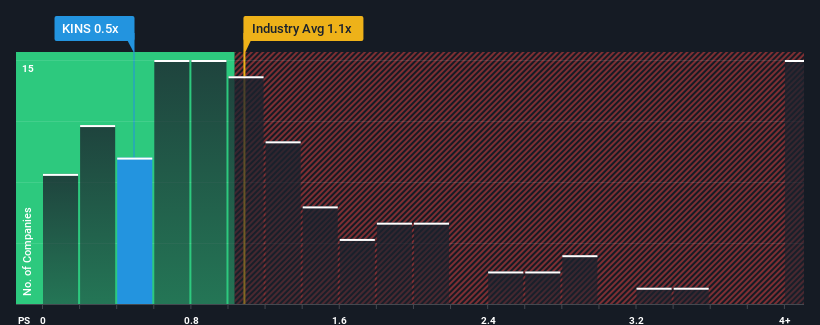

Although its price has surged higher, when close to half the companies operating in the United States' Insurance industry have price-to-sales ratios (or "P/S") above 1.1x, you may still consider Kingstone Companies as an enticing stock to check out with its 0.5x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

View our latest analysis for Kingstone Companies

What Does Kingstone Companies' P/S Mean For Shareholders?

With revenue growth that's inferior to most other companies of late, Kingstone Companies has been relatively sluggish. Perhaps the market is expecting the current trend of poor revenue growth to continue, which has kept the P/S suppressed. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Kingstone Companies.What Are Revenue Growth Metrics Telling Us About The Low P/S?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Kingstone Companies' to be considered reasonable.

Taking a look back first, we see that the company managed to grow revenues by a handy 3.7% last year. However, due to its less than impressive performance prior to this period, revenue growth is practically non-existent over the last three years overall. So it appears to us that the company has had a mixed result in terms of growing revenue over that time.

Shifting to the future, estimates from the only analyst covering the company suggest revenue should grow by 11% over the next year. With the industry only predicted to deliver 4.8%, the company is positioned for a stronger revenue result.

With this information, we find it odd that Kingstone Companies is trading at a P/S lower than the industry. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

The Final Word

Despite Kingstone Companies' share price climbing recently, its P/S still lags most other companies. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

A look at Kingstone Companies' revenues reveals that, despite glowing future growth forecasts, its P/S is much lower than we'd expect. There could be some major risk factors that are placing downward pressure on the P/S ratio. At least price risks look to be very low, but investors seem to think future revenues could see a lot of volatility.

Plus, you should also learn about these 3 warning signs we've spotted with Kingstone Companies (including 1 which is a bit unpleasant).

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Kingstone Companies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:KINS

Kingstone Companies

Through its subsidiary, provides property and casualty insurance products in the United States.

High growth potential with proven track record.

Market Insights

Community Narratives